A 12-attorney litigation firm in Chicago discovered $87,000 in unbilled time sitting in their practice management system — work that had been completed, never invoiced, and was now past the 90-day window where clients pay without pushback. That’s not a billing problem. That’s a law firm bookkeeping problem.

Law firm bookkeeping carries requirements that most general bookkeepers have never encountered: IOLTA trust accounts with state bar compliance obligations, partner equity tracking across multiple compensation models, revenue recognition rules that change based on whether you bill hourly or flat fee, and financial KPIs that don’t exist in any other industry.

This guide covers every financial management challenge specific to law firms between $1M and $10M in revenue. If you’re a managing partner or ops director who already knows what a P&L is, this is where you go deeper — into the systems, compliance rules, and metrics that actually determine whether your firm is profitable or just busy.

Every professional services firm tracks billable hours. Law firms are the only ones where a bookkeeping mistake can trigger a state bar investigation, a malpractice claim, or personal liability for every named partner.

Three structural differences make law firm bookkeeping fundamentally different from standard business accounting:

Your revenue isn’t recognized when work is performed — it’s recognized when work is billed and (depending on your accounting method) collected. That creates a cascade of timing issues:

A firm billing $5M annually with a 15% realization gap is leaving $750,000 on the table. Your bookkeeping system needs to track that gap at the matter level, not just the firm level.

Every state bar in the country requires lawyers to hold client funds in trust accounts separate from operating funds. Commingling even $1 of client money with firm money is an ethical violation — regardless of intent. Your bookkeeper needs to understand the difference between a retainer held in trust (the client’s money) and a retainer earned upon receipt (your money). Getting that wrong isn’t a bookkeeping error. It’s a bar complaint.

In a standard LLC or S-Corp, owners take distributions. In a law firm, partner compensation involves guaranteed payments, equity draws, profit-sharing allocations, and capital account tracking — often with different terms for equity partners, non-equity partners, and of-counsel attorneys. Your bookkeeper needs to track each partner’s capital account, distributions, guaranteed payments, and their share of profits for K-1 preparation. Most general bookkeepers have never prepared a multi-partner K-1 schedule.

Key insight: The average law firm spends 15-20% of gross revenue on administrative overhead. Firms with specialized law firm bookkeeping systems consistently run 3-5 percentage points lower — because clean financial data prevents the revenue leakage, duplicate payments, and missed billing that inflate overhead. For a $3M firm, that’s $90,000-$150,000 in recovered margin annually.

IOLTA (Interest on Lawyers’ Trust Accounts) management is the single highest-stakes bookkeeping task in any law firm. A 2024 American Bar Association study found that trust account violations are among the top three reasons for attorney discipline nationwide.

Funds that must go into your IOLTA account:

Funds that never belong in trust:

