Every plumbing company owner has lived the same paradox. January is chaos — frozen pipe emergencies stack up, the phone rings nonstop, overtime hours pile on — and by March the bank account looks great. Then October hits, the phone slows down, but payroll doesn’t. Insurance premiums renew. Truck payments keep drafting. The account balance drops $30K in six weeks and suddenly you’re wondering where it all went. Plumbing cash flow management isn’t about earning more revenue. It’s about controlling when money comes in versus when it goes out — across twelve months that never behave the same way twice.

For the full picture, see our complete guide to plumbing bookkeeping. This post goes deep on the cash flow mechanics that keep plumbing companies between $1M and $10M solvent through seasonal swings, slow-paying GCs, and the gap between accrual profit and actual cash in the bank.

Understanding your revenue cycle by season is the first step toward managing it. Plumbing demand follows predictable regional patterns, but the timing and intensity vary.

Winter (December-February) brings frozen pipe emergencies in cold-climate states — burst pipes, water heater failures, emergency drain thaws. Revenue spikes are real but unpredictable. You might bill $180K in January and $95K in February. Emergency work commands premium pricing (often 1.5-2x standard rates), but you’re also paying overtime, after-hours premiums, and burning through truck stock faster than normal. In southern states, winter is a moderate slowdown.

Spring (March-May) is peak season almost everywhere. Remodel projects launch, new construction breaks ground, and homeowners tackle deferred maintenance. This is your highest-volume, most predictable revenue window. Service calls stay steady while project revenue ramps up.

Summer (June-August) holds steady. New construction continues, AC-related plumbing work (condensate drains, water heaters stressed by demand) fills gaps, and commercial tenant improvements keep crews busy. Revenue is consistent but rarely peaks.

Late fall (September-November) is the danger zone. Residential remodel work dries up. New construction projects push toward completion (fewer new starts). Homeowners stop calling unless something breaks. Revenue can drop 20-35% from peak months while your fixed costs stay flat.

Here’s what this looks like for a typical $2M plumbing company:

| Month | Revenue | Fixed Costs | Variable Costs | Net Cash Flow |

|---|---|---|---|---|

| January | $210,000 | $95,000 | $84,000 | +$31,000 |

| February | $155,000 | $95,000 | $62,000 | -$2,000 |

| March | $195,000 | $95,000 | $78,000 | +$22,000 |

| April | $215,000 | $95,000 | $86,000 | +$34,000 |

| May | $220,000 | $95,000 | $88,000 | +$37,000 |

| June | $185,000 | $95,000 | $74,000 | +$16,000 |

| July | $175,000 | $95,000 | $70,000 | +$10,000 |

| August | $170,000 | $95,000 | $68,000 | +$7,000 |

| September | $145,000 | $95,000 | $58,000 | -$8,000 |

| October | $130,000 | $95,000 | $52,000 | -$17,000 |

| November | $125,000 | $95,000 | $50,000 | -$20,000 |

| December | $155,000 | $95,000 | $62,000 | -$2,000 |

That’s roughly $108,000 in positive cash flow during the good months — and $49,000 in negative cash flow during the lean ones. The net is positive over 12 months, but the timing mismatch is what kills companies. If you spent your spring surplus on a new truck in June, you’ve got nothing to cover October’s shortfall.

