Most law firms pick an accounting method when they file their first tax return — and never revisit the decision. That default choice quietly shapes how you recognize revenue, when you pay taxes, and whether your financial statements reflect economic reality or just bank activity.

For firms billing $1M–$10M annually, the gap between cash and accrual basis isn’t academic. It determines whether your December financials show the $180,000 in outstanding receivables you’ve already earned, or whether that revenue is invisible until checks clear in January. It affects partner compensation timing, tax planning flexibility, and whether your bank will underwrite that line of credit.

This guide breaks down both methods with law-firm-specific examples, covers the IRS requirements you need to know, and gives you a clear recommendation based on your firm’s size and structure. For a broader look at law firm financial management, see our law firm bookkeeping guide.

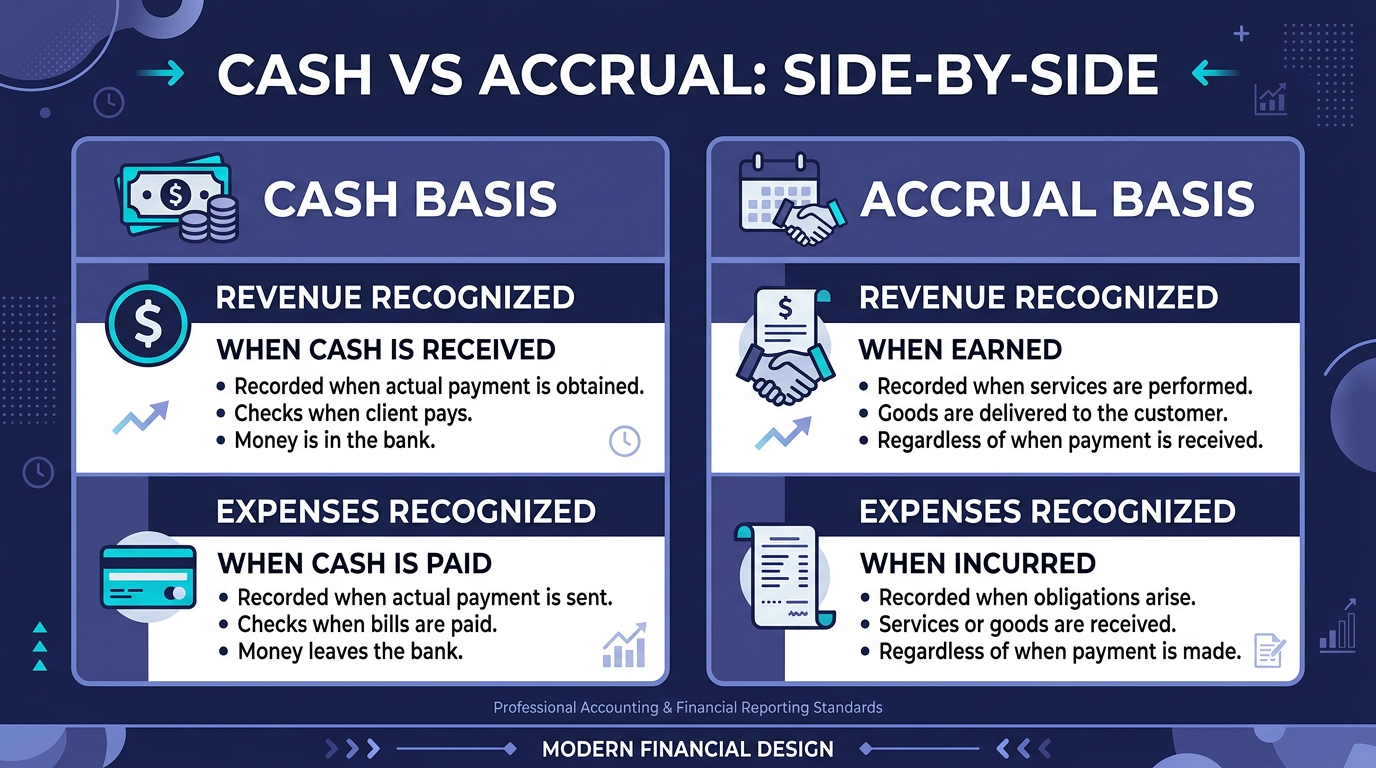

Cash basis is straightforward: you recognize revenue when payment hits your bank account and expenses when you actually pay them. Work-in-progress, outstanding invoices, and accrued liabilities don’t appear on your books until money moves.

