If your firm handles client funds, IOLTA trust account reconciliation is not optional — it is your most critical compliance obligation. A single misstep can trigger state bar investigations, malpractice claims, and even disbarment. Yet many managing partners treat trust accounting as an afterthought, delegating it to staff without clear processes or oversight.

This guide walks through exactly how three-way IOLTA trust account reconciliation works, the violations that get firms in trouble, and the systems that keep you compliant without burning hours every month.

An IOLTA (Interest on Lawyers’ Trust Accounts) account holds client funds that are either too small or held too briefly to earn net interest for the individual client. Instead of sitting idle, the pooled interest funds legal aid programs in your state.

Every state bar requires lawyers to maintain IOLTA accounts separate from operating funds. The core rule is simple: client money never touches your operating account. Retainers, settlement proceeds, escrow deposits, and prepaid costs all go into the trust account until earned or disbursed.

The distinction matters because commingling — even accidentally — is one of the most frequently disciplined ethics violations in legal practice. According to the American Bar Association, trust account mismanagement is a leading cause of attorney discipline nationwide.

Why this matters for your bottom line: Trust account errors do not just create compliance risk. They signal operational dysfunction that bleeds into billing accuracy, collections, and client confidence. Firms with clean trust accounting consistently report stronger financial KPIs across the board.

