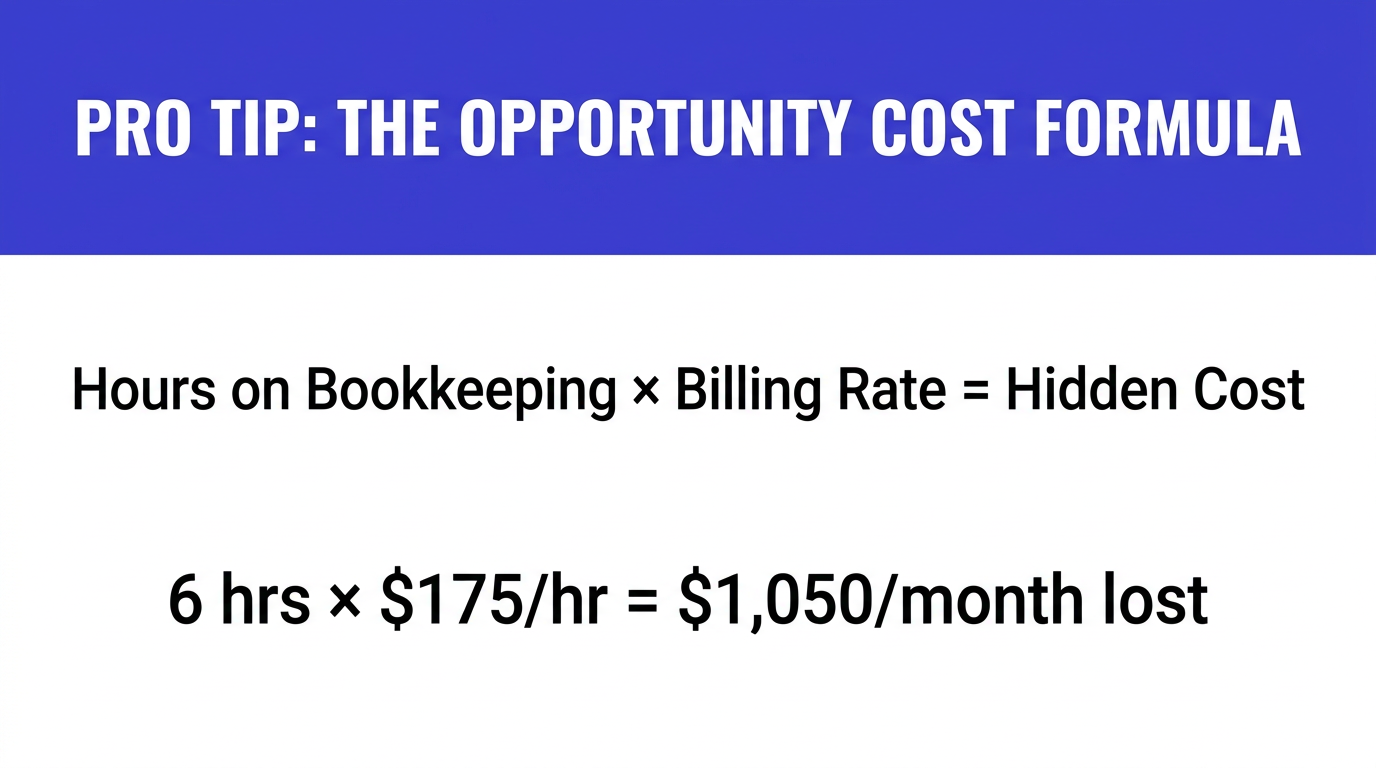

Your firm bills $175/hour. Your managing partner spent six hours last month reconciling QuickBooks because your office manager was on PTO. That’s $1,050 in lost billable time — on a task that an outsourced bookkeeping team handles for $500/month.

That math is why professional services firms between $1M and $10M in revenue are outsourcing their bookkeeping at record rates. Not because they can’t afford an in-house hire — but because the opportunity cost of financial admin is destroying their margins.

