DIY bookkeeping works at $200K in revenue. You’re doing the data entry, the reconciliation, maybe running payroll yourself. It takes a few hours a month. No big deal.

Then your firm crosses $1M. And that “free” bookkeeping becomes the most expensive thing you do. Not because of the software cost — because of what it costs you in lost billable hours, stale decisions, and preventable mistakes. If you’re evaluating whether it’s time to make a change, our complete guide to outsourced bookkeeping walks through the full picture: pricing, process, and ROI.

Here are seven signs that your firm has outgrown DIY bookkeeping — and what to do about it.

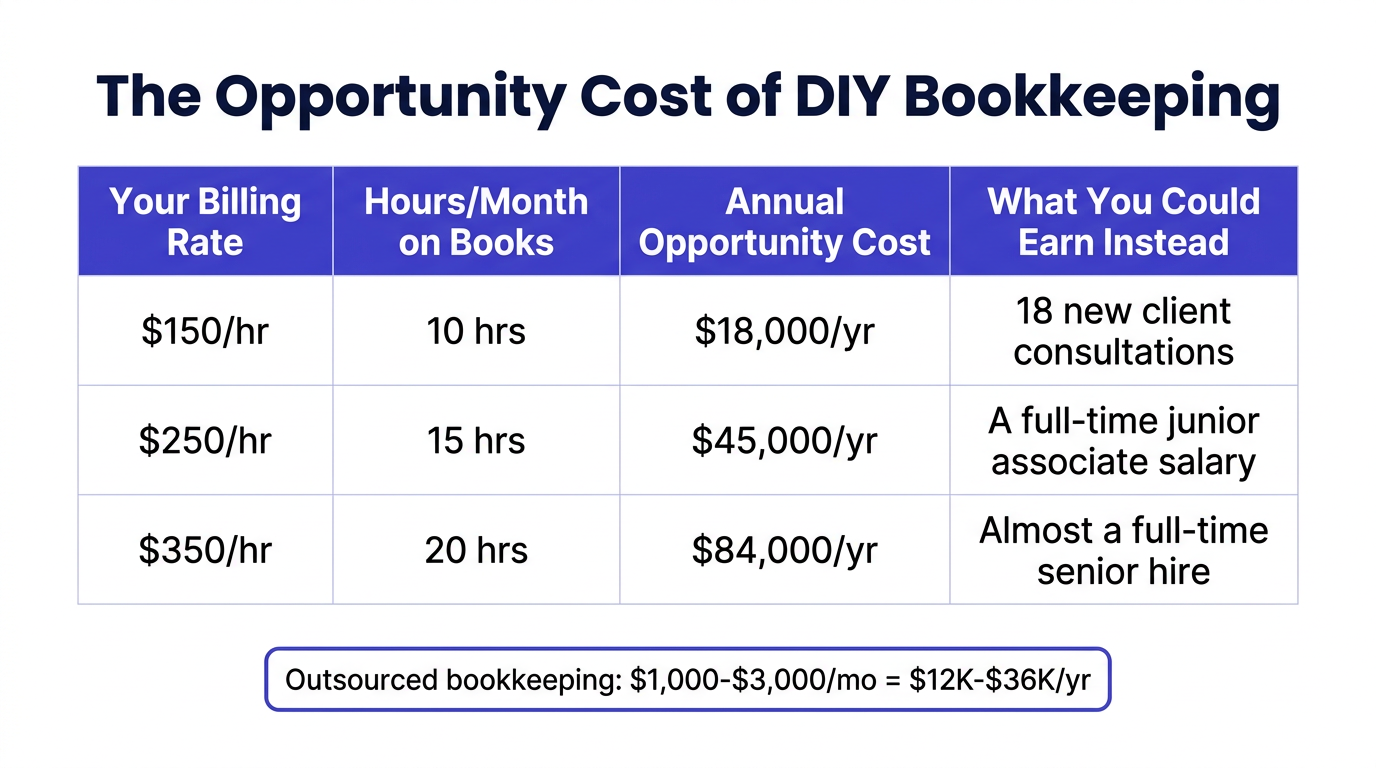

This is the most common sign, and the easiest to quantify. If you or your office manager spends 10 or more hours each month on transaction categorization, bank reconciliation, invoice entry, and payroll reconciliation, you’re bleeding billable capacity.