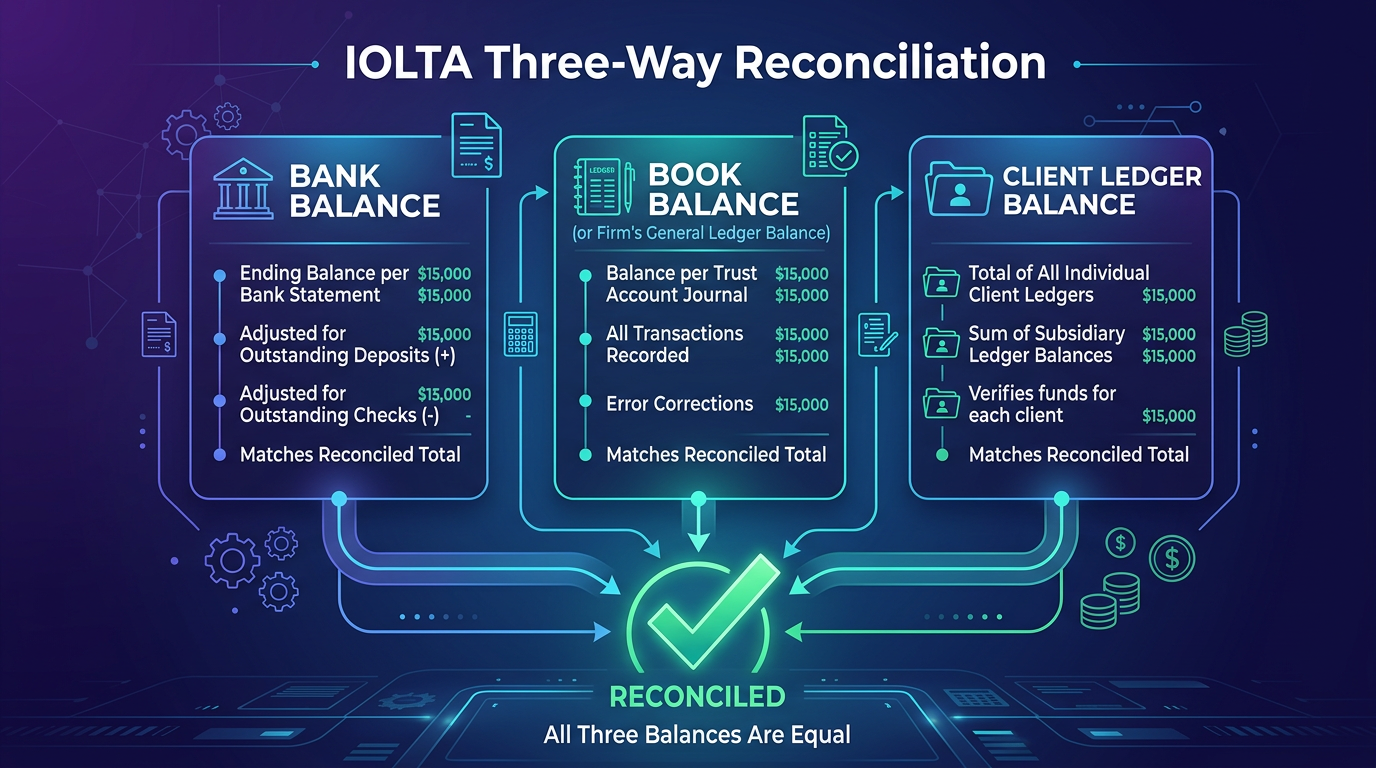

Every month, your bookkeeper must perform a three-way reconciliation that ties together:

All three numbers must match to the penny. If they don’t, you have a problem that needs to be resolved before the month closes — not next quarter, not at year-end. Immediately.

The violations that trigger bar investigations most frequently:

Critical compliance note: Most states require that trust account records be maintained for 5-7 years after the matter closes. Your bookkeeping system must archive individual client ledgers, not just aggregate account statements. A state bar auditor will ask for the ledger on a specific client from 2021 — and you need to produce it within days, not weeks.

Your practice management system (Clio, CosmoLex, or PracticePanther) should integrate directly with your accounting software to automate trust-to-operating transfers when fees are earned. Manual journal entries between trust and operating accounts are where most errors occur.

For a deeper dive into the reconciliation process, see our guide on IOLTA trust account reconciliation.

Partner compensation in a law firm isn’t payroll — it’s a financial architecture that determines how profits flow, how capital is tracked, and how the IRS views each partner’s income. Getting this wrong creates tax liability surprises, partner disputes, and year-end scrambles that consume dozens of billable hours.

These three terms are not interchangeable, and each has different tax treatment:

| Payment Type | What It Is | Tax Treatment | When Used |

|---|---|---|---|

| Distribution | Share of profits based on partnership % | Reported on K-1, subject to self-employment tax | Year-end or quarterly profit allocation |

| Draw | Advance against expected distributions | Reduces capital account, not deductible by firm | Monthly “salary equivalent” for partners |

| Guaranteed Payment | Fixed amount regardless of firm profit | Deductible by firm, ordinary income to partner | Base compensation for managing partners |

A partner receiving $25,000/month in draws plus a $100,000 guaranteed payment plus a 30% profit share needs three separate tracking mechanisms in your books. Most general bookkeepers set up a single “Partner Pay” account and create a mess that takes 40+ hours to untangle at tax time.