This guide breaks down everything you need to know about outsourced bookkeeping for professional services firms: what it actually costs, what’s included, how the transition works, and how to evaluate whether it’s the right move for your firm.

Outsourced bookkeeping means hiring an external team — not an employee — to handle your day-to-day financial record-keeping. For professional services firms, that typically includes:

What it is not: tax filing, strategic financial advisory, or fractional CFO work. Those are separate services. An outsourced bookkeeper is the engine room — they keep the data clean so your CPA and advisors can do their job with accurate numbers.

Key distinction: If you’re comparing outsourced bookkeeping to a virtual CFO, you’re looking at different services. A bookkeeper handles data entry and reconciliation. A CFO interprets the data and makes strategic recommendations. Most firms need both, but the bookkeeper comes first. See our breakdown of in-house vs. outsourced bookkeeping for the full comparison.

Generic bookkeeping — the kind designed for retail shops and restaurants — doesn’t work for professional services. Your firm has specific financial dynamics that require specialized handling:

You don’t sell widgets. You sell time, and time gets complicated. Between retainers, fixed-fee engagements, hourly billing, and progress invoicing, your revenue recognition needs to track:

A bookkeeping partner who understands professional services knows how to set up your chart of accounts to separate these categories. A generalist bookkeeper dumps everything into “Revenue” and calls it a day.

In a law firm, architecture practice, or consulting firm, 55-75% of your expenses are people costs. Your bookkeeping needs to track:

If your books don’t separate labor burden from base salary, you’re underpricing every fixed-fee project by 25-40%. That’s not a bookkeeping problem — it’s a pricing problem caused by bad bookkeeping.

Law firms have IOLTA requirements. Property management companies have security deposit escrow rules. Healthcare practices have insurance payment reconciliation. Each industry within professional services has compliance requirements that a generic bookkeeper will miss.

Pricing varies by firm size, transaction volume, and complexity. Here’s the realistic range for professional services firms:

| Firm Revenue | Monthly Transactions | Outsourced Cost/Month | In-House Equivalent |

|---|---|---|---|

| $500K – $1M | 100-200 | $500 – $1,000 | $3,500 – $4,500 |

| $1M – $3M | 200-500 | $1,000 – $2,500 | $4,500 – $6,000 |

| $3M – $5M | 500-1,000 | $2,000 – $4,000 | $5,500 – $7,500 |

| $5M – $10M | 1,000+ | $3,500 – $6,000 | $7,000 – $9,500 |

The “In-House Equivalent” column includes salary, benefits (add 30-40% to base), software licenses, training, management overhead, and backup coverage.

For a detailed breakdown by business size and service tier, see our complete outsourced bookkeeping cost analysis.

Pro Tip: When comparing costs, don’t forget the hidden expenses of in-house: turnover (average bookkeeper tenure is 2.3 years), training new hires, PTO coverage gaps, and the 2-4 week disruption when someone quits mid-month-end-close.

Cost savings are the obvious benefit. The real ROI comes from three less obvious places:

Every hour your managing partner or office manager spends on bookkeeping tasks is an hour not spent on client work. At a $175-$300/hour billing rate, even 5 hours/month of recovered time generates $10,500-$18,000/year in additional capacity.

Most firms running their own books get financials 30-45 days after month-end. An outsourced team with defined SLAs delivers closed books by the 10th-15th of the following month. That 20-30 day improvement means you’re making decisions on data from this quarter, not last quarter.