Here’s the math most firm owners never run:

| Your Billing Rate | Hours/Month on Books | Annual Opportunity Cost |

|---|---|---|

| $150/hr | 10 hours | $18,000/year |

| $250/hr | 15 hours | $45,000/year |

| $350/hr | 20 hours | $84,000/year |

Meanwhile, outsourced bookkeeping for a $1M–$3M firm runs $1,000–$2,500 per month — a fraction of the opportunity cost. According to the Bureau of Labor Statistics, the median bookkeeper salary is approximately $47,440 per year before benefits, PTO, and employer taxes push the real cost well past $60,000.

Pro Tip: Track your actual bookkeeping hours for one month. Include the 20 minutes categorizing transactions on your phone, the Saturday morning fixing a reconciliation error, and the hour prepping reports for your CPA. The real number is always higher than people estimate.

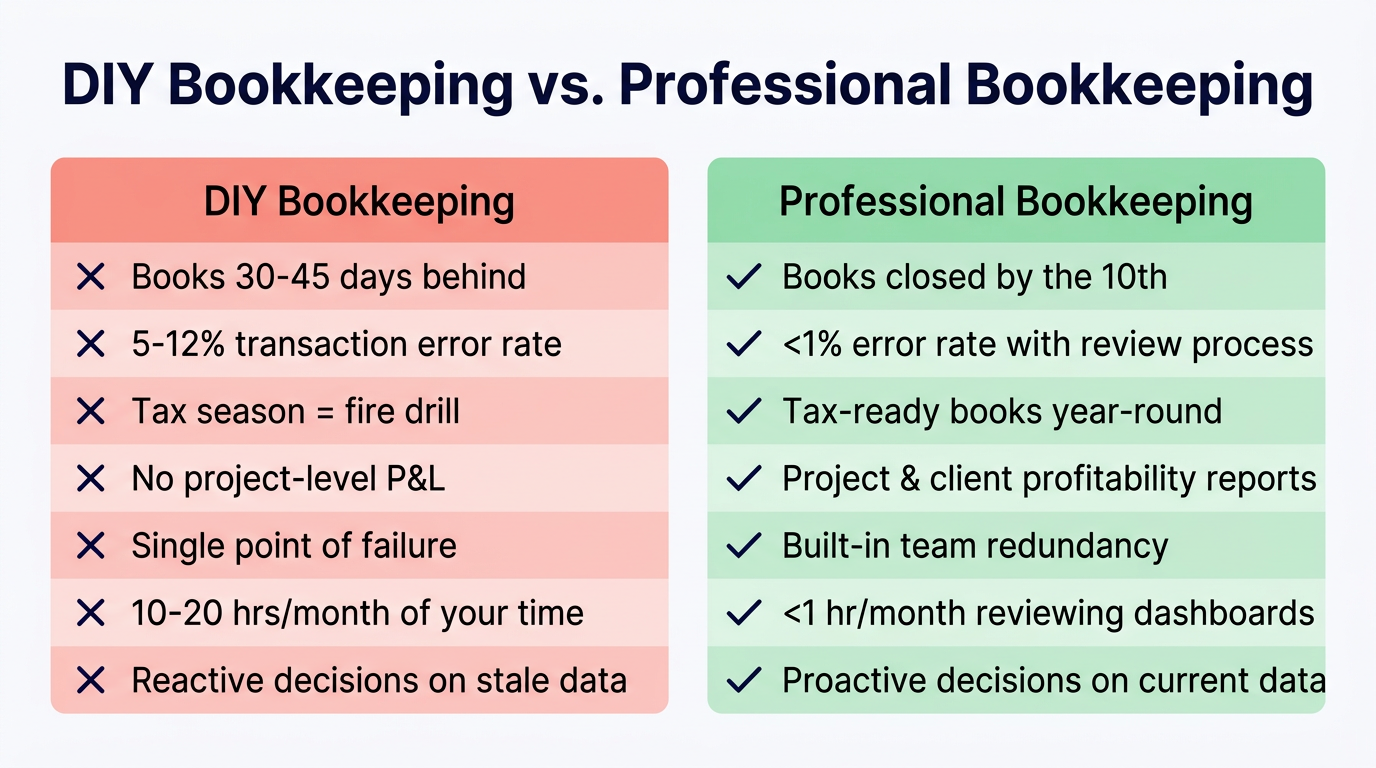

If your most recent financial statements are from two months ago, you’re making decisions on stale data. And in a professional services firm where labor is 55–75% of expenses, stale data leads to costly mistakes.

