Every outsourced bookkeeping firm’s website says the same things: “accurate books,” “dedicated team,” “industry expertise.” The proposals look similar. The pricing seems comparable. And yet, the wrong choice will cost you three to six months of lost time, messy data, and a painful migration to the next provider. If you’re evaluating outsourced bookkeeping firms for your professional services firm, you need a structured framework — not a gut check.

This 12-point checklist is built for managing partners and firm owners running $1M–$10M professional services businesses. It covers every dimension that matters — from industry expertise to contract terms — so you can separate serious providers from generalists before you sign anything.

Switching bookkeeping providers is expensive. The direct cost of onboarding — chart of accounts migration, historical cleanup, access provisioning — typically runs $2,000–$5,000. But the real cost is the three to four months of degraded financial visibility while a new team learns your business. During that window, you’re making hiring decisions, pricing projects, and managing cash flow on stale or incomplete data.

A structured evaluation upfront eliminates most of the risk. You’re not looking for perfection — you’re looking for alignment between what your firm needs and what the provider actually delivers. Here are the 12 criteria that matter most.

This is the single most important factor. A bookkeeping firm that specializes in professional services — law firms, architecture practices, consulting firms, property management companies — understands your financial dynamics on day one. They know what Work in Progress (WIP) tracking looks like, how to handle retainer accounting, and why your chart of accounts needs project-level classes.

A generalist firm will learn these things on your dime. They’ll miscategorize retainer payments as revenue (instead of deferred revenue), ignore WIP entirely, and lump all labor costs into a single line item. That’s not bookkeeping — it’s data entry that creates more problems than it solves.

What to ask: “How many firms in my specific industry do you currently serve? Can you show me a sample chart of accounts for a firm like mine?” If they hesitate, move on.

Your bookkeeping partner needs to work fluently with your existing tools. For professional services firms, that typically means QuickBooks Online or Xero as the accounting platform, plus integrations with your practice management software — Clio for law firms, Harvest or Toggl for consulting, AppFolio or Buildium for property management, Procore for construction.

The right provider has already built workflows between these systems. They know the common sync issues, the data mapping requirements, and the automation opportunities. The wrong provider will treat your tech stack as a “we’ll figure it out” project. For guidance on how a properly configured accounting system should look, see our QuickBooks Online setup guide.

What to ask: “Walk me through how you handle the integration between [your PM software] and QuickBooks. What syncs automatically, and what requires manual intervention?”