DIY bookkeeping error rates run 5-12% on transaction categorization. For a firm processing $200K/month in transactions, that’s $10,000-$24,000/month in potentially miscategorized expenses. Those errors compound into:

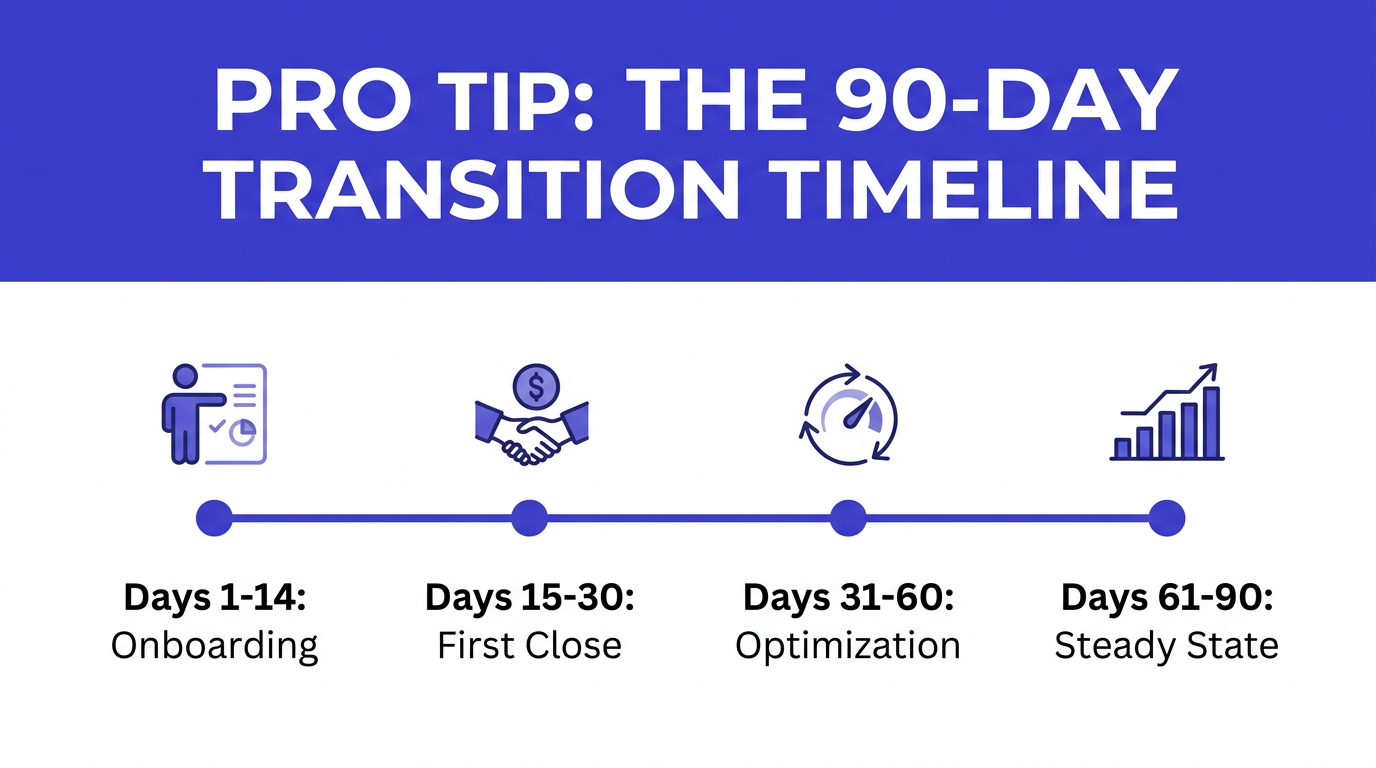

The transition to outsourced bookkeeping follows a predictable timeline:

Reality check: Month one will feel slower than doing it yourself. That’s normal. You’re investing upfront time to build a system that runs without you. By month three, you should be spending less than 1 hour/month reviewing financials instead of 10-15 hours doing them.

A firm that specializes in professional services will understand your chart of accounts needs, your practice management software integrations, and your compliance requirements out of the box. Generalist providers will learn on your dime.

Ask this question: “How many law firms / consulting firms / PM companies do you currently serve?” If the answer is zero, keep looking.

