A $4M litigation firm switched three practice areas from hourly billing to flat fee in Q1 2025. Revenue stayed flat — but their bookkeeper spent six months untangling misclassified income, phantom WIP balances, and realization rate reports that no longer made sense. The billing model changed. The accounting never caught up.

The debate between matter-based billing vs flat fee isn’t just a pricing strategy decision. It’s an accounting architecture decision that affects how your firm recognizes revenue, tracks work in progress, calculates profitability, and reports to partners.

This guide breaks down the accounting implications of every billing model used in law firms between $1M and $10M — and shows you how to set up your books so the numbers match reality.

Law firms operate under four billing structures, each with distinct accounting treatment that determines how you configure QBO, what you track in your practice management system, and when revenue counts.

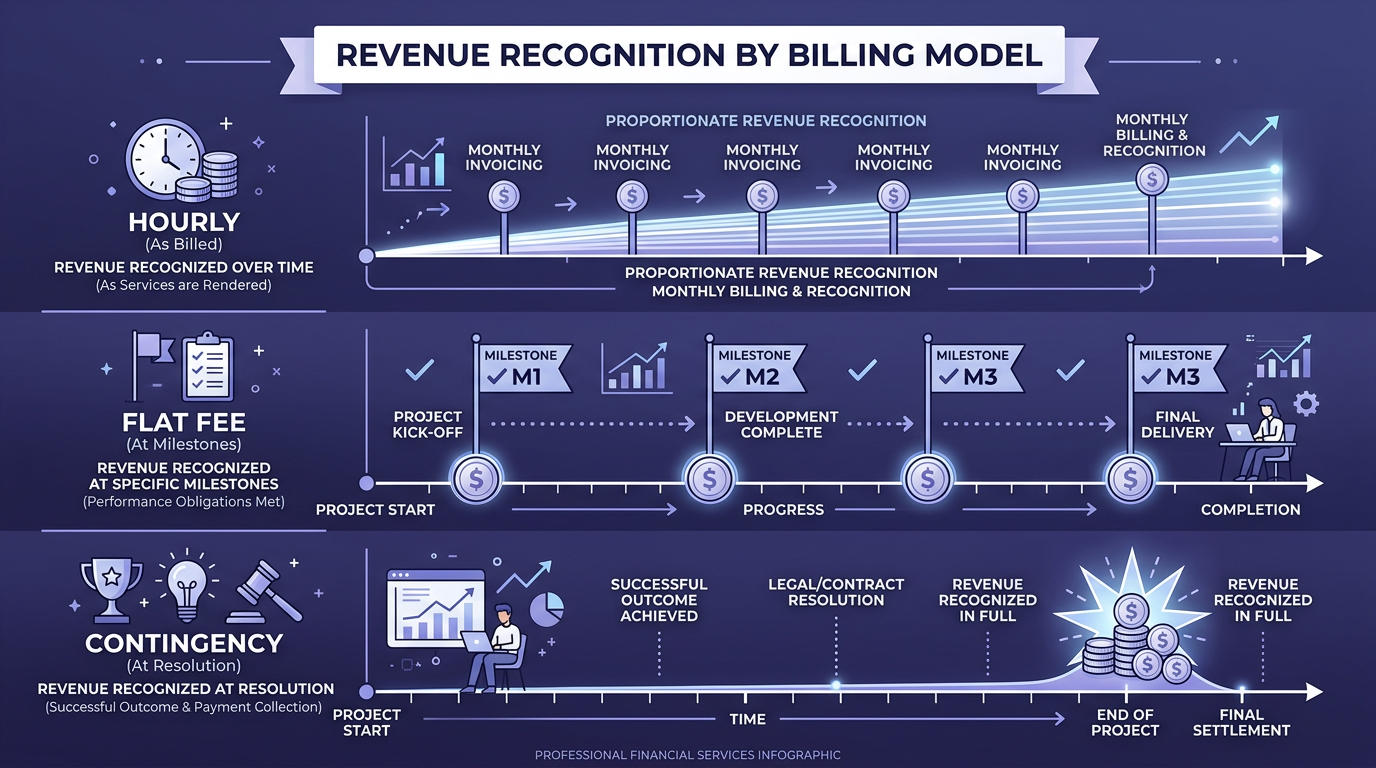

Attorneys log time against specific matters at predetermined rates. Revenue is recognized when invoiced (accrual basis) or collected (cash basis). Every hour logged but not yet billed creates a WIP asset on your balance sheet.