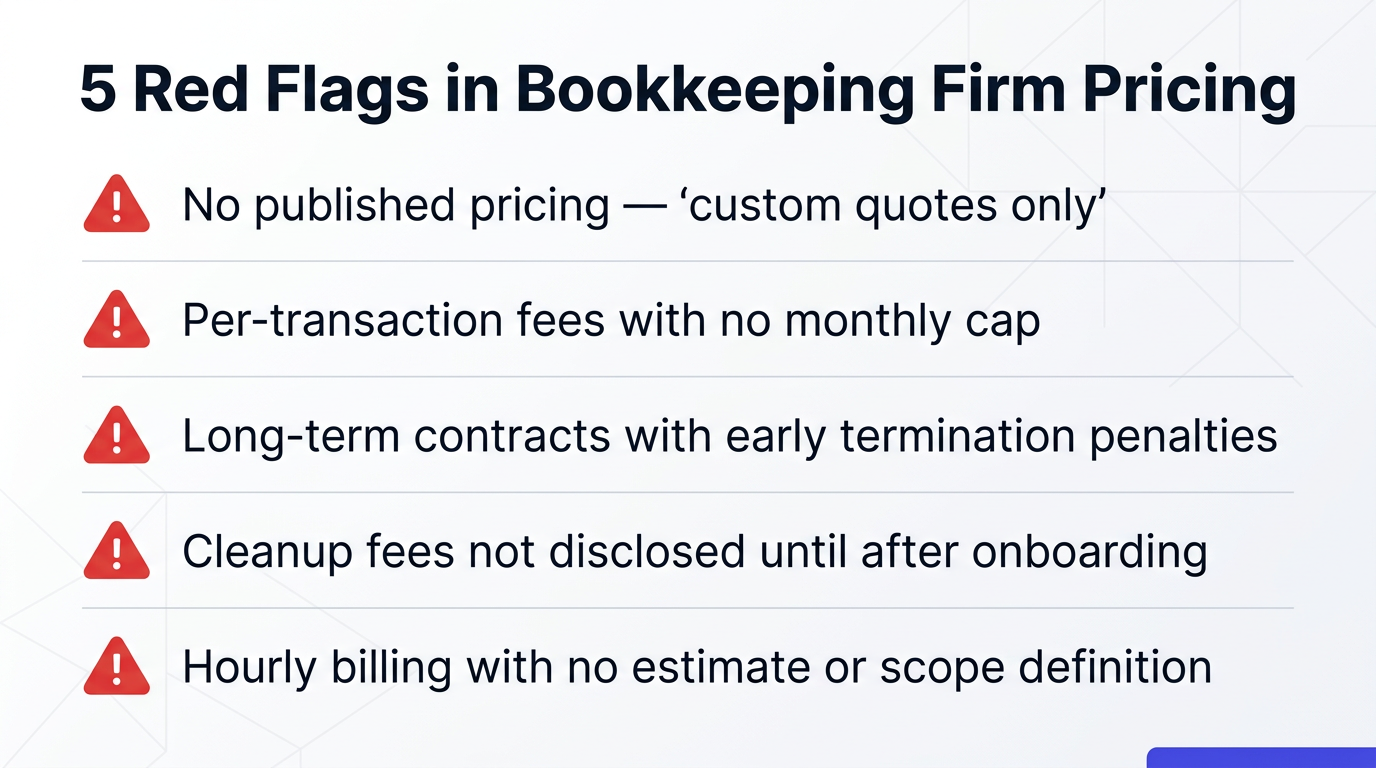

Transparent pricing is a signal of confidence and maturity. The best outsourced bookkeeping firms publish their pricing tiers on their website and quote flat monthly fees based on transaction volume and complexity. For a deeper analysis of what these fees should look like, read our outsourced bookkeeping cost breakdown.

Be cautious of firms that only offer “custom quotes” without any published range. Per-transaction pricing with no cap is another warning sign — your costs scale unpredictably as your business grows. Flat-fee pricing, with clearly defined inclusions and exclusions, gives you budget certainty and aligns incentives: the provider is motivated to build efficient processes, not maximize billable hours.

What to ask: “Is your pricing flat-fee or variable? What’s included in the base fee, and what triggers additional charges?”

The first 30 days define the entire engagement. A professional bookkeeping firm has a documented onboarding process with clear milestones: access provisioning in days one through three, chart of accounts review in week one, historical data review and cleanup scope in week two, first month-end close by day 30.

Vague onboarding — “we’ll get started and figure things out as we go” — is a red flag. You should receive a written onboarding timeline before signing, with named team members responsible for each step. The best providers also assign an onboarding specialist who is separate from the ongoing engagement team, so the transition gets dedicated attention.

What to ask: “Can I see your standard onboarding timeline? What do you need from us in the first week, and what deliverables should we expect by day 30?”