Your litigation team completes a $45,000 matter in November. You send the invoice on November 28. The client pays on January 15.

Under cash basis:

– November books: $0 revenue from this matter

– December books: $0 revenue from this matter

– January books: $45,000 revenue recognized

Meanwhile, you paid the $6,200 expert witness fee in October. Under cash basis, that expense hit October — two months before the related revenue appears. Your October P&L overstates expenses, and your January P&L overstates profit. Neither month reflects the actual economics of the engagement.

Pro Tip: Cash basis can mask serious collection problems. If your firm bills $3M but only collects $2.4M, cash-basis statements show $2.4M in revenue and no indication that $600K is aging in receivables. Track your realization rate and collection rate separately, regardless of accounting method.

Accrual basis recognizes revenue when you earn it (when services are performed) and expenses when you incur them (when the obligation arises) — regardless of when cash changes hands.

Same scenario: $45,000 matter completed in November, invoiced November 28, paid January 15. The $6,200 expert witness fee was incurred in October.

Under accrual basis:

– October books: $6,200 expense recognized (expert witness obligation incurred)

– November books: $45,000 revenue recognized (services completed and invoiced)

– January books: Cash received — the receivable converts to cash, but no new revenue is recorded

Now your November financials show $45,000 in revenue offset by the allocated costs, giving you an accurate picture of that matter’s profitability.

Accrual basis delivers advantages that matter more as firm complexity grows:

| Factor | Cash Basis | Accrual Basis |

|---|---|---|

| Revenue recognition | When payment received | When services performed |

| Expense recognition | When payment made | When obligation incurred |

| Receivables on balance sheet | Not tracked | Yes — full A/R visibility |

| WIP tracking | Not reflected | Can be tracked as an asset |

| Tax timing | Defer revenue by delaying collection | Revenue recognized when earned, regardless of collection |

| Financial statement accuracy | Reflects cash flow only | Reflects economic activity |

| Complexity | Lower — fewer adjusting entries | Higher — requires month-end accruals |

| Bookkeeping cost | Lower | 15–25% higher due to adjusting entries |

| Bank/lender preference | Acceptable for small credit lines | Required for most commercial lending |

| Best for | Solo and small firms (<$5M) | Mid-size and large firms (>$5M) |

Important: Regardless of which method you use for tax purposes, nothing stops you from running internal management reports on an accrual basis. Many firms file taxes on cash basis but operate internally on accrual. This is called tax-basis vs. book-basis reporting, and it’s more common than most managing partners realize.