Accounting complexity: High. You’re tracking time entry, WIP aging, invoicing, collections, write-downs, and realization rates — all at the matter level.

The client pays a predetermined amount for a defined scope. A business formation costs $3,500 regardless of whether the attorney spends 6 or 16 hours. Revenue recognition depends on your engagement letter and state bar rules.

Accounting complexity: Moderate. No WIP tracking or realization rate calculations. But you need scope tracking to ensure profitability, and correct handling of fee deposits based on earned vs. unearned status.

The firm receives a percentage of the client’s recovery — typically 33% to 40%. Revenue is zero until the case resolves, often years after the engagement began. You still track attorney time for profitability analysis, but there’s no invoicing cycle.

Accounting complexity: Low for day-to-day, high for planning. Cash flow is inherently unpredictable, and case costs advanced on behalf of clients must be tracked as receivables or trust disbursements.

Many firms blend models — a family law matter might bill hourly for litigation but flat fee for document preparation. An IP firm might charge flat fees for trademark filings but hourly for opposition proceedings.

Accounting complexity: Highest. Every hybrid arrangement requires clear rules about which revenue line each fee component hits and which profitability metrics apply.

| Factor | Hourly (Matter-Based) | Flat Fee | Contingency | Hybrid |

|---|---|---|---|---|

| Revenue recognition | Upon invoicing or collection | Upon receipt or milestone completion | Upon case resolution | Split by component |

| WIP tracking required | Yes — critical | No | No | Partial (hourly portions only) |

| Realization rate applies | Yes | No (fixed price) | N/A | Hourly portions only |

| Trust account treatment | Unearned retainers held in IOLTA | Depends on state bar rules | Client cost advances in IOLTA | Varies by component |

| Cash flow predictability | Moderate (30-90 day collection cycle) | High (upfront or milestone) | Very low (months to years) | Moderate |

| Profitability measurement | Revenue per hour vs. cost per hour | Total fee vs. total cost | Recovery amount vs. case investment | Blended analysis required |

| QBO chart of accounts | Income by practice area + WIP asset | Income by service type | Contingency fee income + cost advances | Multiple income lines per engagement |

| Key risk | WIP aging and write-downs | Scope creep eroding margins | Case loss = zero revenue | Misclassification between fee types |

Important: The IRS treats law firm revenue recognition differently depending on whether your firm uses cash basis or accrual basis accounting. Under IRS Publication 538, firms with less than $30M in average annual gross receipts can generally use cash basis — but flat fee arrangements with milestone-based earning schedules may require accrual treatment for the deferred portions regardless of your overall method. Check with your CPA before switching billing models.

Each billing model follows different revenue recognition rules, and getting them wrong can trigger IRS scrutiny and state bar issues.

Under accrual basis, revenue is recognized when the invoice is generated — not when time is logged, and not when the client pays. A paralegal logging 8 hours on Monday creates WIP. When the invoice goes out on the 15th, WIP converts to accounts receivable and revenue is recognized. When the client pays on the 45th day, AR converts to cash.

Under cash basis, revenue isn’t recognized until the client’s check clears. WIP and AR are tracked operationally (in your practice management system) but don’t appear on your financial statements.

The critical distinction: time logged is never revenue. This is the single most common accounting error in hourly-billing firms. If your P&L shows revenue the moment attorneys enter time, your financial statements are overstated.

Flat fees introduce a question that hourly billing avoids entirely: when is the fee earned?

Three approaches, each with different accounting treatment:

Earned upon receipt — The engagement letter specifies the flat fee is nonrefundable and earned when paid. Revenue is recognized immediately. The fee goes directly to your operating account, never touching IOLTA. (Not permitted in all jurisdictions.)

