A four-partner litigation firm in Dallas ran into a $140,000 problem at tax time: two equity partners had been over-distributed by a combined $93,000 relative to their profit allocations, while a third partner’s capital account showed a negative balance that nobody could explain. The culprit wasn’t fraud — it was a general bookkeeper who tracked partner draws the same way she tracked owner distributions at a single-member LLC. One QuickBooks equity account, one distribution line, no capital account reconciliation.

Law firm partner distributions are structurally different from standard owner draws. When you have three to eight equity partners, each with different compensation arrangements, guaranteed payments, capital contributions, and profit-sharing percentages, your bookkeeping system needs to track every dollar flowing to each partner individually — because the IRS requires it on each partner’s K-1, and your operating agreement probably defines it in ways your bookkeeper has never seen.

This guide breaks down the compensation models, tax implications, capital account mechanics, and QuickBooks setup that managing partners at firms between $1M and $10M need to get right. If your current system involves a single “partner draws” account and year-end guesswork, you’re leaving your firm exposed to both tax penalties and partner disputes.

The way your firm divides profits shapes everything downstream — from how you track distributions in your books to what shows up on each partner’s K-1. There are three dominant models, and most firms use some variation or blend of them.

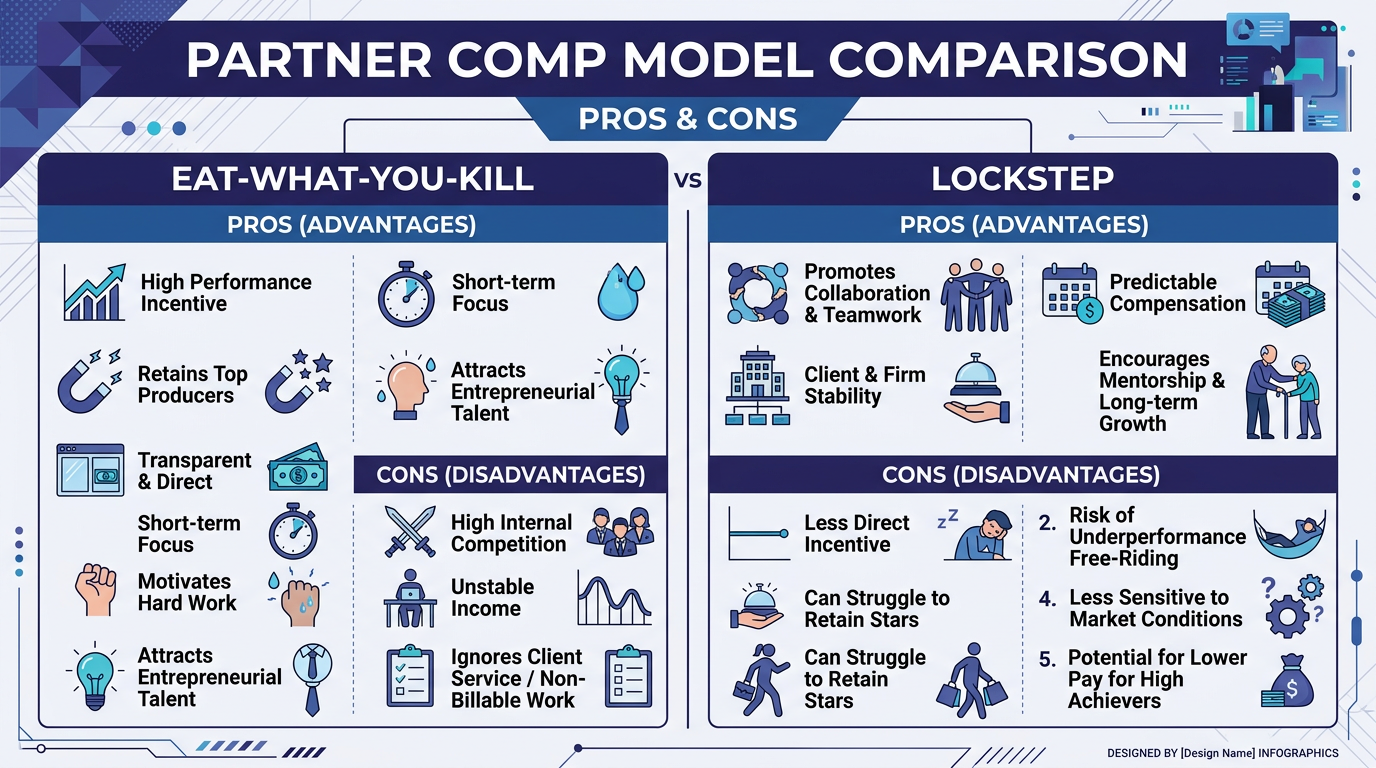

Under this model, each partner’s compensation is driven primarily by the revenue they personally originate and collect. A partner who brings in $1.2M in collected fees and the firm’s overhead allocation is 40% takes home roughly $720,000 (minus their share of firm-wide costs). This model rewards rainmakers but can create friction around shared clients, cross-selling, and matters where origination credit is unclear.

From a bookkeeping standpoint, eat-what-you-kill requires matter-level revenue attribution tied to individual partners. Your accounting system must track origination credit, working attorney credit, and collected revenue at the partner level — not just the firm level.