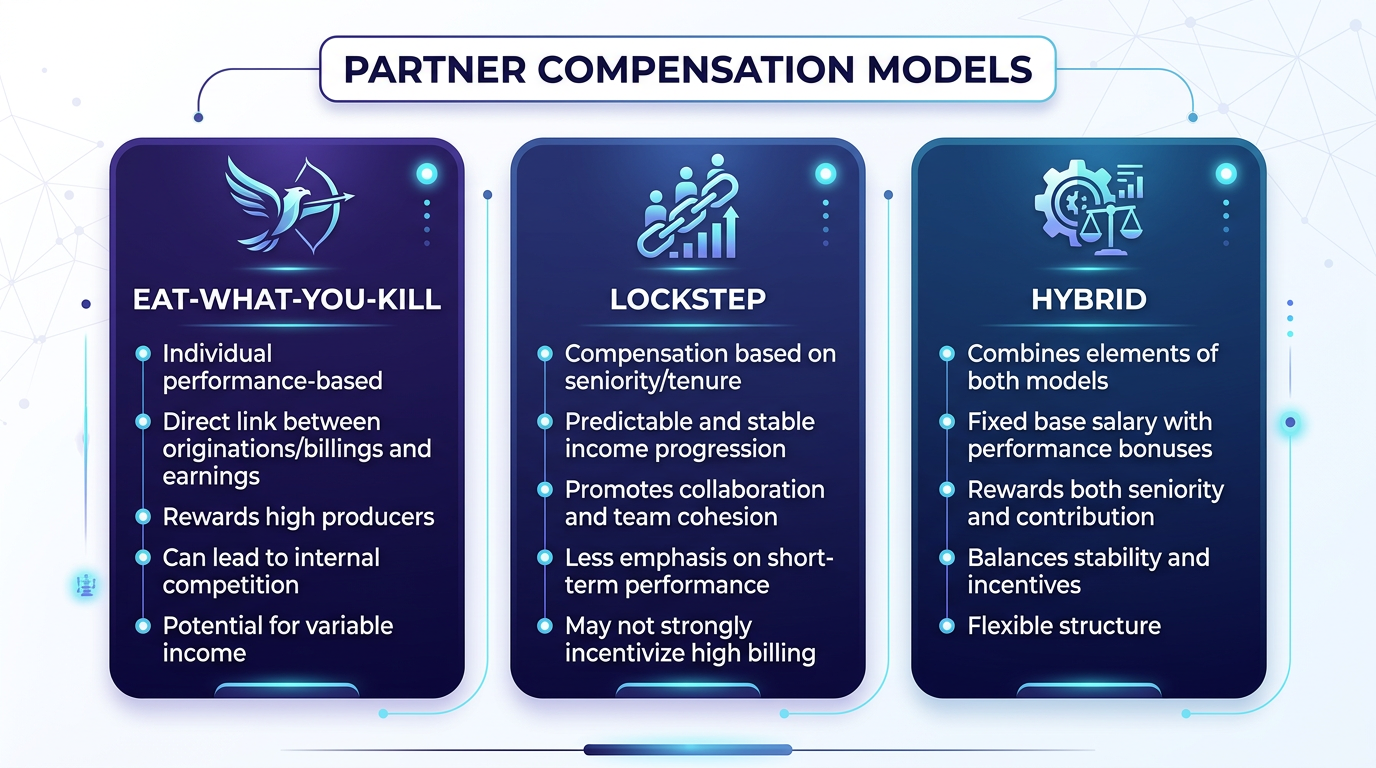

Your compensation model determines your entire chart of accounts structure:

Eat-what-you-kill firms allocate profits based on each partner’s individual origination and collections. This requires matter-level profitability tracking, origination credits, and sometimes split-credit rules when multiple partners contribute to a client relationship. Your bookkeeping system needs to track revenue attribution at the individual partner level.

Lockstep firms allocate profits based on seniority tiers, regardless of individual production. This is simpler from a bookkeeping perspective but requires clear documentation of each partner’s tier and the percentage allocation formula.

Hybrid models — the most common in mid-size firms — combine a base lockstep component with an eat-what-you-kill bonus pool. These are the most bookkeeping-intensive because you’re tracking both firm-wide profitability and individual partner metrics simultaneously.

Every equity partner has a capital account that tracks their ownership stake. The balance changes with:

A partner who joined with a $150,000 buy-in, was allocated $200,000 in profits, and took $180,000 in draws has a capital account balance of $170,000. This matters for K-1 preparation, partner departures, and firm valuation. Your bookkeeper must maintain a running capital account ledger for every equity partner.

For a comprehensive breakdown of distribution structures and equity tracking, see our guide to law firm partner distributions and equity.