Earned upon completion — The fee is earned when the defined scope of work is finished. Until then, the fee is an unearned liability on your balance sheet. If collected in advance, it sits in your IOLTA trust account until the work is done.

Earned at milestones — The fee is earned in stages tied to deliverables. A $6,000 estate plan might recognize $2,000 after the initial consultation and drafts, $2,000 after revisions and execution, and $2,000 after funding and final review.

Pro Tip: The ABA Model Rule 1.15 governs how client funds — including flat fee deposits — must be handled. But your state’s version may differ significantly. Illinois, for example, requires flat fees to be deposited into trust and withdrawn only as earned, unless the engagement letter explicitly states the fee is earned upon receipt and the client agrees in writing. Your bookkeeping system must match your state’s rule, not the ABA model.

Contingency cases produce zero recognized revenue until resolution. During the life of a case, track case costs advanced (filing fees, experts, depositions) as either client receivables or expenses depending on your engagement letter. Track attorney time for internal profitability analysis — a $300,000 settlement with a 33% fee earns $100,000, but if your attorneys invested 400 hours at $200/hour blended cost, the actual margin is 25%.

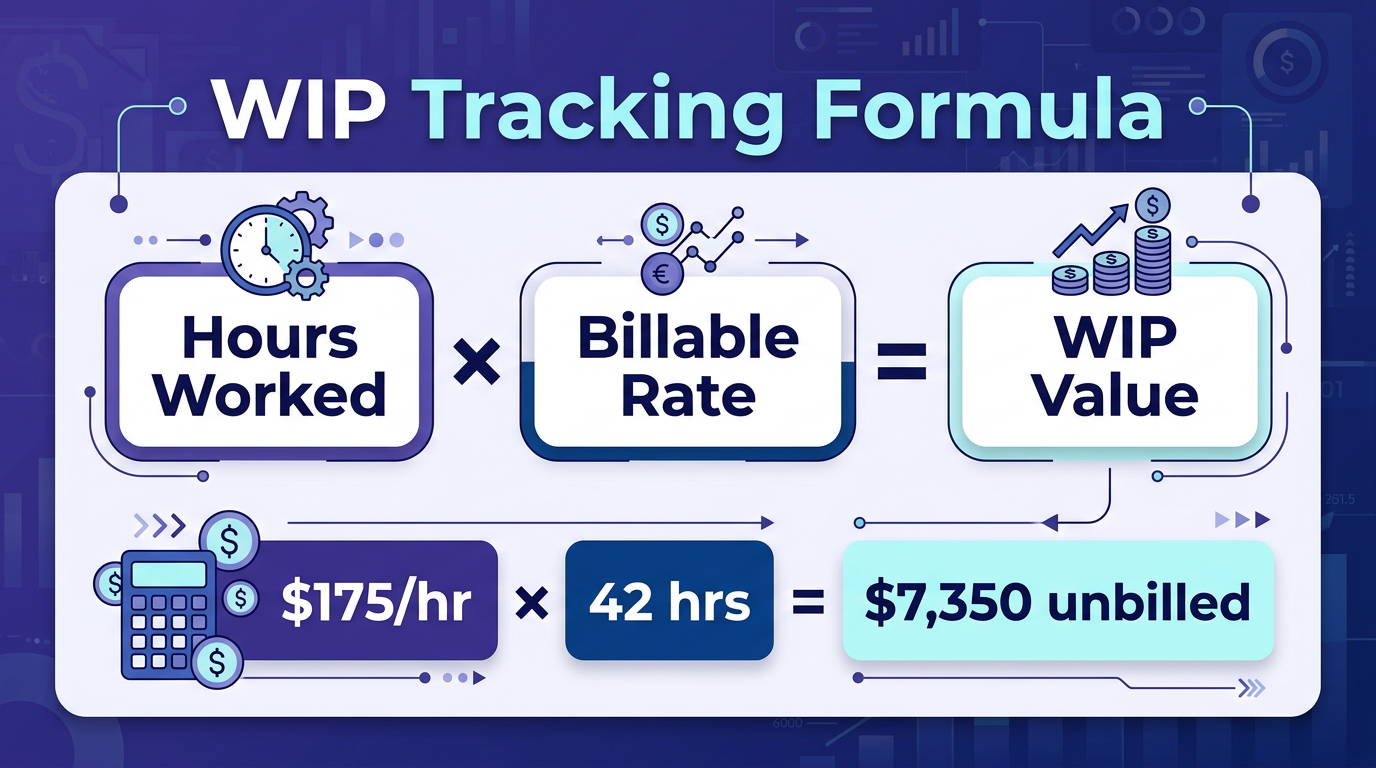

Work in progress represents completed work that hasn’t been invoiced — money you’ve earned in substance but haven’t captured in your billing system. Thomson Reuters benchmarks show that WIP older than 90 days has a collection probability below 60%. Over 180 days, it drops below 30%.

Hourly billing: WIP is tracked as a current asset on the balance sheet. Your practice management system (Clio, PracticePanther, Rocket Matter) generates the WIP report. Your bookkeeper reconciles the WIP balance in QBO against the practice management total monthly. Mismatches mean time isn’t flowing through — or write-downs aren’t being recorded.

Flat fee billing: No WIP exists. But track hours internally as “shadow WIP” for profitability analysis. If your flat fee formations average 14 hours at $3,500, your effective rate is $250/hour. If hours creep to 20, that drops to $175/hour.

Hybrid billing: Only hourly components generate WIP. Your chart of accounts and practice management system must cleanly separate hourly and flat fee revenue streams within the same matter.