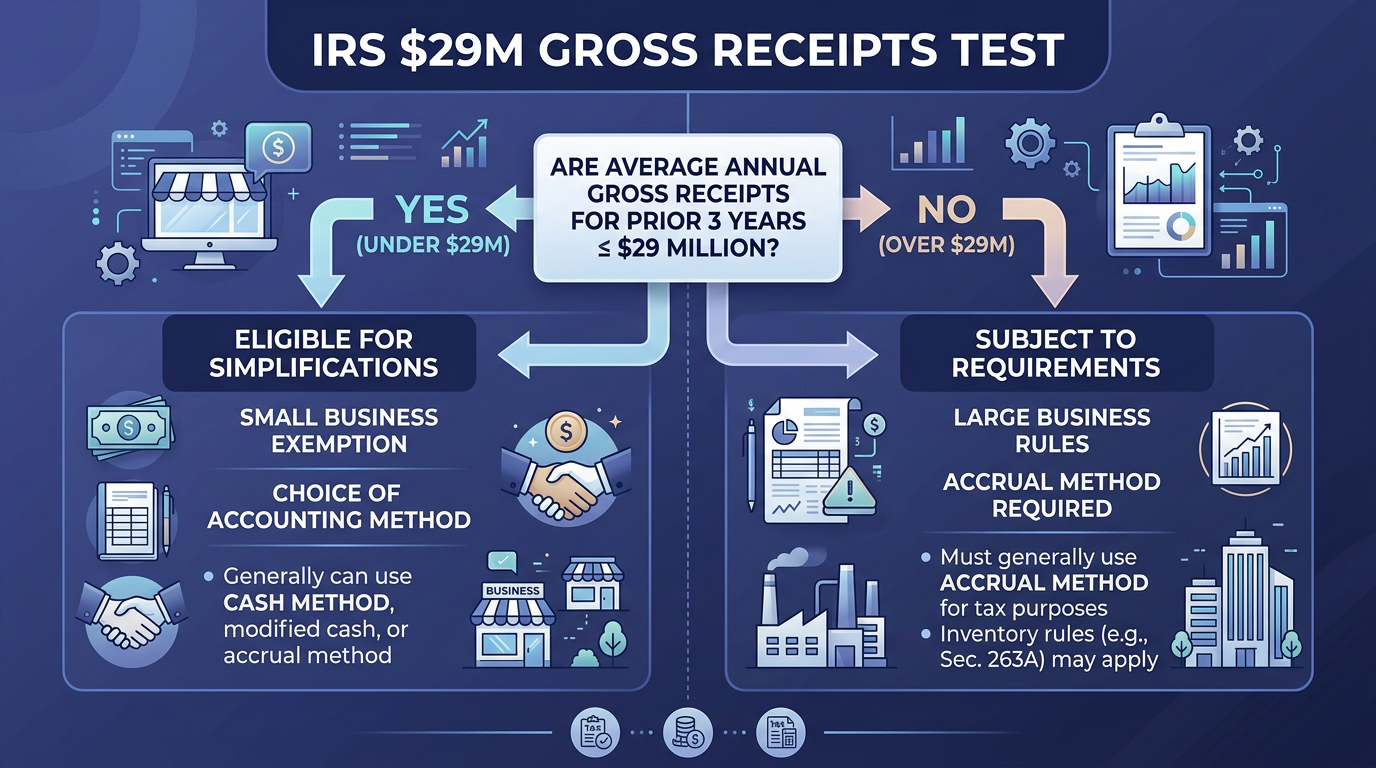

The IRS doesn’t let every business choose freely. IRC Section 448 restricts the cash method for certain entities.

C corporations and partnerships with C corporation partners cannot use the cash method if their average annual gross receipts exceed $29 million (for tax years beginning in 2024–2025, adjusted annually for inflation). This is the “gross receipts test” under IRC §448(c).

Most law firms operate as one of these structures:

The practical takeaway for most law firms: If you’re structured as an S corp, LLP, or sole proprietorship — which covers the vast majority of firms billing $1M–$10M — the IRS imposes no requirement to use accrual. Your choice is purely strategic.

Even if you’re below the threshold, certain activities trigger mandatory accrual treatment:

Your accounting method is one of the most powerful — and most overlooked — tax planning levers available to a law firm.