Consider what happens when your books are 30–45 days behind:

A professional bookkeeping team with defined SLAs closes your books by the 10th–15th of the following month. That’s the difference between leading with data and chasing it.

If your CPA dreads working with your firm, that’s a sign. If you’ve filed extensions in two of the last three years, that’s a bigger sign. And if you’ve ever paid for a tax amendment because your books had material errors, you already know the problem.

Here’s what the annual fire drill actually costs:

| Tax Season Problem | Direct Cost | Hidden Cost |

|---|---|---|

| Filing an extension | $0 (IRS fee) | 6 months of uncertainty about tax liability |

| CPA catch-up and cleanup | $2,000–$5,000 | Higher CPA fees going forward (risk premium) |

| Amended return | $1,500–$4,000 | Potential audit trigger |

| Misclassified 1099 contractors | $5,000–$25,000+ in penalties | IRS scrutiny for 3+ years |

Professional bookkeeping means your books are tax-ready year-round — not just “close enough” in April. Your CPA gets clean, reconciled financials on schedule, with proper classifications and documentation already in place.

Ask yourself: can you tell, right now, whether the Henderson account is making or losing money?

Not revenue — profitability. After fully loaded labor costs, after overhead allocation, after scope creep hours that nobody billed for.

Most DIY bookkeeping setups dump everything into broad revenue and expense categories. There’s no class tracking, no project tagging, no WIP (work-in-progress) reconciliation. The result: you’re flying blind on which clients and projects actually contribute to your bottom line.

This matters because professional services firms routinely discover that 20–30% of their clients are unprofitable when they finally get project-level visibility. That’s not a rounding error — it’s a strategic problem that only surfaces with the right financial infrastructure.

The real cost: Without project-level P&L, every fixed-fee proposal is a guess. You’re pricing based on gut feeling instead of data. Firms that implement project profitability tracking typically find 8–12% in revenue leakage from unbilled time and underpriced engagements.