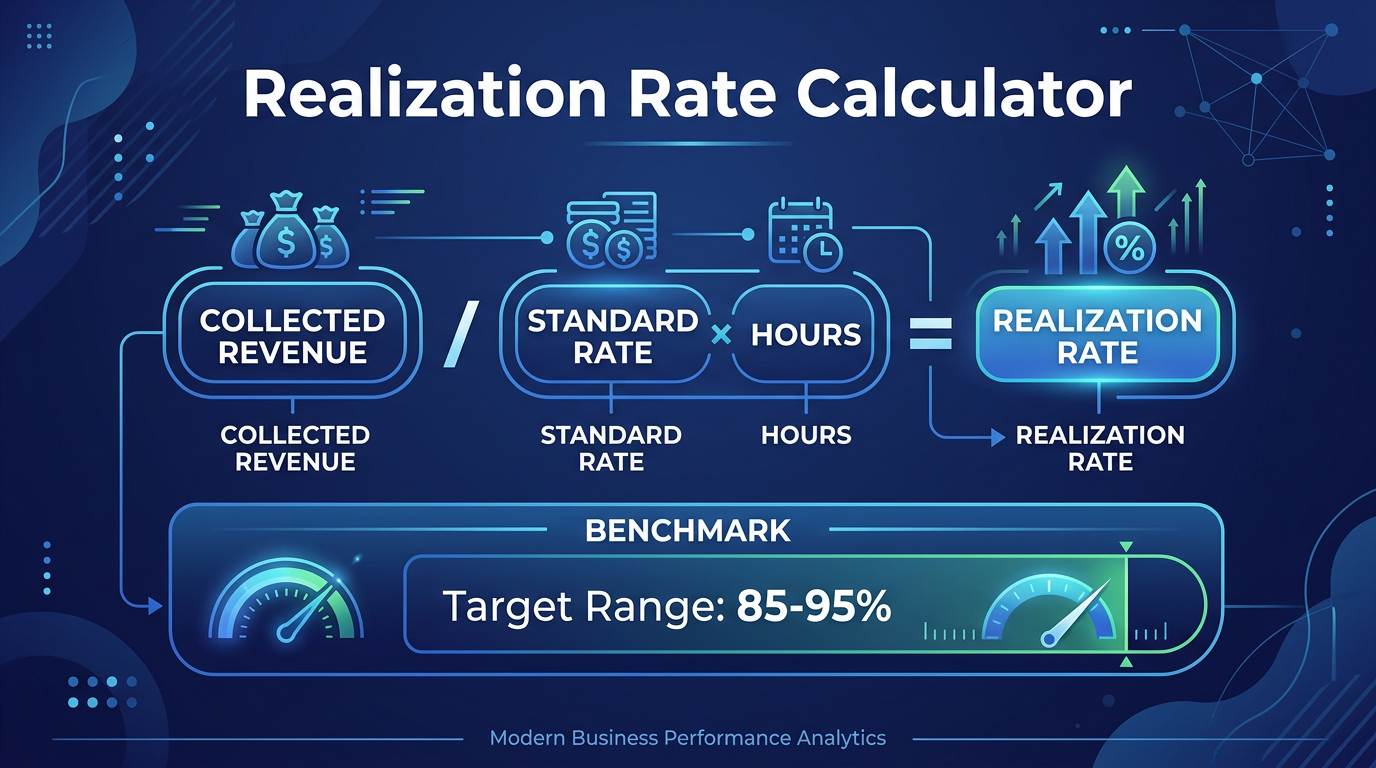

Realization rate measures what you collect versus what you could have collected at standard rates — the single most important profitability metric for hourly-billing firms.

Formula: Realization Rate = (Cash Collected) / (Standard Rate x Hours Worked) x 100

A firm with a $400/hour rate and 1,800 billable hours has a theoretical maximum of $720,000. If it collects $576,000 after write-downs and uncollectible invoices, the realization rate is 80%.

Hourly billing: Track realization at the attorney, practice area, and matter level. Clio’s Legal Trends Report places the median at 87% — the average firm loses 13 cents of every dollar.

Flat fee billing: Measure effective hourly rate instead — the flat fee divided by actual hours invested.

Contingency billing: Track return on case investment — the fee earned divided by total cost (attorney time plus case costs advanced).

In Clio, configure billing settings to capture standard value (hours x rate), invoiced value (after write-downs), and collected value (client payments) per matter. QBO won’t calculate realization rates natively — use Clio’s built-in reporting or build a monthly reconciliation spreadsheet. The integration between your practice management software and accounting system is where most firms leak data.

Key insight: Firms that track realization rates at the matter level consistently outperform firms that only track at the firm level. A firm-wide 85% realization rate might mask the fact that your corporate practice runs at 92% while your family law practice runs at 71%. Matter-level tracking reveals which clients, case types, and attorneys are dragging the number down — and gives you the data to reprice, restructure, or stop accepting that work.

Your QBO chart of accounts must reflect how your firm earns revenue. Hourly and flat fee firms need different account structures — and firms that do both must keep them separate.

Hourly billing requires the WIP asset (1300) and write-down contra account (4010). Flat fee replaces those with the unearned fee deposit liability (2200). If your firm runs both models, you need all accounts — and class tracking in QBO (Hourly vs. Flat Fee vs. Contingency) to enable accurate reporting by billing model.

Your billing model directly affects partner distribution calculations. Hourly firms tie compensation to origination and collection credits. Flat fee models simplify origination but make fair allocation harder across partners handling different matter types.

Track financial KPIs by partner separately for hourly and flat fee work. A partner generating $800,000 in flat fee revenue at 40% margin contributes more than one generating $1M hourly with a 15% realization gap and 25% WIP aging loss.