Pro tip: Set up a separate equity section in your chart of accounts for each partner — not a single “Members’ Equity” line. When Partner A leaves the firm, you need to calculate their buyout from their individual capital account. If everything is lumped together, you’ll spend $5,000-$10,000 in CPA fees reconstructing individual balances from historical transactions.

How your firm bills clients determines how you recognize revenue — and getting this wrong creates phantom profits, surprise tax bills, and cash flow crises that hit in Q4 when it’s too late to course-correct.

The most straightforward model from a bookkeeping perspective, but with hidden complexity:

Flat fees create a revenue recognition timing issue. If a client pays $15,000 for a complete business formation package, when do you recognize that revenue?

The most challenging model to account for. Revenue is zero until the case resolves — which could be months or years. In the meantime, the firm is advancing costs (filing fees, expert witnesses, deposition transcripts) that may or may not be recovered.

Your bookkeeping system should track contingency matters as cost advances (an asset on the balance sheet), not expenses. When the case settles, the fee and cost recovery hit revenue simultaneously, and the cost advance asset is zeroed out.

Realization rate = Collected Revenue / Standard Billing Value

If your attorneys billed at standard rates for a total value of $4M, but after write-downs, write-offs, and client adjustments you collected $3.2M, your realization rate is 80%. The industry benchmark for well-managed firms is 85-92%.

Every point of realization improvement on $4M in standard billings is worth $40,000. That’s the kind of “aha” calculation that should drive your monthly financial review.

For a detailed comparison of billing approaches, read matter-based billing vs. flat fee accounting.