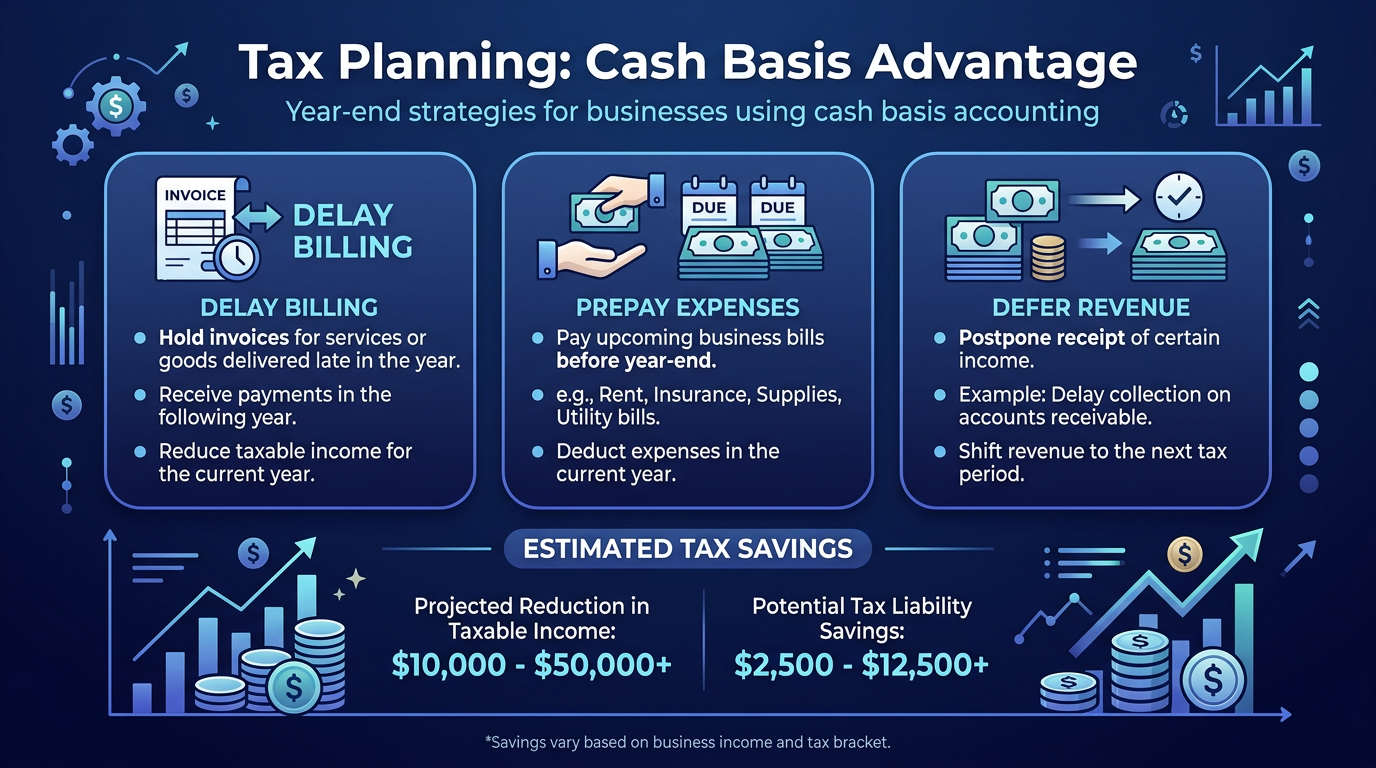

Year-end acceleration of expenses. Prepay January rent in December, stock up on office supplies, pay outstanding vendor invoices before December 31. Each accelerated payment creates a current-year deduction.

Revenue deferral. Hold December invoices until January, or hold deposits received late in December. This pushes taxable revenue into the next year. A firm with $200,000 in December billings that delays invoicing until January 2 defers that entire amount.

Estimated tax management. Cash basis gives you more control over quarterly income fluctuations since you can time collections and payments to smooth taxable income.

Pro Tip: The year-end revenue deferral strategy has limits. If you routinely delay invoicing to shift revenue, the IRS may scrutinize the practice under the constructive receipt doctrine. Revenue is taxable when you have an unrestricted right to collect it — not just when the check arrives. Consult your tax advisor before implementing aggressive deferral strategies.

Bad debt deductions. Accrual-basis firms can deduct genuinely uncollectible receivables. Cash-basis firms can’t — they never recognized the revenue, so there’s nothing to deduct.

Expense accrual timing. Accrue bonuses, vacation pay, and other liabilities in the year they relate to, even if paid in the following year (subject to the all-events test and economic performance rules).

Section 481(a) adjustment. If you switch methods, the IRS requires a cumulative adjustment to prevent income from being permanently skipped or double-counted. Depending on direction, this can be spread over multiple years — creating a planning opportunity.

You’re not limited to a pure cash or pure accrual approach. Many law firms use a modified cash basis (sometimes called “hybrid” or “OCBOA” — Other Comprehensive Basis of Accounting).

A modified cash basis firm uses cash accounting for day-to-day transactions but applies accrual treatment to specific items. Common modifications for law firms:

Modified cash gives you the tax timing benefits of cash basis (defer revenue until collected, accelerate deductions) while producing financial statements that are closer to economic reality. Your balance sheet shows real assets and major liabilities, even though revenue recognition follows cash rules.

The AICPA recognizes modified cash basis as an acceptable framework for compiled and reviewed financial statements, which means your CPA can issue formal statements on this basis without qualification.

Recommended: Cash basis.

Simplicity outweighs everything else at this scale. You likely don’t have a dedicated bookkeeper, and your banking relationships don’t require accrual-basis statements. Track receivables informally in your practice management software.

Recommended: Modified cash basis for management, cash basis for tax.

At this size, you need better financial visibility but still benefit from cash-basis tax treatment. Run modified cash internally — capitalize assets, accrue payroll, track receivables — but file taxes on cash basis. This gives you meaningful management reports without increasing your tax burden.