Your bookkeeping partner needs to work with your existing tools:

See our QuickBooks Online setup guide for how this should look.

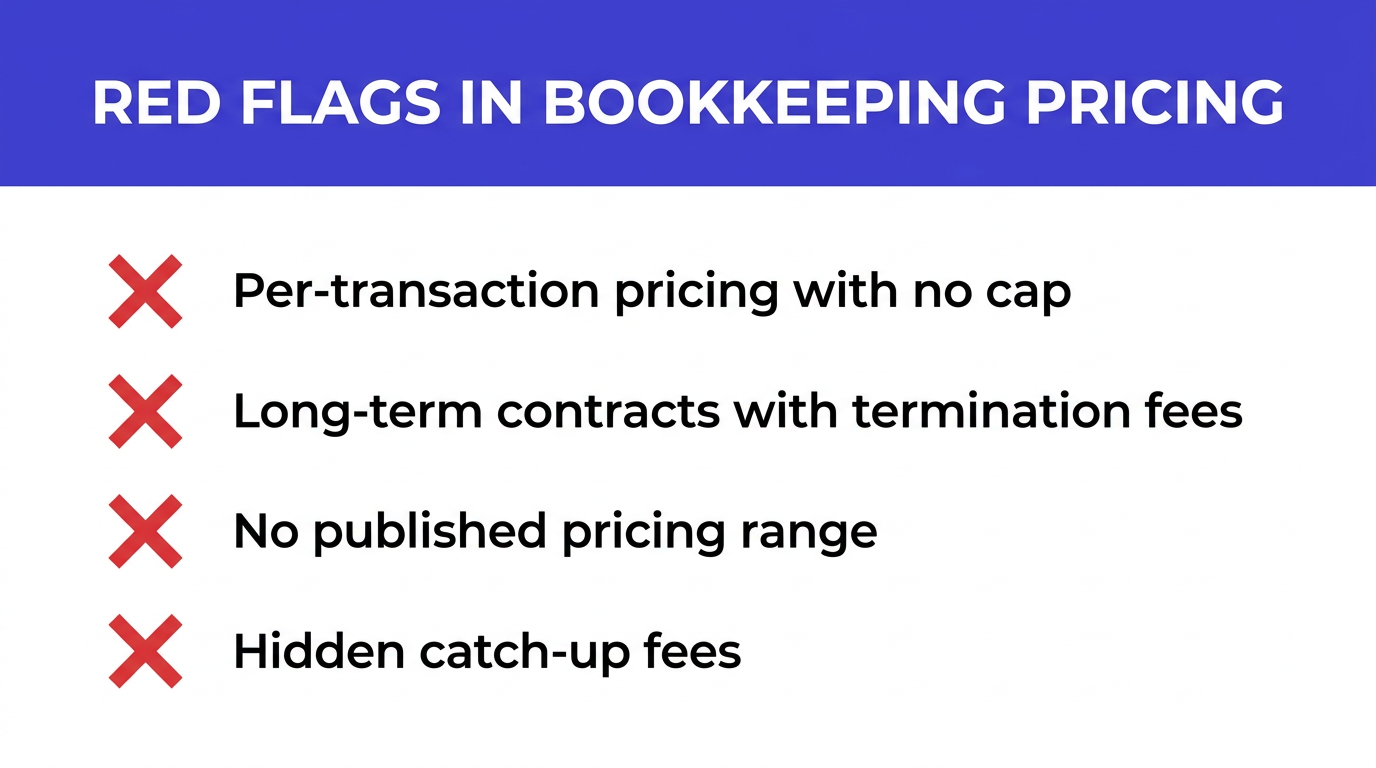

Define expectations upfront:

Green flags:

For our approach to transparent pricing, visit our pricing page.