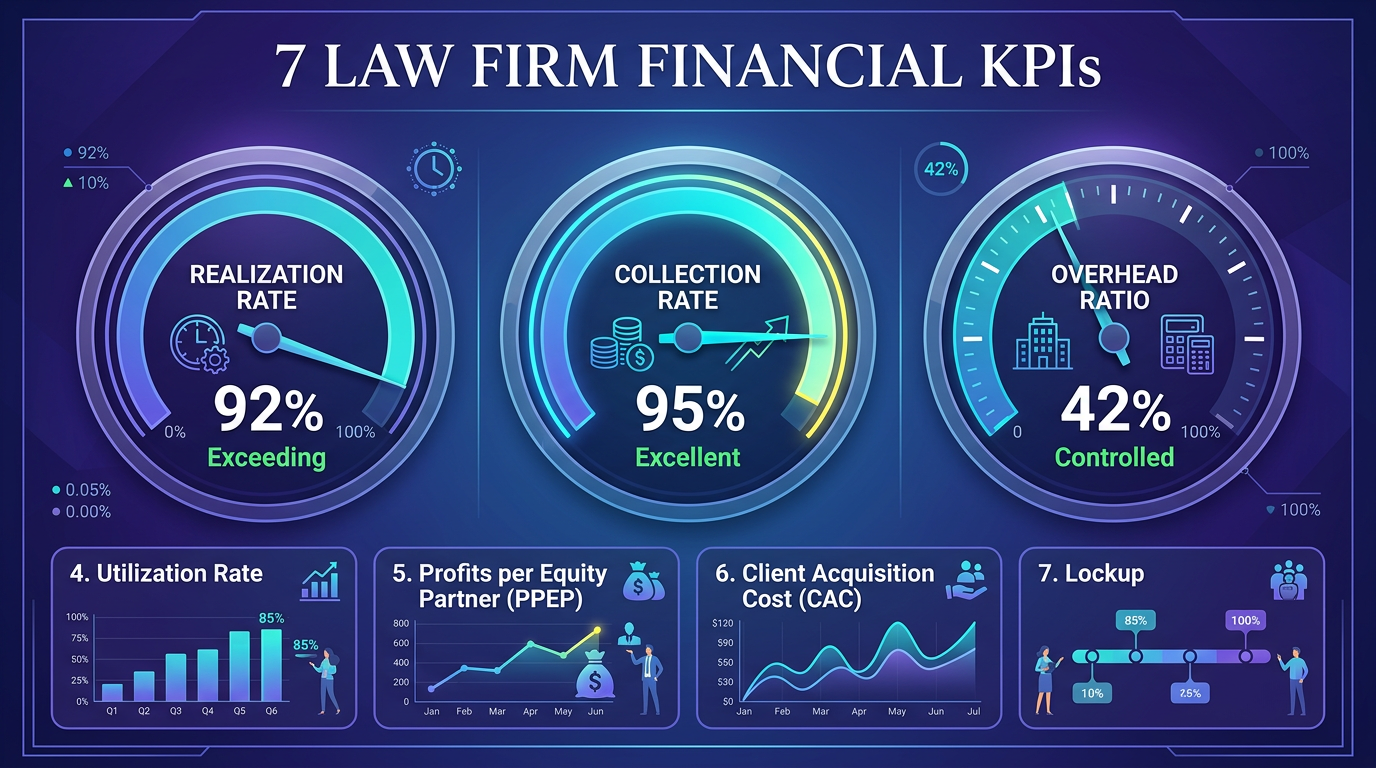

General business metrics (gross margin, EBITDA) don’t capture what makes a law firm profitable or fragile. These seven KPIs are the ones that managing partners at high-performing firms review monthly.

| KPI | Formula | Top-Quartile Benchmark | Warning Threshold |

|---|---|---|---|

| Realization Rate | Collected / Standard Value | 88-92% | Below 80% |

| Collection Rate | Collected / Billed | 95-98% | Below 90% |

| Cost Per Matter | Total Costs / Matters Closed | Varies by practice area | 20%+ above peer average |

| Revenue Per Lawyer | Gross Revenue / # Lawyers | $350K-$600K | Below $250K |

| Overhead Ratio | Non-lawyer Costs / Revenue | 35-42% | Above 50% |

| AR Aging (90+ days) | AR > 90 Days / Total AR | Below 10% | Above 20% |

| Profit Per Partner | Net Income / # Equity Partners | $250K-$500K+ | Below $150K |

Realization rate tells you if your pricing is right. If it’s below 80%, you’re either billing too high (and writing down), billing the wrong clients, or not managing scope creep.

Collection rate tells you if your clients are paying. A 90% collection rate means you’re doing $500K in work and only getting paid for $450K. At that point, you don’t need a new billing strategy — you need a collections process and possibly different clients.

Revenue per lawyer is the single best productivity metric. A firm with 8 lawyers and $2.8M in revenue generates $350K per lawyer. If one attorney is at $200K and another is at $500K, you have an underperformance problem that needs to be addressed — not by bookkeeping, but by management. Bookkeeping gives you the data to see it.

AR aging is your early warning system. When the percentage of receivables over 90 days climbs above 15%, you’re heading toward a cash flow crunch. The average law firm collects 73% of invoices within 30 days, 20% between 30-90 days, and writes off 7%. If your 90+ day bucket is growing, address it now — not at year-end.

Profit per partner (PPP) is what drives partner satisfaction, lateral hiring, and firm valuation. The Am Law 200 average PPP was $1.12M in 2025, but for firms in the $1M-$10M range, $250K-$500K is a strong target. Anything below $150K means your partners could earn more as senior associates at larger firms.

For a deep dive into each metric with tracking templates, see our guide on law firm financial KPIs.

Quick calculation: Pull your last 12 months of revenue and divide by the number of timekeepers (partners + associates). If that number is below $300K, you have capacity that isn’t generating revenue. Either you need more clients, your attorneys aren’t logging enough billable hours, or your realization rate is dragging revenue below what the time records suggest.

This decision affects your tax liability, your ability to understand firm economics, and your compliance with partnership tax rules. Most firms below $5M default to cash basis without analyzing whether it’s actually the right choice.

What it means: Revenue is recognized when cash hits the bank. Expenses are recognized when checks clear.

Advantages for law firms:

– Simplest to maintain — no accrued receivables, no deferred revenue tracking

– Tax timing flexibility — you can defer income by delaying invoices in December

– Aligns with how most attorneys think about money (“Did the client pay?”)

Disadvantages:

– Creates a distorted view of profitability. A firm that bills $800K in December but collects it in January shows a terrible December and an inflated January.

– WIP and unbilled receivables are invisible on cash-basis financials

– Doesn’t meet GAAP standards (matters if you’re ever seeking bank financing or valuation)

What it means: Revenue is recognized when earned (work performed), regardless of when cash arrives. Expenses are recognized when incurred.

