Every plumbing company between $1M and $10M uses subcontractors. Gas line specialists, drain camera operators, trenching crews, backflow testers — these are skilled trades people you bring in for specific jobs, pay by the project, and never put on payroll. Managing 1099 for subcontractors plumbing companies rely on is straightforward in theory: collect a W-9, track payments, file a 1099-NEC at year end. In practice, most plumbing contractors we work with have at least two or three subs with missing paperwork, inconsistent payment records, or categorization errors that create real compliance exposure.

For the full picture, see our complete guide to plumbing bookkeeping. This post focuses specifically on the subcontractor management workflow — from onboarding documentation through year-end filing — and the penalties you face when it falls apart.

The decision to subcontract versus hire is not just operational. It has direct financial and legal consequences that affect your tax liability, insurance costs, and audit risk.

Financial case for subcontracting: You avoid payroll taxes (7.65% FICA match), workers’ compensation premiums (8-15% of payroll for plumbing classifications), unemployment insurance, benefits, and the administrative overhead of managing another W-2 employee. On a $60,000/year worker, the fully loaded cost difference between W-2 and 1099 is typically $12,000 to $22,000 per year.

Financial case for hiring: Employees show up when scheduled, follow your processes, and build institutional knowledge. Subcontractors cost more per hour, set their own schedules, and serve other clients. If you need someone 40 hours a week, 50 weeks a year, the premium you pay for a sub’s flexibility rarely pencils out.

Common plumbing subcontractor roles:

Important: The IRS does not care what you call someone. If a worker functions as an employee — using your tools, following your schedule, working exclusively for you — classifying them as a 1099 subcontractor creates misclassification liability regardless of what your contract says.

The single most important compliance step happens before you write the first check. Require a completed W-9 from every subcontractor before the first payment. Not after. Not at year end when you’re scrambling. Before.

1. Request the W-9 at engagement. When you agree to use a sub on a job, send the W-9 request as part of your subcontractor agreement package. Make it a gating requirement — no W-9, no purchase order, no payment.

2. Verify the TIN. The IRS TIN Matching program lets you verify that the name and TIN on a W-9 actually match IRS records. A mismatched TIN triggers a B-Notice from the IRS and can result in backup withholding at 24%.

3. Store W-9s securely. These forms contain Social Security numbers or EINs. Store them in an encrypted digital folder — not in an unlocked filing cabinet and not in a shared Google Drive with no access controls. Retention requirement: four years after the tax year the form covers.

4. Re-collect W-9s when information changes. If a sub incorporates, changes their business name, or gets a new EIN, you need an updated W-9 before the next payment.

Accurate 1099 reporting starts with how you set up vendors and categorize payments in QuickBooks Online. Get this right and year-end filing is a 20-minute export. Get it wrong and you’re pulling bank statements in January trying to reconstruct a year’s worth of sub payments.

1. Create each sub as a vendor. Go to Expenses > Vendors > New Vendor. Enter the legal name exactly as it appears on the W-9 — not nicknames, not DBA names unless the W-9 specifies.

2. Enable 1099 tracking. On the vendor record, check “Track payments for 1099.” This is the critical step most plumbing contractors miss. Without this flag enabled, the vendor’s payments won’t appear in your 1099 report, and you’ll have to go back and manually tally every payment from the year.

3. Enter the TIN. Input the EIN or SSN from the W-9 into the Tax ID field on the vendor record. QBO uses this to populate the 1099-NEC forms.

4. Categorize payments correctly. Map sub payments to a dedicated COGS account — typically 5070 Subcontractor Costs — not to a generic “Contract Labor” or “Outside Services” expense account. This keeps your job costing clean and your bookkeeping audit-ready.

5. Use the 1099 report to verify. Run Reports > 1099 Transaction Detail quarterly — not just at year end. Catch missing vendors and miscategorized payments while you can still fix them.

Every nonemployee you paid $600 or more during the calendar year gets a 1099-NEC. This applies to individuals, partnerships, and LLCs taxed as sole proprietors or partnerships. It does not apply to payments made to corporations (S-corps and C-corps) — which is why the W-9 matters, because it tells you the entity type.