Lockstep ties compensation to tenure. A partner at year five earns a defined percentage, a partner at year ten earns more, and so on. This model is common in large firms with institutional clients where no single partner “owns” the relationship. It rewards loyalty and reduces internal competition but can frustrate high-performing junior partners.

Bookkeeping under lockstep is more straightforward: profit allocations follow a fixed schedule defined in the partnership agreement. The challenge is keeping the schedule current as partners join, leave, or move between tiers.

Most mid-size firms land here. A hybrid model blends objective metrics (origination, collections, billable hours) with subjective factors (mentoring, firm leadership, business development effort) and a seniority baseline. The managing partner or compensation committee assigns final allocations, often annually.

Hybrid models are the hardest to track because the allocation percentages change every year. Your bookkeeping system needs to handle mid-year adjustments when a partner’s allocation shifts after the annual compensation review.

| Factor | Eat-What-You-Kill | Lockstep | Hybrid |

|---|---|---|---|

| Basis | Individual origination and collections | Seniority and tenure | Blended metrics + committee discretion |

| Bookkeeping complexity | High — requires matter-level attribution | Low — fixed schedule | Medium to high — annual recalculation |

| Partner disputes | Frequent (origination credit conflicts) | Rare (formula is predetermined) | Moderate (subjective component) |

| Rainmaker retention | Strong | Weak | Moderate |

| Collaboration incentive | Low | High | Moderate |

| K-1 preparation | Complex (variable allocations) | Simple (fixed percentages) | Moderate (annual percentage updates) |

| Best fit | Firms under $5M with entrepreneurial culture | Established firms with institutional clients | Most mid-size firms ($2M-$10M) |

Important: Your partnership or operating agreement is the controlling document for how profits are allocated — not your bookkeeper’s assumptions. Before setting up any tracking system, pull out the agreement and confirm the exact allocation formula, guaranteed payment terms, and capital contribution requirements. If the agreement is vague on any of these points, get it amended before tax season.