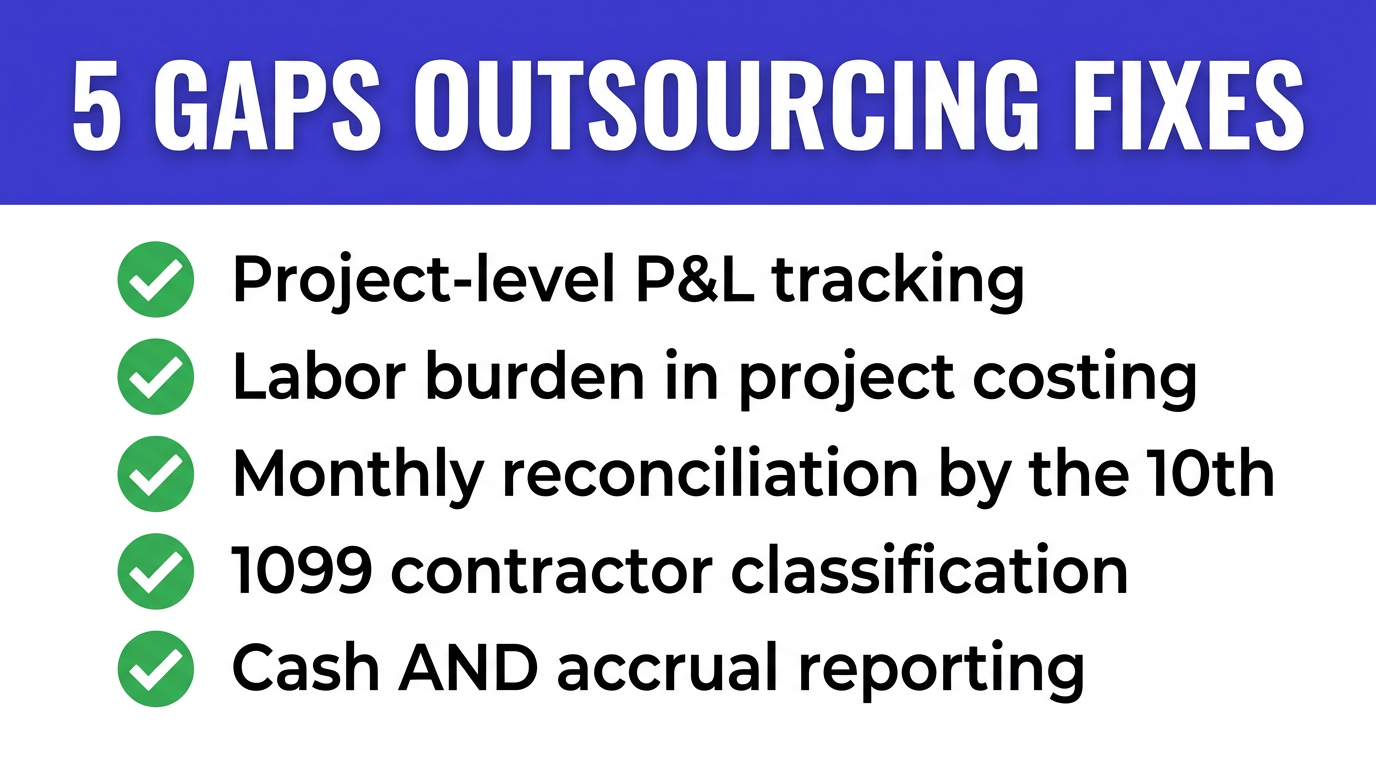

Professional services firms at the $1M-$10M level share common bookkeeping problems. Outsourcing addresses all five:

For a deep dive into each of these, read our analysis of the 5 bookkeeping mistakes costing professional services firms thousands.

The decision to outsource bookkeeping isn’t about whether you can do it yourself — it’s about whether you should. If your firm’s competitive advantage comes from billable expertise, every hour spent on financial admin is an hour stolen from growth.

Request a free bookkeeping diagnostic — we’ll review your current setup, identify the gaps, and show you exactly what outsourced bookkeeping looks like for your firm.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.