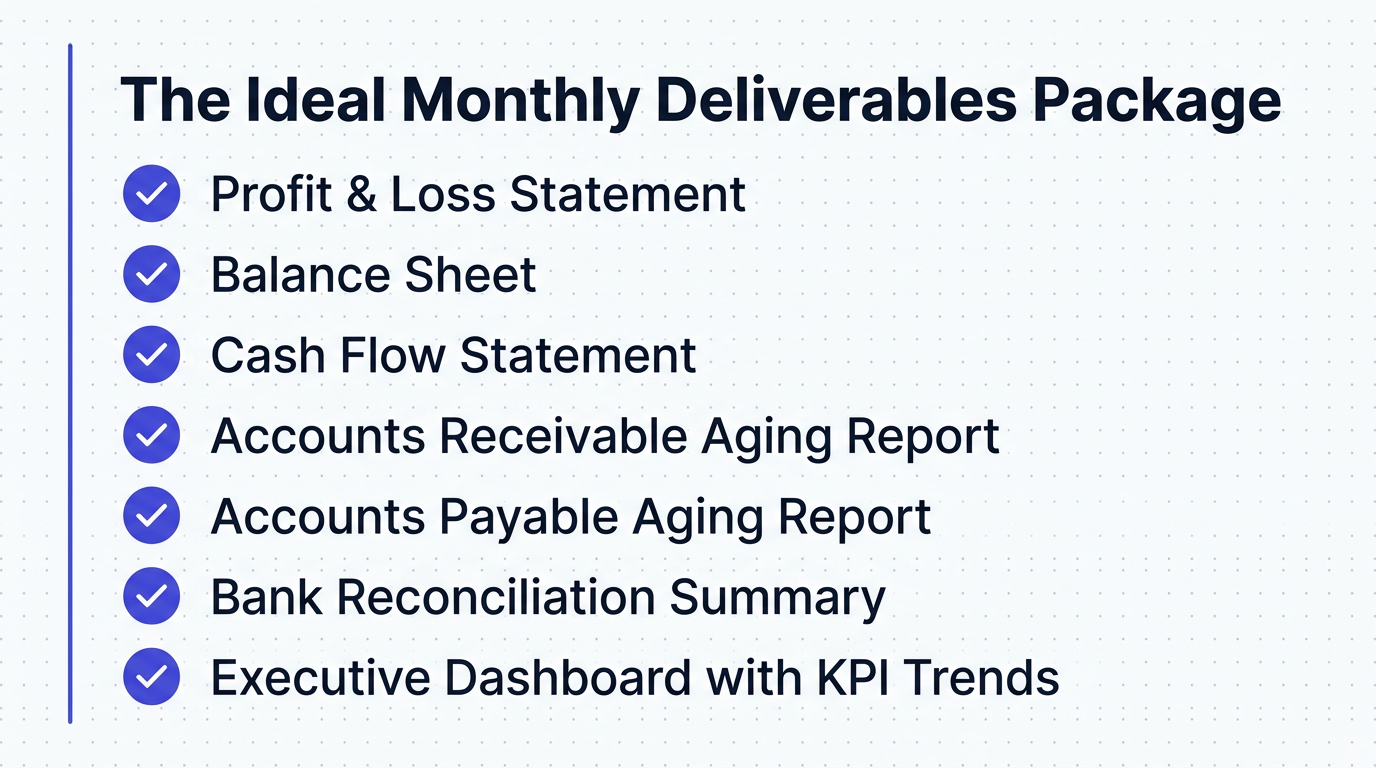

This is where many firms fall short. Basic bookkeeping gives you a P&L and Balance Sheet. A professional services-focused provider delivers a complete monthly package that drives actual business decisions:

| Deliverable | Why It Matters for Professional Services |

|---|---|

| Profit & Loss Statement | Revenue and expense tracking by period, department, or project class |

| Balance Sheet | Assets, liabilities, and equity — including WIP and deferred revenue |

| Cash Flow Statement | Actual liquidity vs. accrual profitability (they’re often very different) |

| AR Aging Report | Who owes you, how much, and how overdue — critical for collections |

| AP Aging Report | What you owe vendors, with payment due dates to manage cash flow |

| Bank Reconciliation | Proof that every transaction is accounted for — your audit trail |

| Executive Dashboard | KPI trends: revenue growth, margins, utilization, collection rates |

If a provider can’t commit to all seven of these in writing, they’re not equipped for a professional services firm at your level.

Outsourced bookkeeping works when communication is structured and predictable. You should know exactly when you’ll hear from your team, through which channels, and with what response time guarantees. The standard for professional services engagements: same-day acknowledgment of requests, 24–48 hour resolution for standard items, and a monthly review call to discuss financials and trends.

Ask specifically about escalation procedures. When something urgent comes up — a client dispute, a cash flow crunch, an unexpected vendor bill — how fast can they turn around an answer? The best firms offer a named point of contact with a direct communication line, not a generic support queue.

What to ask: “What’s your guaranteed response time for urgent requests? How do monthly review meetings work?”

Dedicated teams outperform rotating staff every time. When the same bookkeeper handles your account month after month, they learn your business patterns, your vendor relationships, and your approval workflows. They stop asking questions about routine transactions and start flagging only the exceptions that matter.

Rotating staff means re-training every month. The new person doesn’t know that the $4,200 charge from ABC Consulting is a recurring retainer (not a one-time expense), so they categorize it wrong. Multiply that by twenty transactions and your financials are unreliable. Ask whether you’ll have a dedicated team and who your primary contact will be.