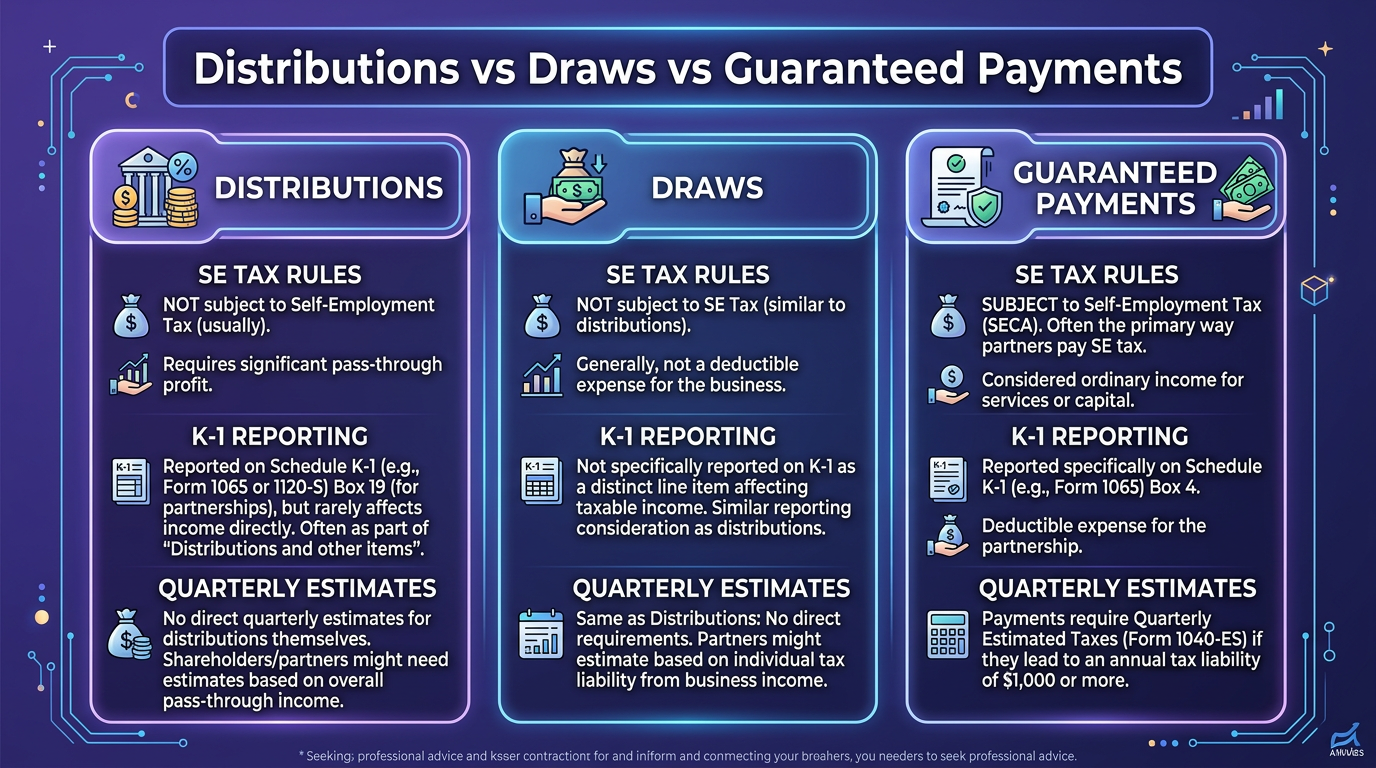

These three terms get used interchangeably in most law firms. They are not the same thing, and the IRS treats them very differently.

A distribution is a payment of profits to a partner based on their ownership percentage or profit-sharing allocation. Distributions are not deductible by the partnership — they flow through to the partner’s individual return via Schedule K-1 and are taxed as ordinary income (plus self-employment tax in most cases). The partnership itself pays no income tax.

Key rule: distributions reduce a partner’s capital account. If a partner is allocated $300,000 in profits and takes $350,000 in distributions, their capital account drops by $50,000. If the capital account goes negative, the partner may be required to contribute capital back to the firm — or face tax consequences on the excess distribution.

A guaranteed payment is compensation paid to a partner regardless of whether the firm earns a profit. Think of it as a partner’s “salary” — it’s determined without regard to partnership income. Under IRC Section 707(c), guaranteed payments are deductible by the partnership as an expense and reported separately on the partner’s K-1 (Box 4).

For law firms, guaranteed payments are common for:

The critical bookkeeping distinction: guaranteed payments reduce firm profits before the remaining profits are allocated among partners. If your firm earns $2M and pays $200,000 in guaranteed payments, only $1.8M is available for profit allocation.

A draw is an advance against expected profits — the partner takes money now and it’s reconciled against their actual profit allocation at year-end. Draws are not taxable events themselves. They simply reduce the partner’s capital account like any distribution.

The danger is over-drawing. A partner who takes $30,000 per month in draws ($360,000 annually) but is only allocated $280,000 in profits has been over-distributed by $80,000. That $80,000 must be reconciled — typically by reducing future draws, requiring a capital contribution, or adjusting the following year’s allocation.