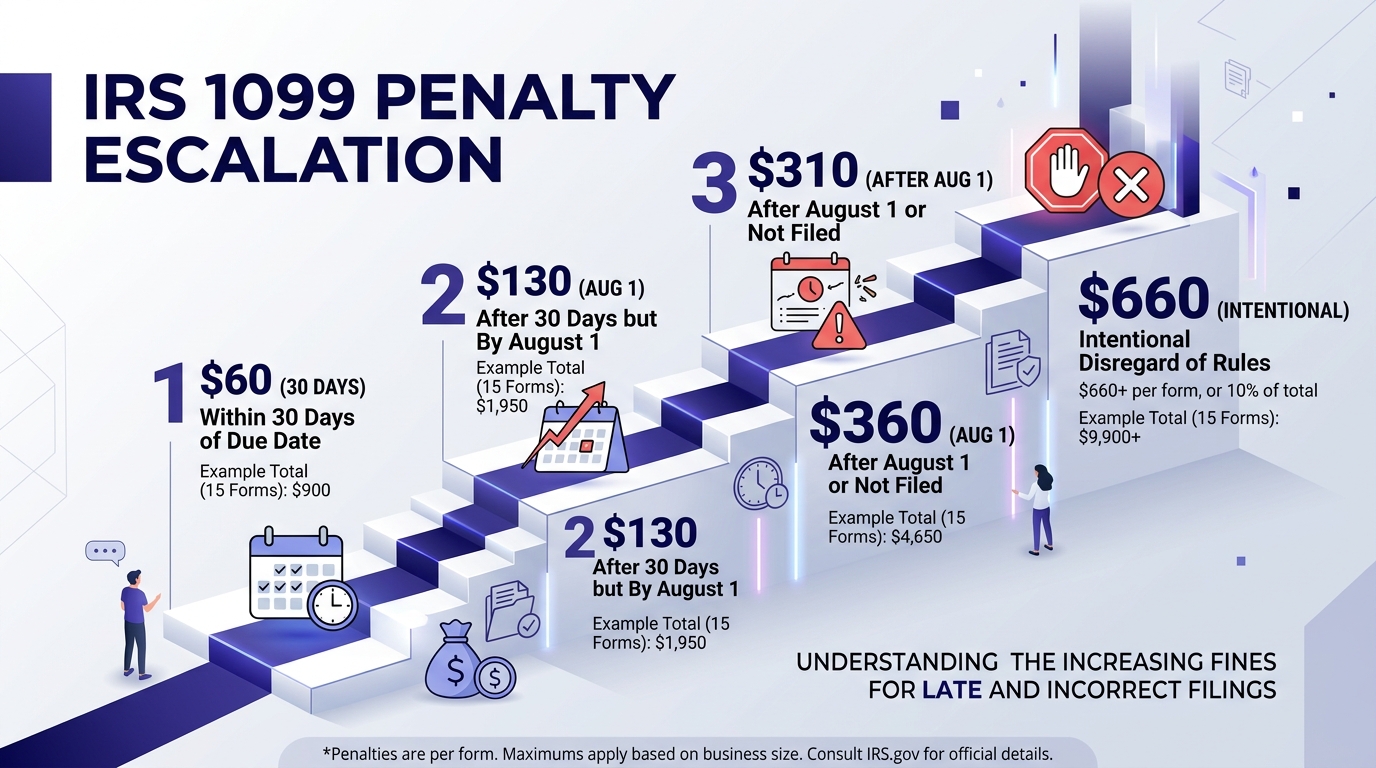

Miss the deadline and penalties escalate based on how late you file:

| Filing Status | Penalty Per Form | Example: 15 Subs |

|---|---|---|

| Filed within 30 days of deadline | $60 | $900 |

| Filed by August 1 | $130 | $1,950 |

| Filed after August 1 or not at all | $310 | $4,650 |

| Intentional disregard | $660 | $9,900 |

These penalties apply per form. A plumbing company with 15 subs that misses the January 31 deadline and doesn’t file until September is looking at $4,650 in penalties — for paperwork, not fraud.

Real scenario: One of the plumbing contractors we onboarded had 15 active subcontractors. Three were missing W-9s entirely. Without the W-9, you can’t file the 1099 on time — which means at minimum, $60 per form for late filing within 30 days, or $310 each if you don’t track them down until after August 1. Those three missing W-9s represented $930 in potential penalties just for late filing — before any TIN mismatch or backup withholding issues entered the picture.

Worker misclassification — treating an employee as a 1099 subcontractor — is one of the highest-risk compliance issues in the trades. Plumbing companies are particularly vulnerable because the line between “sub” and “employee” is blurry in field operations.

The IRS uses a 20-factor test grouped into three categories — behavioral control, financial control, and relationship type. The simplified version:

Behavioral control: Do you tell the worker when to show up, how to do the work, and what tools to use? If yes, they’re likely an employee. A true sub sets their own schedule, uses their own equipment, and controls their own methods.

Financial control: Does the worker have a significant investment in their own tools and equipment? Do they serve multiple clients? Can they profit or lose money on a job? Subs carry their own insurance, own their own equipment, and market their services to other plumbing companies.