Advantages for law firms:

– True picture of economic performance by period

– Tracks WIP and receivables as assets

– Required for firms with over $30M in gross receipts (IRC Section 448)

– Better for bank financing, partner buyouts, and firm valuation

Disadvantages:

– More complex bookkeeping — requires tracking unbilled WIP, accrued revenue, and deferred income

– Can create tax on income not yet collected (you pay tax on what you earned, even if the client hasn’t paid)

Under $5M revenue: Cash basis is usually fine. The simplicity outweighs the reporting limitations, and the tax deferral flexibility is valuable. Just make sure your practice management system tracks WIP separately so you have that data even if it’s not on your P&L.

$5M-$10M revenue: Consider accrual or modified accrual. At this size, the gap between cash-basis financials and economic reality becomes large enough to mislead management decisions. A hybrid approach — accrual for internal reporting, cash for tax returns — gives you the best of both worlds.

Above $10M revenue: Accrual is effectively mandatory for accurate management. The IRS requires accrual basis for C-corps with gross receipts over $30M, and partnerships of this size need GAAP-compliant financials for banking and valuation purposes.

For a detailed comparison with tax implications specific to law firms, read our guide to cash vs. accrual accounting for law firms.

The right software stack eliminates manual data entry, automates trust accounting compliance, and gives you real-time financial visibility. The wrong stack creates duplicate data entry, reconciliation nightmares, and a bookkeeper who spends 60% of their time on data wrangling instead of analysis.

Best for: Firms that want best-of-breed practice management with flexible accounting.

Watch out for: The Clio-QBO sync can create duplicate entries if not configured correctly. Your bookkeeper needs to understand which system is the source of truth for each transaction type. Invoices originate in Clio. Vendor bills originate in QBO. Trust transactions originate in Clio. Operating expenses originate in QBO.

Best for: Firms that want a single system handling everything — practice management, accounting, billing, and trust.

Watch out for: CosmoLex’s accounting module is less flexible than QBO for complex chart-of-accounts setups. If your firm has multiple entities, intercompany transactions, or complex partner compensation structures, you may outgrow it.

Best for: Firms already on QBO that need legal-specific trust accounting and billing without switching practice management systems.

Watch out for: LeanLaw is a billing and trust overlay, not a full practice management system. You’ll still need a separate tool for client intake, document management, and calendaring.

For a comprehensive comparison of all three options with feature matrices and pricing breakdowns, see our detailed guide on the best software for law firm bookkeeping.

Integration rule of thumb: The fewer manual journal entries your bookkeeper makes each month, the fewer errors end up in your financials. A well-integrated stack should automate at least 80% of transaction entries. If your bookkeeper is manually entering invoices from Clio into QuickBooks, you’re paying for double data entry — and getting double the error rate.