Pro Tip: Set up a quarterly draw reconciliation rather than waiting until year-end. Compare each partner’s year-to-date draws against projected profit allocations at the end of every quarter. This gives you three opportunities to adjust draw amounts before tax season creates a crisis. Most partnership disputes we see stem from year-end surprises that could have been caught in Q2.

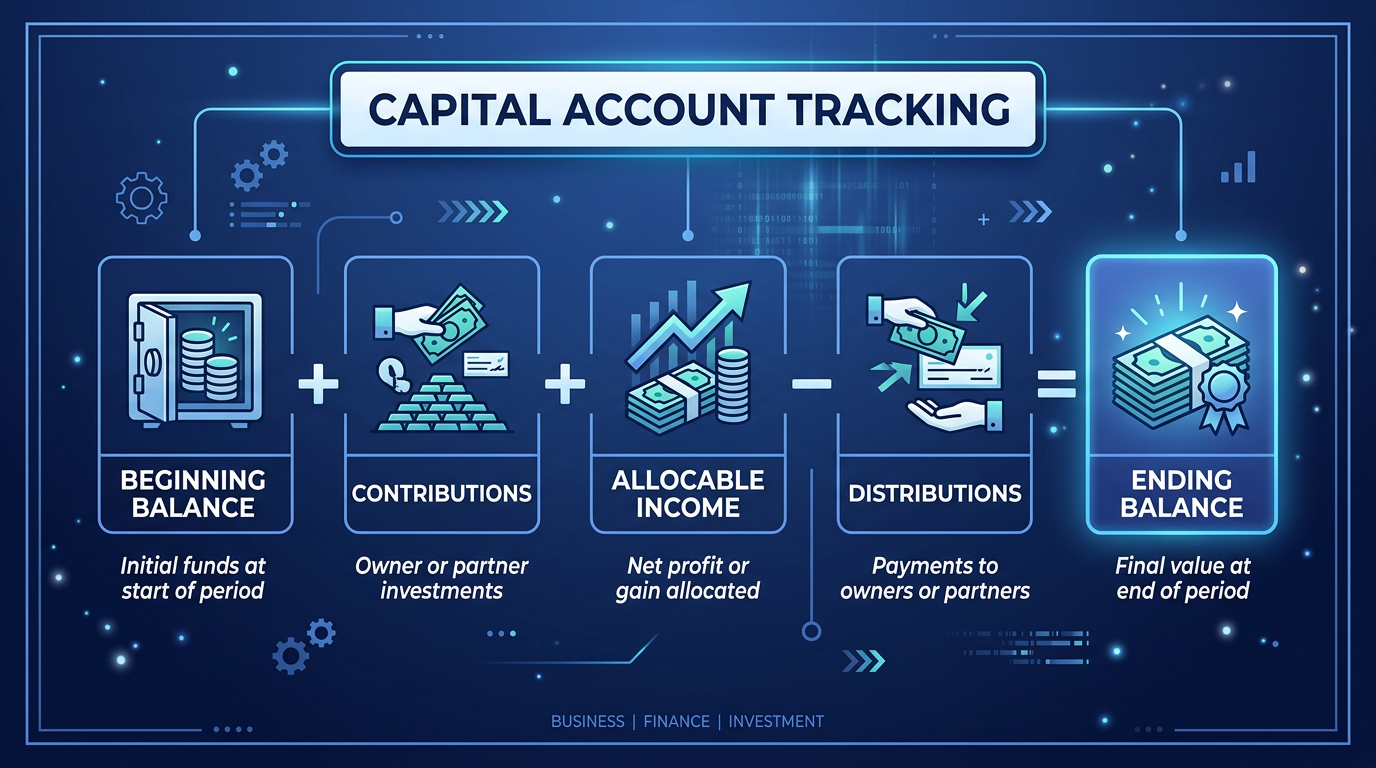

Every partner in a law firm has a capital account — a running balance that reflects their economic interest in the firm. Getting capital accounts wrong doesn’t just create partner disputes; it creates incorrect K-1s, which creates IRS problems.