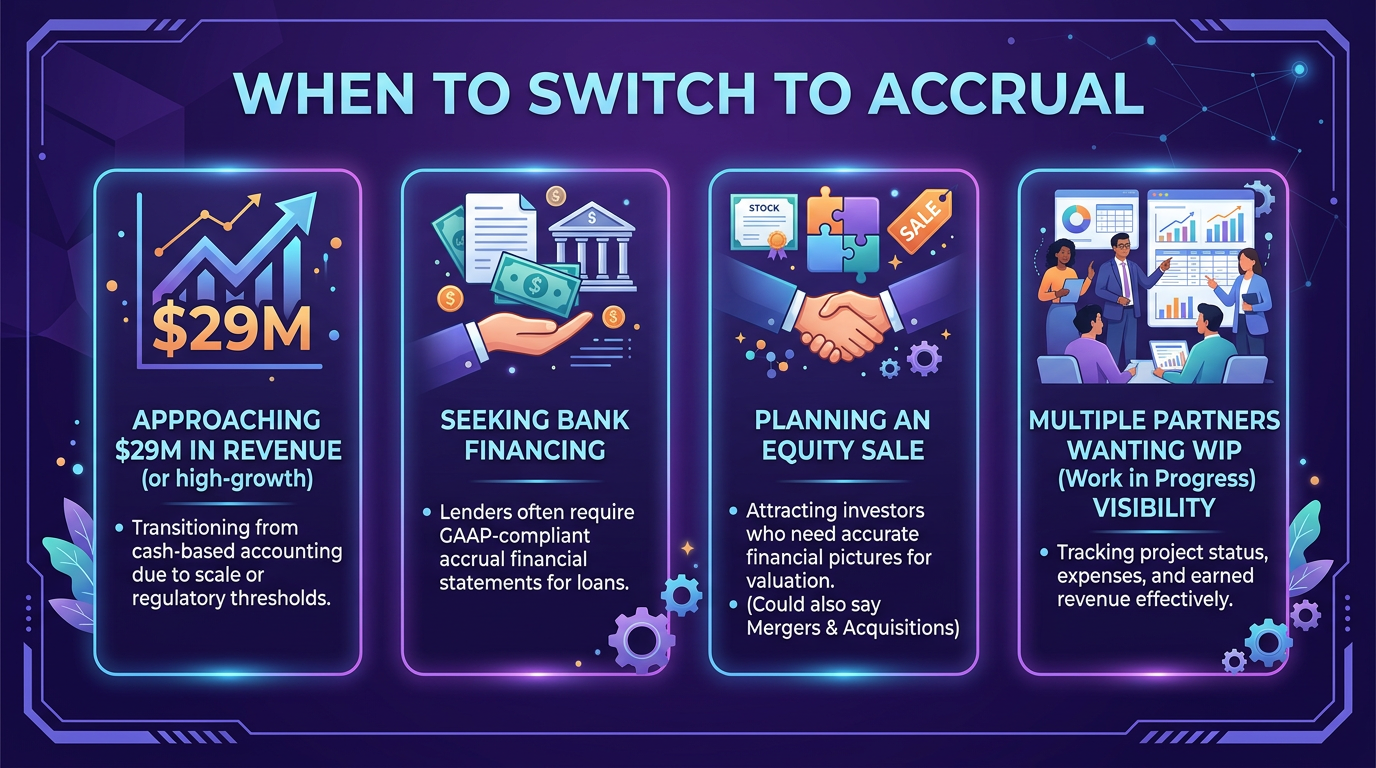

Recommended: Accrual basis for management, evaluate for tax.

Partner compensation discussions, lateral hiring decisions, and practice-group profitability analysis all require accrual data. Your bank likely wants accrual statements for credit facilities. You may still file taxes on cash basis (if your entity structure allows it), but your internal accounting should be accrual.

Recommended: Full accrual basis.

At this scale, you need accrual for external reporting, lending relationships, M&A due diligence, and accurate partner capital accounting. The bookkeeping cost premium is negligible relative to revenue.

If you’re switching from cash to accrual (or vice versa), here’s what to expect.

This is the most common direction. The key adjustments:

Less common but sometimes done for tax optimization. The 481(a) adjustment here is negative (decreases taxable income), and the IRS requires you to take the full benefit in year one — no spreading. This can create a significant one-time tax benefit.

Best timing: The beginning of a tax year with relatively low receivables. Converting when receivables are at their annual peak (often December for litigation firms) maximizes the 481(a) adjustment and the associated tax hit.

Get professional help. Method changes involve Form 3115, transition adjustments, and multi-year tax implications. This is not a DIY project — work with a CPA who has experience with professional services firm conversions.

Ready to get your firm’s accounting method right? Whether you’re evaluating a switch from cash to accrual or need help setting up modified cash reporting, our team specializes in bookkeeping for law firms. Schedule a free consultation →

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.