Your bookkeeper’s job doesn’t end with monthly financials. They need to hand your CPA a clean, organized file at year-end — and ideally, they should be supporting estimated tax calculations quarterly. CPA-ready books means: all transactions categorized to the correct tax-relevant accounts, 1099 contractor payments properly tracked and classified, depreciation schedules maintained, and owner distributions separated from operating expenses.

The real test is what happens at tax time. If your CPA sends back a list of 30 questions and reclassification requests, your bookkeeping isn’t CPA-ready — it’s CPA-adjacent. A good outsourced firm coordinates directly with your CPA and resolves issues before the filing deadline.

What to ask: “Do you coordinate directly with our CPA? What does your year-end close process look like?” Cross-reference their answer with AICPA standards for financial reporting quality.

Your firm today is not the same firm it will be in two years. If you’re at $1.5M now and targeting $4M, your bookkeeping needs will change dramatically — more transactions, more employees, more complex project structures, potentially multiple entities. The provider you choose needs to scale with you without a painful migration.

Ask about their client size range. If their largest client is a $500K solo practice, they may not have the processes or capacity to support a $5M firm with 30 employees and multi-state tax obligations. Conversely, if their minimum engagement is $10M, you’ll be their smallest (and lowest-priority) client.

What to ask: “What’s the revenue range of your current clients? How does your service model change as a firm grows from $1M to $5M?”

Your bookkeeping provider will have access to your bank accounts, payroll data, and sensitive financial records. You need to know how they protect that data. At minimum, look for: role-based access controls (not everyone on the team sees everything), two-factor authentication on all financial accounts, encrypted file transfer for sensitive documents, and a clear data retention and deletion policy.

Also ask about their employee screening process. Who on their team will access your financial systems? Do they run background checks? What happens when a team member leaves the firm — how quickly is access revoked? These aren’t hypothetical concerns for firms handling client trust accounts or sensitive financial data.

Every bookkeeping firm will tell you they’re great. References let you verify. Ask for two to three references from firms similar to yours — same industry, similar revenue range, comparable complexity. Then actually call them.

The questions to ask references: How long have you worked together? How smooth was onboarding? How accurate are the monthly financials? Have you ever had a significant error, and how was it resolved? Would you hire them again? The answers to these questions tell you more than any sales presentation ever will.

What to ask the provider: “Can you connect me with two or three current clients in my industry? Do you have any case studies showing measurable results?”

The best outsourced bookkeeping relationships are built on performance, not contracts. Month-to-month terms (or a short 90-day initial commitment) signal that the provider is confident in their service quality. Long-term contracts with early termination penalties signal the opposite — they need the contract because they can’t rely on the results to keep you.

Review the contract carefully for: data ownership (you own your books, always), transition assistance if you leave (they should help migrate your data), scope of work definition (what’s included vs. out-of-scope), and billing terms (net 15, net 30, autopay). A clean exit clause protects both parties and sets the right tone for the relationship. For context on how in-house vs. outsourced engagements compare on flexibility and commitment, see our full analysis.

Beyond the 12-point checklist, watch for these warning signs during the evaluation process:

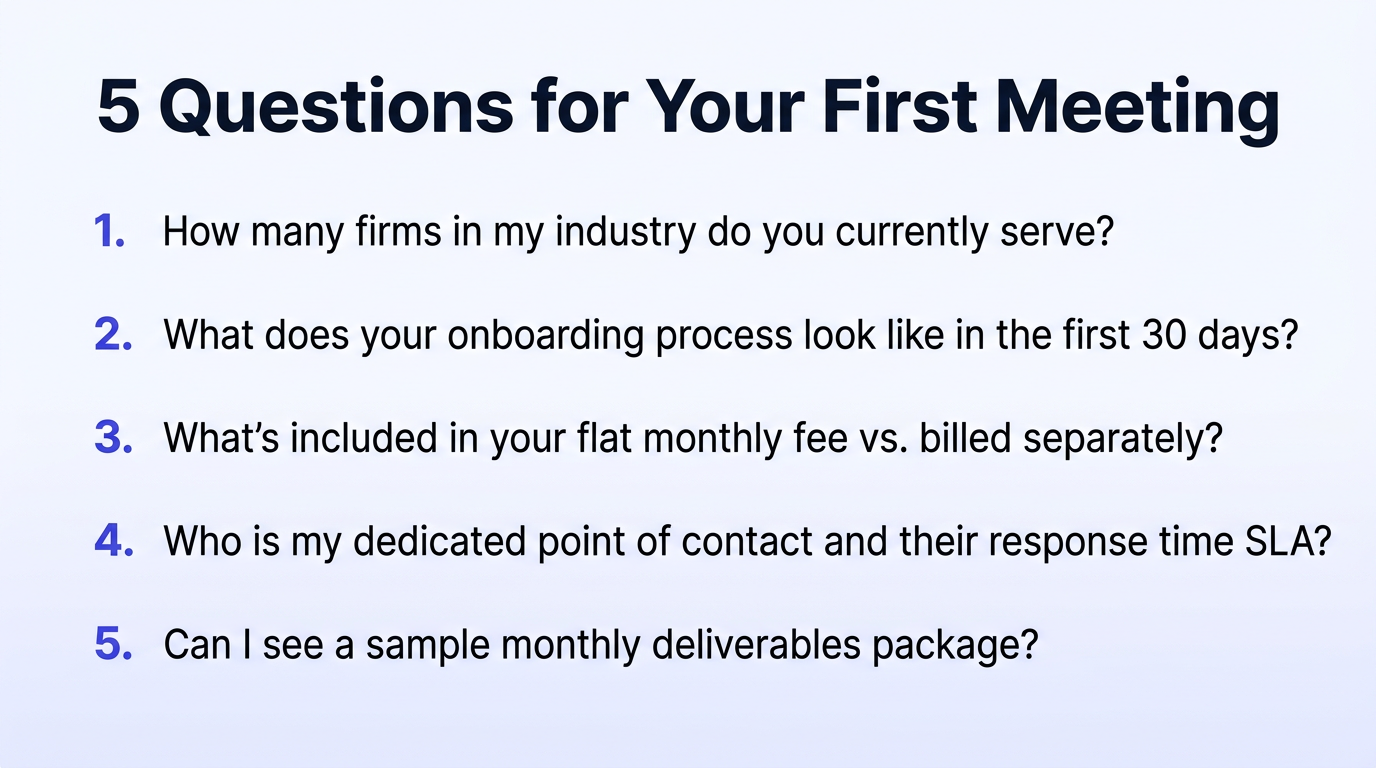

Once you’ve narrowed your list to two or three candidates, schedule a 45-minute evaluation call with each. Structure it around these five areas:

Minutes 1–10: Your firm overview. Share your revenue range, team size, industry, current tech stack, and the specific pain points driving your search. This gives the provider context to tailor their responses.

Minutes 10–25: Their process walkthrough. Ask them to walk through onboarding, a typical month-end close, and their reporting cadence. Listen for specificity — dates, deliverables, named team members — not vague promises.

Minutes 25–35: Industry-specific depth. Ask how they handle the unique financial dynamics of your industry. For law firms: IOLTA reconciliation and trust accounting. For consulting: WIP tracking and project-level P&L. For property management: security deposit escrow and owner distributions. If they can’t speak fluently about your industry’s bookkeeping challenges, they’ll learn on your dime.

Minutes 35–40: Pricing and terms. Get a clear answer on monthly cost, what’s included, onboarding fees, and contract length. Compare to the benchmarks in our outsourced bookkeeping cost guide.

Minutes 40–45: References and next steps. Request client references in your industry and ask about their timeline to start. A provider who can begin within two weeks has capacity. A provider who says “we can start in six to eight weeks” may be overcommitted.

Score each candidate against the 12 criteria on a simple 1–3 scale (1 = doesn’t meet, 2 = partially meets, 3 = fully meets). Weight industry specialization, monthly deliverables, and communication cadence highest — these three factors have the largest impact on day-to-day satisfaction.

The right provider won’t score perfectly on every dimension. What matters is alignment on the criteria that matter most for your firm, a clear onboarding process, and terms that give you flexibility if the relationship doesn’t work out.

Ready to see what a structured bookkeeping engagement looks like for professional services firms? Request a free bookkeeping diagnostic — we’ll review your current setup, walk you through our process against every point on this checklist, and give you an honest assessment of whether we’re the right fit.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.