When distributions exceed a partner’s accumulated profits and contributions, their capital account goes negative. This is more common than most managing partners realize — especially in firms where partners take monthly draws based on last year’s income while current-year profits are declining.

A negative capital account creates two problems:

Track capital accounts monthly, not annually. A running monthly balance lets you catch negative trends before they become year-end emergencies.

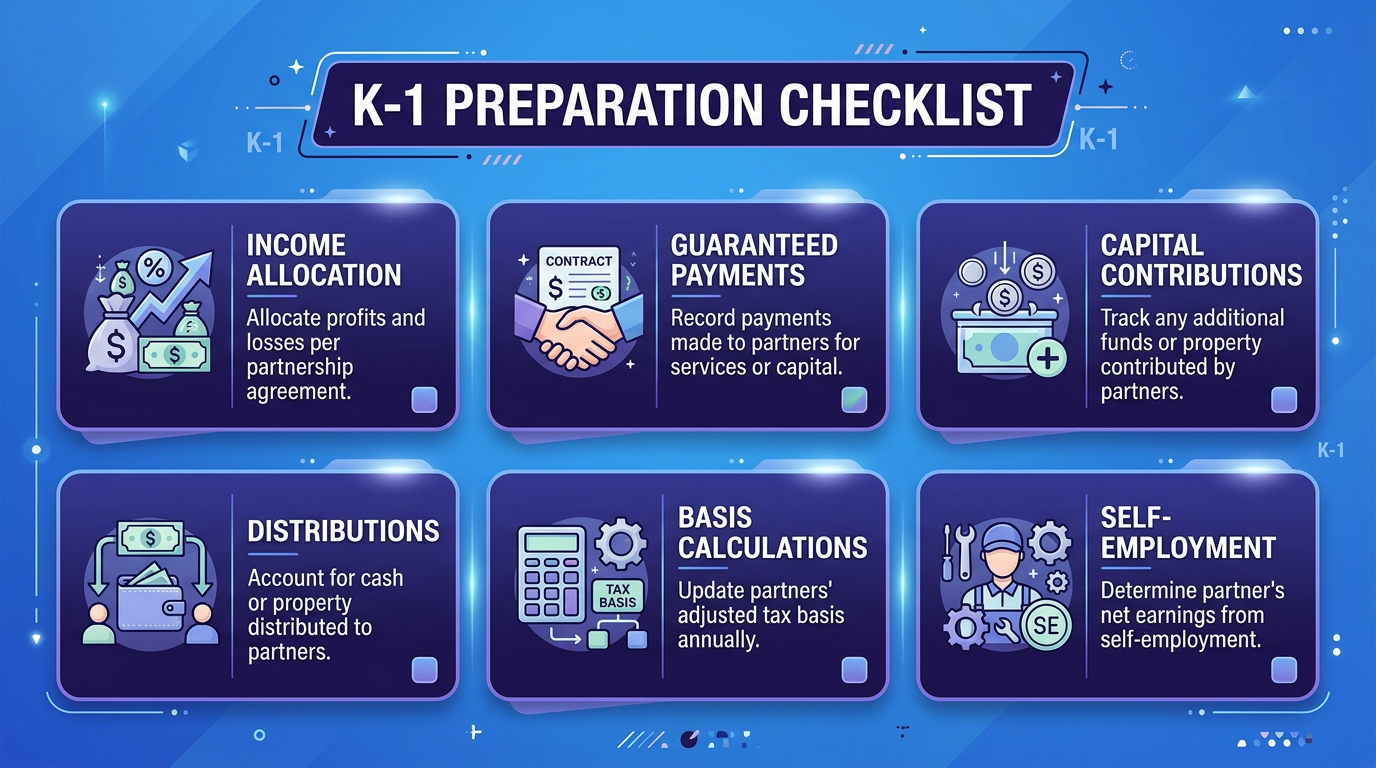

Schedule K-1 (Form 1065) reports each partner’s share of partnership income, deductions, credits, and other items. For a multi-partner law firm, K-1 preparation is where every bookkeeping shortcut from the prior year comes home to roost.