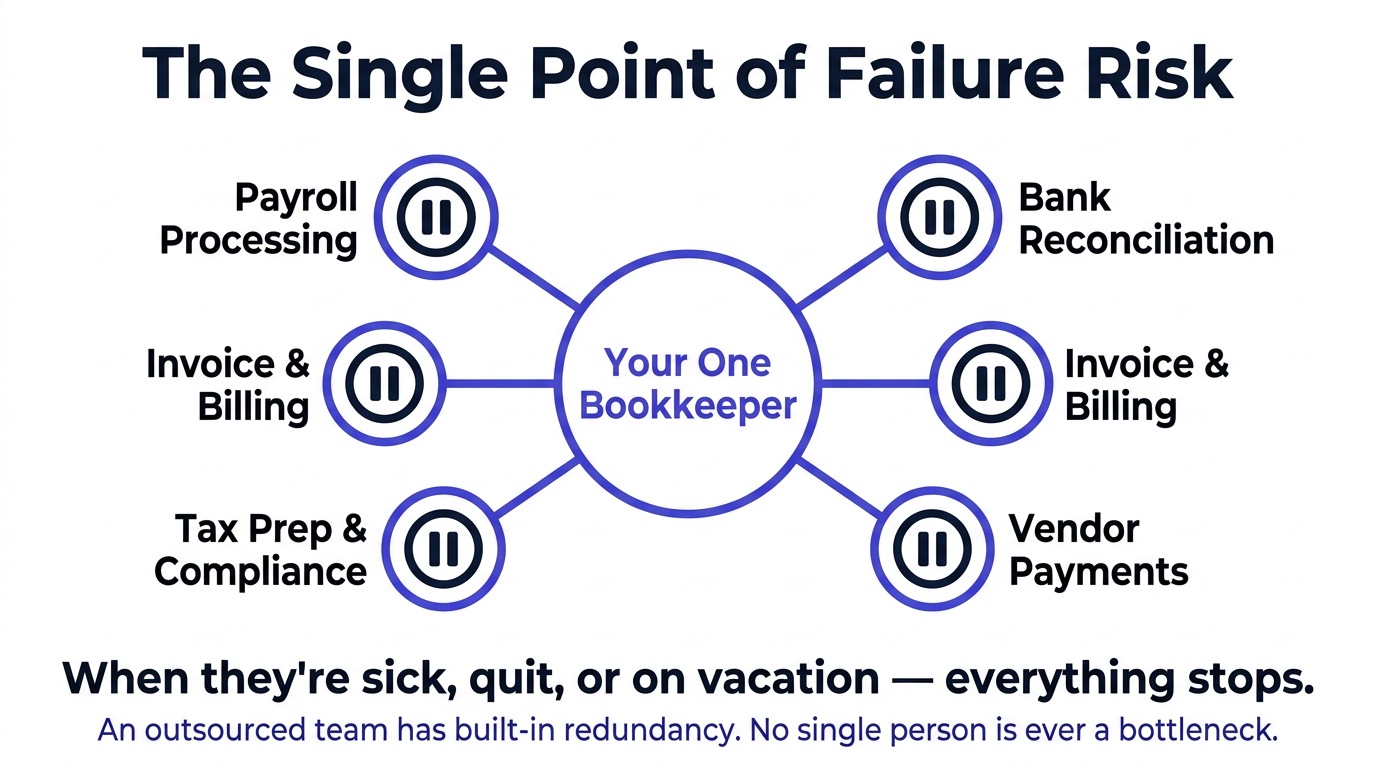

If one person handles all of your financial operations — whether that’s you, an office manager, or a part-time bookkeeper — you have a single point of failure. When that person takes vacation, gets sick, or quits, everything stops:

And it’s not just the immediate disruption. When that person leaves — and the average bookkeeper tenure is just 2.3 years — you lose institutional knowledge. Where do the receipts go? How do you categorize that recurring charge from the software vendor? What’s the process for the quarterly payroll filing? It all walks out the door.

An outsourced bookkeeping team has built-in redundancy. Your account is managed by a team, not a single person. If one team member is unavailable, another picks up seamlessly because the processes are documented and the systems are standardized.

There’s a meaningful difference between “bookkeeping” and “financial infrastructure.” At $200K–$500K in revenue, you need bookkeeping: someone to categorize transactions and reconcile the bank account. At $1M+, you need systems.

Financial infrastructure for a growing professional services firm includes:

You can’t build this infrastructure while also being the person who categorizes transactions. The operational work crowds out the strategic work every time. Read our guide on the five bookkeeping mistakes that cost professional services firms thousands for more on the structural gaps that emerge at this stage.

Sometimes the clearest sign is the one you’ve already experienced. If any of these sound familiar, you’ve outgrown DIY bookkeeping:

Each of these mistakes has a direct cost (penalties, overpayments, lost revenue) and an indirect cost (the time you spent fixing it, the stress, the lost confidence in your numbers). Professional bookkeeping doesn’t eliminate human error entirely — but it introduces review processes, segregation of duties, and systematic checks that catch mistakes before they become expensive.

Reality check: If you’ve experienced two or more of the items on this list in the past 12 months, DIY bookkeeping isn’t just inconvenient — it’s actively costing your firm money. The question isn’t whether you can afford to outsource. It’s whether you can afford not to.

The transition from DIY to professional bookkeeping follows a predictable pattern. If your books are behind, the first step is a catch-up engagement that brings everything current — typically within 2–4 weeks depending on how far behind you are.

After that, here’s what the first 90 days look like:

By month three, most firm owners go from spending 10–20 hours per month on bookkeeping to less than one hour reviewing dashboards and reports. That’s not a marginal improvement — it’s a structural change in how you operate.

If you recognized your firm in three or more of these signs, it’s time to stop treating bookkeeping as a DIY project and start treating it as the financial infrastructure your firm needs to grow.

Request a free bookkeeping diagnostic — we’ll review your current setup, calculate your real cost of DIY bookkeeping, and show you exactly what professional bookkeeping services look like for your firm. No pitch deck, no pressure — just an honest assessment.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.