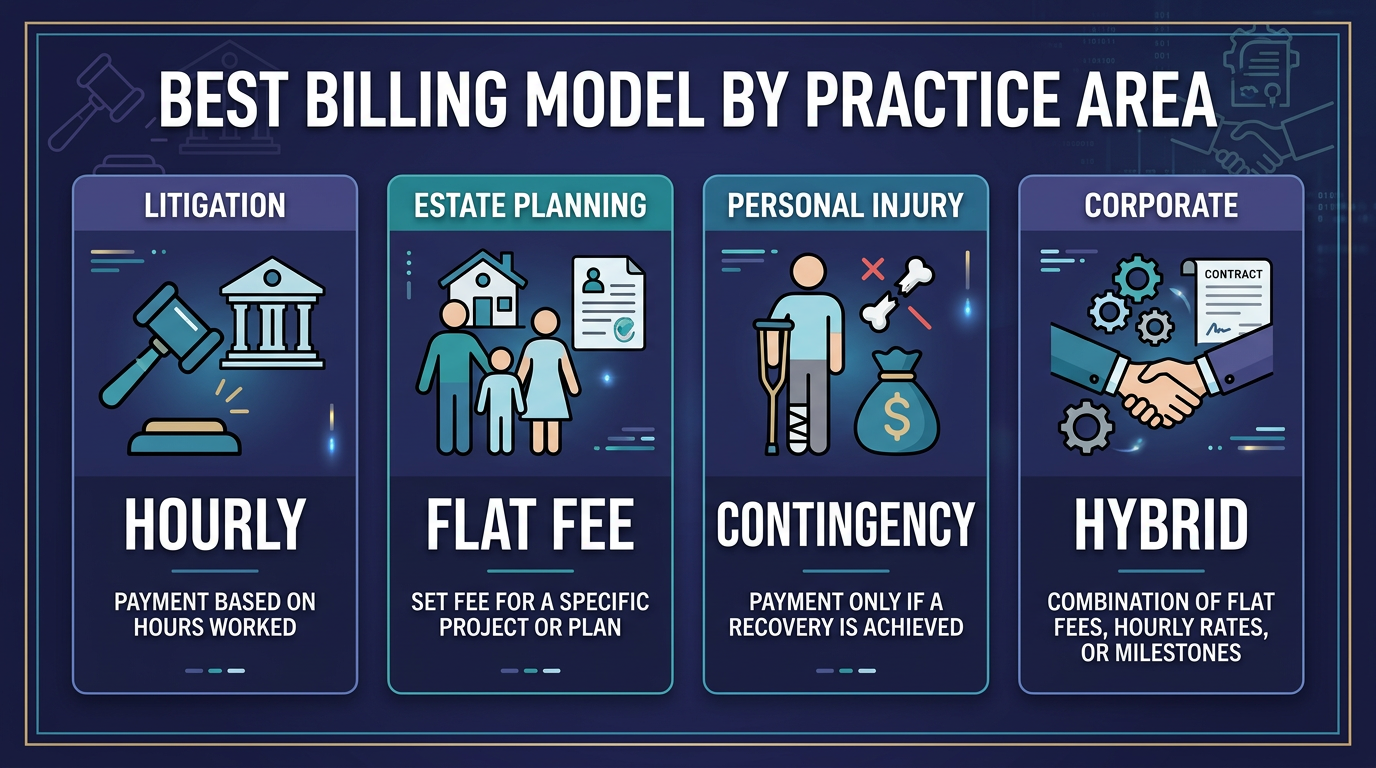

Not every practice area should use the same billing model. The accounting implications should factor into your decision alongside client preferences and competitive positioning.

Best fit for hourly billing: Complex litigation with unpredictable scope, regulatory and compliance advisory, and matters where the client’s decisions control the timeline.

Best fit for flat fee billing: Transactional work with predictable scope (formations, filings, closings), routine compliance filings, immigration petitions, trademark applications, and estate planning.

Best fit for contingency: Personal injury, medical malpractice, employment discrimination, and cases with high potential recovery relative to litigation cost.

Best fit for hybrid: Family law (flat fee for uncontested, hourly for contested), IP portfolios (flat fee filings, hourly opposition), and corporate clients with both transactional and advisory needs.

The accounting principle: match your billing model to the predictability of the work, and match your accounting setup to the billing model. For a complete breakdown of every financial metric across billing models, see our law firm bookkeeping guide.

Related Reading:

Ready to get your law firm’s books aligned with your billing model? Whether you’re running hourly, flat fee, or a hybrid across practice areas, Steph’s Books specializes in law firm accounting that matches how your firm actually operates. Schedule a free consultation →

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.