Before filing, run this check: each partner’s ending capital account on Schedule L should equal their beginning capital account, plus their profit allocation, plus contributions, minus distributions, minus their share of losses. If it doesn’t balance, there’s a posting error somewhere — usually a draw that was recorded to the wrong partner or a guaranteed payment that was double-counted.

For firms with five or more equity partners, this reconciliation should be completed by January 31 at the latest. Partners need their K-1s to file individual returns, and a math error discovered in March creates a cascade of amended returns.

QuickBooks Online can handle multi-partner tracking, but not with the default chart of accounts. You need a structured equity section that mirrors your partnership agreement.

For each partner, create this sub-account hierarchy under equity:

Repeat for each equity partner. Yes, a five-partner firm will have 20 equity sub-accounts. That granularity is what makes K-1 preparation take hours instead of weeks.

When Partner A takes a $25,000 monthly draw:

Do not run partner draws through payroll. Partners in a partnership are not employees — they don’t receive W-2s, and running draws through payroll creates incorrect payroll tax withholding.

When the firm pays a $15,000 monthly guaranteed payment to a non-equity partner:

Guaranteed payments hit the P&L as an expense. Distributions do not. This distinction is critical for accurate profit reporting.

After closing the books, allocate net income to each partner per the operating agreement:

This journal entry moves profits from the firm-level retained earnings into each partner’s equity section, which feeds directly into K-1 preparation.

Pro Tip: Use QBO’s class tracking feature to tag every revenue transaction with the originating partner. This gives you real-time origination reports without a separate spreadsheet — and it’s essential for eat-what-you-kill and hybrid compensation models. Enable classes under Settings > Advanced, and require class assignment on every income transaction.

If your firm uses Clio, PracticePanther, or CosmoLex, connect it to QBO so that billed time flows into accounts receivable automatically. The practice management system handles matter-level billing; QBO handles the financial accounting and partner equity tracking. Trying to do both in one system leads to compromises in both. For a deeper look at which software combinations work best, see our guide to law firm bookkeeping software.

After working with dozens of law firms on partner accounting, these are the errors we see most frequently — and every one of them is preventable with proper bookkeeping setup.

This is the most common mistake, and it makes K-1 preparation nearly impossible without reconstructing every transaction for the year. Each partner needs their own equity sub-accounts. Period.

Guaranteed payments are a firm expense. Distributions are not. Recording guaranteed payments as distributions overstates firm profit and understates the receiving partner’s reportable income. The IRS notices this discrepancy because Box 1 and Box 4 on the K-1 won’t reconcile with the partnership return.

Annual capital account reconciliation means you discover problems in January when K-1s are due. Monthly tracking means you catch a partner’s negative capital account trend in July and have time to adjust draws.

The partnership agreement defines profit allocation, not the bookkeeper’s interpretation of “equal split.” If the agreement says profits are split 40/35/25 after guaranteed payments, that’s what your books must reflect — even if the partners informally agreed to something different over lunch.

Partners are not employees. Running draws through payroll creates W-2s that shouldn’t exist, payroll tax obligations that don’t apply, and a mess at tax time that requires amended payroll returns and corrected K-1s. Use equity draw accounts, not payroll.

Year-end is too late to discover that one partner has been over-distributed by $100,000. Quarterly reconciliation of draws against projected allocations prevents the single most common source of partner disputes in law firms.

Partner distribution tracking doesn’t exist in isolation. It’s one component of a comprehensive law firm bookkeeping system that includes trust accounting, revenue recognition, and financial reporting. Firms that get the partner equity piece wrong typically have other bookkeeping gaps — because the same complexity that makes distributions difficult makes everything else harder too.

If your firm is still evaluating whether cash or accrual accounting better fits your practice, that decision directly affects when partner profits are recognized and distributed. Our cash vs. accrual accounting guide for law firms walks through the implications for multi-partner firms specifically.

Related Reading:

Ready to get your partner distributions and equity tracking right? Steph’s Books provides specialized bookkeeping for law firms — including capital account management, K-1 preparation support, and monthly partner equity reconciliation. Schedule a consultation →

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.