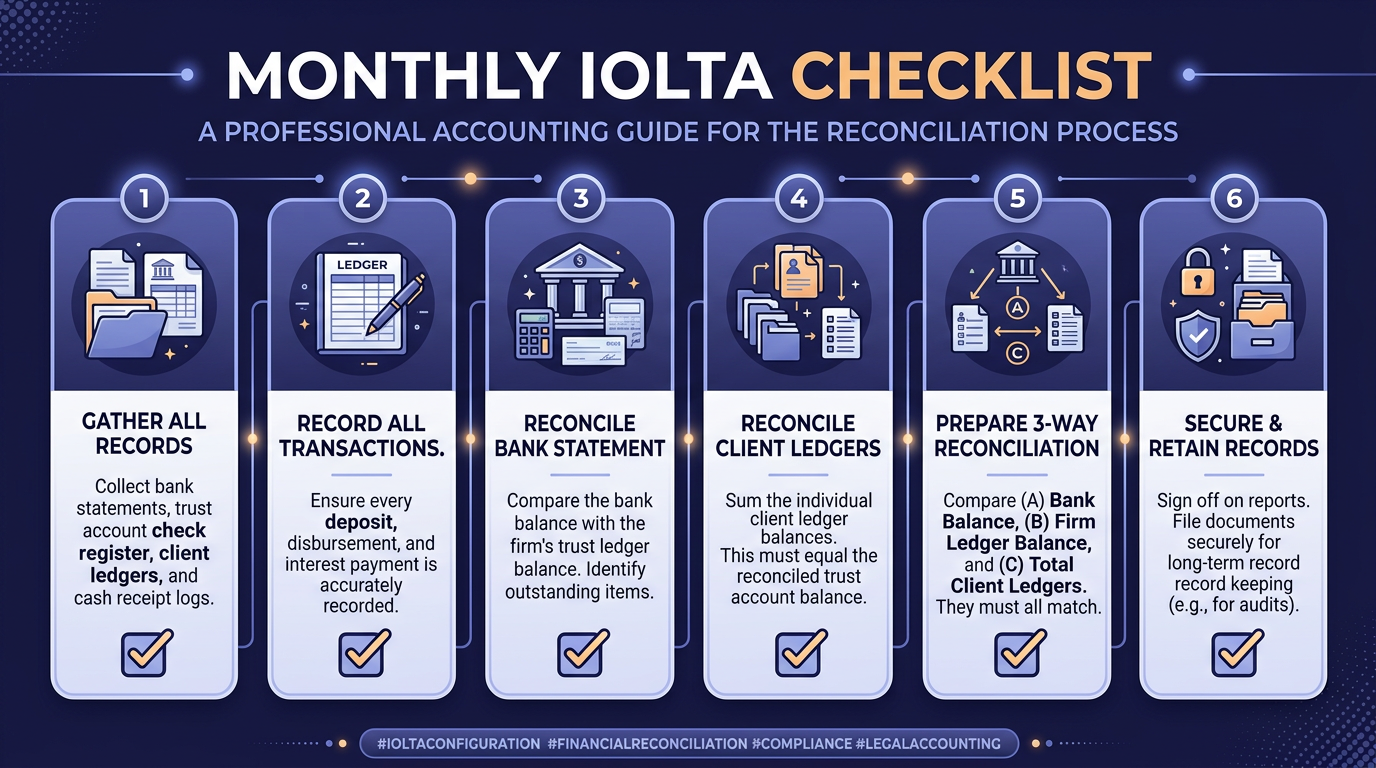

Three-way reconciliation is the gold standard for IOLTA trust account reconciliation. It cross-checks three independent records to ensure every dollar is accounted for:

When all three match, your trust account is reconciled. When they do not, you have a problem that needs immediate attention.

Before you start, pull together:

Start with the ending bank statement balance and adjust for timing differences:

If the adjusted bank balance matches your book balance, you have completed the first leg of the reconciliation.

This is where most firms fall short. Pull every individual client ledger and sum the balances:

Critical: If your client ledger total does not match your book balance, stop and investigate immediately. The discrepancy means either a transaction was recorded to the wrong client, a transaction was missed entirely, or there is an unauthorized disbursement. Never adjust a client ledger to force a match.

With all three figures in hand, confirm:

If all three agree, document the reconciliation with:

Common causes of discrepancies include:

Resolve every discrepancy before closing the month. Carrying forward unresolved items compounds the problem and makes future reconciliations exponentially harder.

Trust account violations carry severe consequences. Here are the issues state bars see most frequently:

| Violation | Description | Typical Penalty |

|---|---|---|

| Commingling | Mixing personal or firm operating funds with client funds | Suspension (6 months to 3 years) |

| Misappropriation | Using client funds for firm expenses or personal use | Disbarment |

| Failure to reconcile | Not performing monthly three-way reconciliation | Public reprimand or suspension |

| Negative client balance | Disbursing more than a client has in trust | Suspension + restitution |

| Failure to maintain records | Incomplete or missing trust account records | Private or public reprimand |

| Delayed disbursement | Holding earned fees in trust beyond a reasonable time | Reprimand + fee dispute |

| Overdraft notification | Bank reports an overdraft to the state bar (automatic in most states) | Triggered investigation |

| Failure to return funds | Not returning unearned retainer or unused cost deposits | Suspension + restitution |

Most state bars have automatic overdraft notification agreements with banks. If your IOLTA account goes negative — even for a single day due to a timing issue — the bank notifies your state bar, and you receive an inquiry letter. The presumption is against you until you prove it was a clerical error.

Real talk: The managing partners we work with at law firms are not misappropriating funds. They are getting caught by sloppy processes — skipped reconciliations, no secondary review, deposits applied to the wrong client. The penalties are the same regardless of intent.

Every state has its own trust account rules, but the common requirements include:

Some states have moved to proactive management-based regulation, where firms must demonstrate compliance systems rather than just responding to complaints. If your state adopts this model, having documented reconciliation procedures and strong financial controls becomes essential evidence of compliance.

When a state bar auditor reviews your trust account, they typically examine:

Manual trust accounting with spreadsheets is a compliance risk in itself. Purpose-built law firm bookkeeping software automates the three-way reconciliation and flags issues before they become violations.

Your trust accounting software should integrate with QuickBooks Online or your general ledger system so that:

The right software does not replace the need for someone who understands trust accounting rules — it just makes the mechanical process faster and less error-prone.

Trust accounting is one area where the cost of getting it wrong dwarfs the cost of getting help. Consider bringing in a specialized law firm bookkeeper if:

Firms that invest in proper trust accounting — whether in-house or outsourced — typically spend $500–$1,500/month on the function. Firms that face state bar discipline spend $10,000–$50,000+ on defense costs alone, not counting the reputational damage, lost clients, and potential malpractice insurance premium increases.

The math is straightforward: proactive compliance costs a fraction of reactive damage control.

The firms that never have trust account problems share three habits:

These are not complex systems. They are disciplines. And they protect your license, your firm, and your clients.

Ready to get your trust accounting under control? Steph’s Books provides dedicated bookkeeping for law firms, including IOLTA trust account reconciliation, three-way matching, and state bar compliance support. Schedule a free consultation and let us handle the numbers so you can focus on your practice.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.