Relationship type: Is the work ongoing and integral to your business, or project-based and specialized? A plumber who works exclusively for you, 40 hours a week, on your truck, with your tools is an employee — regardless of what your contract says.

If the IRS or state determines you misclassified employees as independent contractors, the financial exposure is significant:

Pro Tip: If you’re unsure whether a worker is a sub or an employee, file IRS Form SS-8 and let the IRS make the determination. It takes 6-12 months, but it gives you a definitive answer and demonstrates good faith if you’re ever audited.

The IRS requires you to keep employment tax records for four years after the due date of the return or the date the tax was paid — whichever is later. For 1099 purposes, this means:

Store everything digitally with dated backups. If you’re using QuickBooks Online, your transaction data is retained automatically — but the W-9s and subcontractor agreements need a separate, organized storage system.

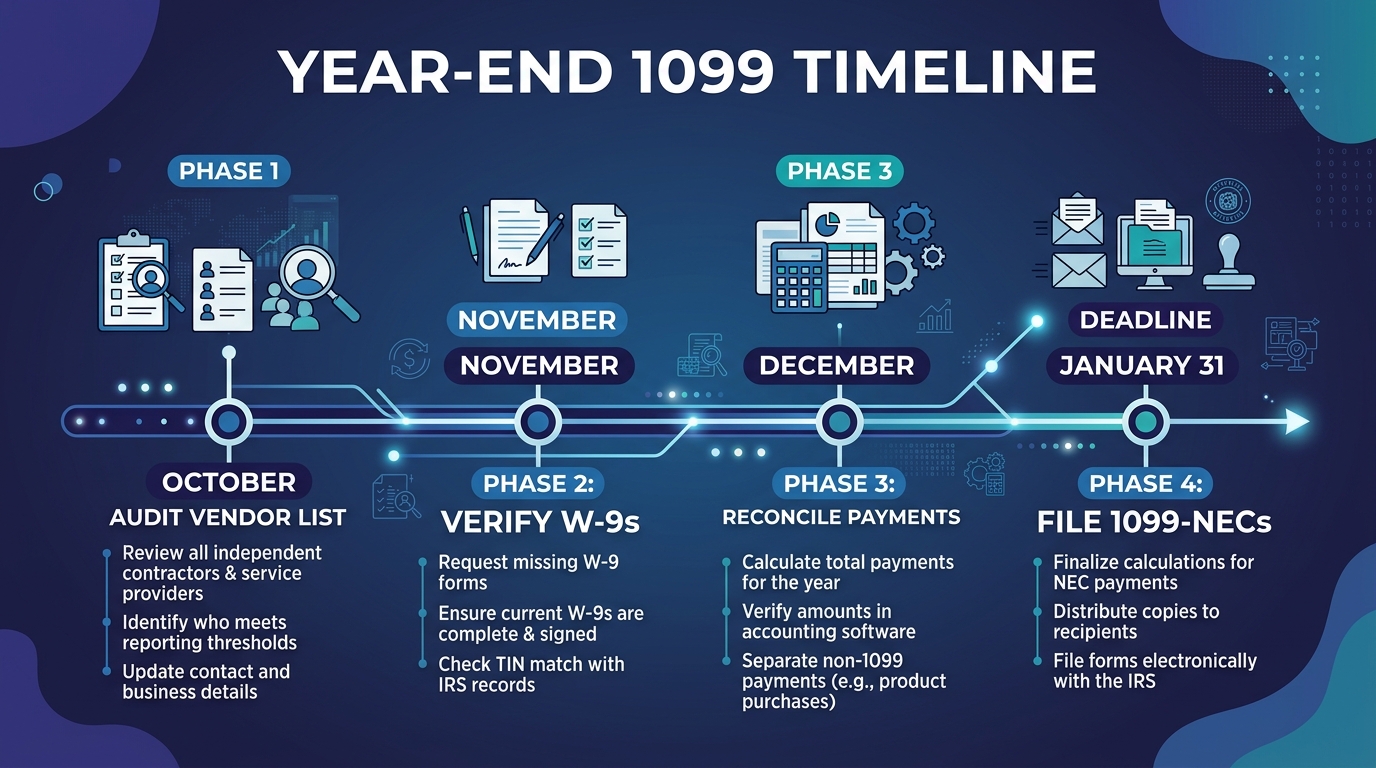

Don’t wait until January to start your 1099 prep. The plumbing contractors who file cleanly every year follow a timeline that starts in October.

Stop chasing W-9s in January. Steph’s Books handles 1099 subcontractor tracking, W-9 management, and year-end filing for plumbing contractors — so you never miss a deadline or face an avoidable penalty. Get an instant quote or schedule a free consultation to lock down your subcontractor compliance.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.