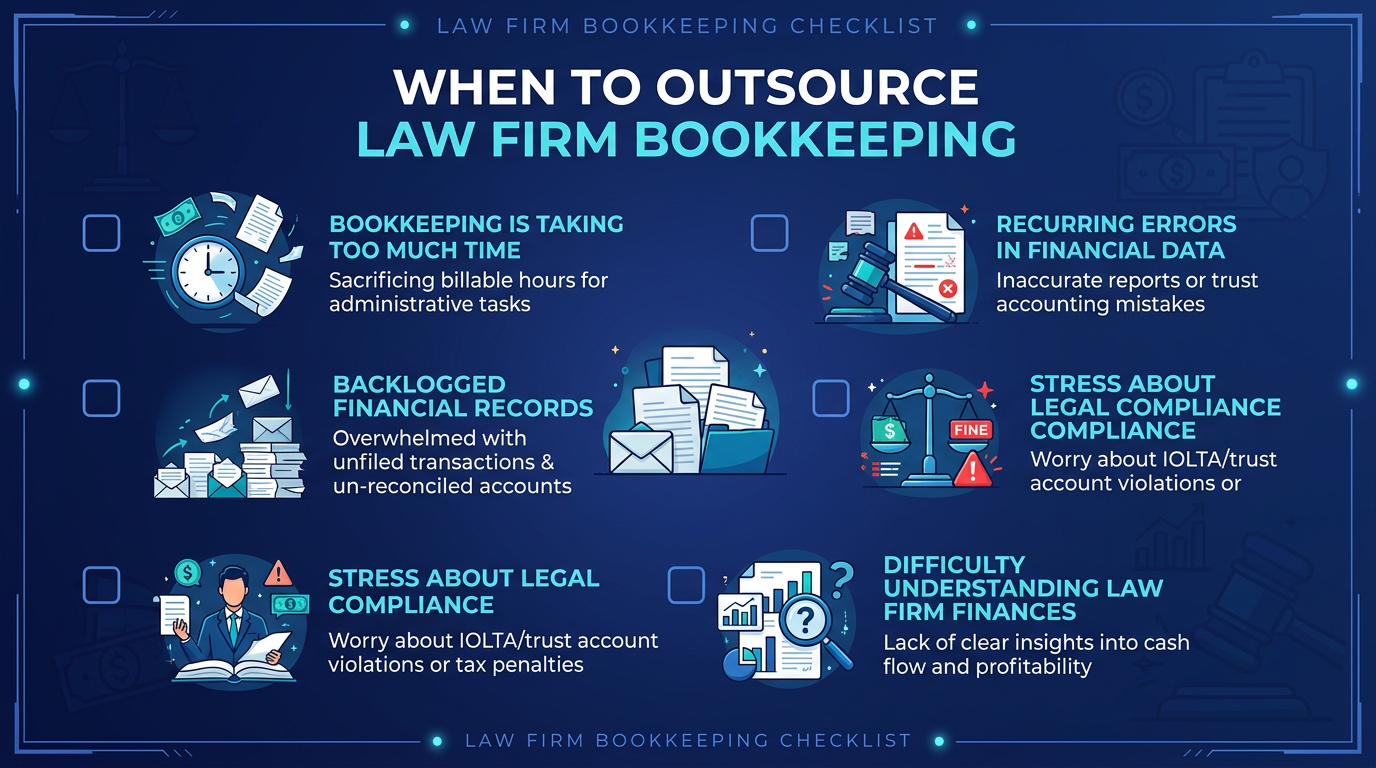

Not every firm needs to outsource. But if any of these scenarios sound familiar, it’s time to evaluate whether your current bookkeeping setup is a liability.

Your three-way trust reconciliation is more than 30 days behind. This is a compliance risk, not just an inconvenience. State bar audits don’t accept “we’ll catch up next month.”

Partner K-1s aren’t ready until March or April. If your bookkeeper can’t close the books by January 31, your partners’ personal tax returns are being delayed — and they’re paying their CPA for rush fees.

You don’t know your realization rate. If no one at your firm can tell you the gap between standard billing and actual collections within 5 minutes, your financial data isn’t organized for management decisions.

Your bookkeeper doesn’t understand trust accounting. If they’ve ever asked “Can we just put everything in one account?” — that’s your answer.

Month-end close takes more than 10 business days. A well-run law firm should close books within 5-7 business days. If it’s taking longer, the process is broken.

| Cost Category | In-House Bookkeeper | Outsourced (Specialized) |

|---|---|---|

| Base salary/fee | $55,000-$75,000/year | $1,500-$3,500/month ($18K-$42K/year) |

| Benefits & taxes | $15,000-$22,000/year | Included |

| Software licenses | $2,400-$6,000/year | Usually included |

| Training & supervision | 5-10 hrs/month of partner time | Included |

| Trust accounting expertise | Rarely (requires legal bookkeeping experience) | Standard (specialized firms) |

| Coverage for PTO/sick | None (books stop) | Continuous (team-based) |

| Total annual cost | $72,000-$103,000 | $18,000-$42,000 |

For a $3M-$5M law firm, outsourcing typically saves $30,000-$60,000 per year compared to an in-house hire — while getting a team with specific law firm bookkeeping expertise instead of a single generalist.

Not every outsourced bookkeeping firm can handle law firm accounts. Ask these questions before signing:

The ROI calculation is straightforward: take your managing partner’s effective hourly rate, multiply by the hours they spend on financial administration each month, and compare that to the cost of outsourcing. A managing partner billing at $450/hour who spends 8 hours per month on bookkeeping oversight is burning $3,600/month in opportunity cost — more than the cost of a specialized outsourced team.

For more detail on the full outsourcing evaluation, see our complete outsourced bookkeeping guide and our comparison of in-house vs. outsourced bookkeeping.

Ready to get your law firm’s books right? Steph’s Books specializes in bookkeeping for law firms — including IOLTA trust reconciliation, partner distributions, and the financial KPIs that drive profitability. Schedule a free consultation and see what clean books look like for your firm.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.