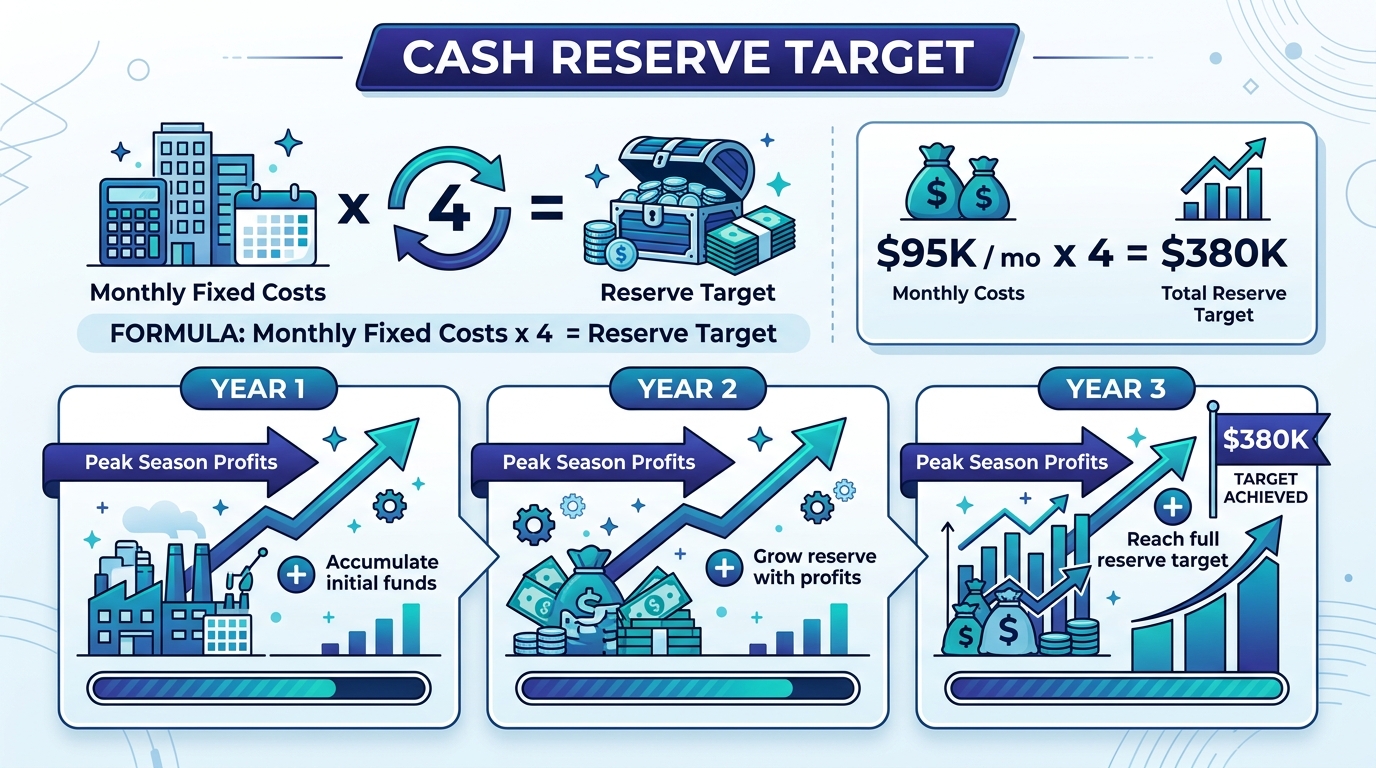

The single most important plumbing cash flow management discipline is building a cash reserve during peak months. Not a vague savings goal — a specific dollar target with a specific timeline.

The formula is simple: monthly fixed costs multiplied by 4. That’s your target reserve.

For a plumbing company running $95,000/month in fixed costs (rent, payroll for office staff, insurance, truck payments, software, loan payments), the target is $380,000. That covers the four months where revenue dips below breakeven — October through January — without touching a credit line.

Most companies can’t build that in one season. Here’s the realistic path:

The reserve sits in a separate high-yield business savings account — not your operating account. If it’s in the same account, it gets spent. Every owner says “I’ll just keep track mentally.” Nobody does.

New construction rough-ins, whole-house repipes, and commercial build-outs can run $15,000-$150,000+ per project. If you wait until project completion to invoice, you’re financing the general contractor’s project with your cash for 60-120 days. That’s not a business decision — it’s a cash flow trap.

Progress billing breaks the project into milestones and invoices at each one:

| Milestone | % Billed | Example ($50K Repipe) |

|---|---|---|

| Contract signed / mobilization | 30% | $15,000 |

| Rough-in complete / inspection passed | 30% | $15,000 |

| Trim-out / fixtures set | 30% | $15,000 |

| Final punch list / completion | 10% | $5,000 |

This structure means you’re collecting $15,000 within two weeks of starting work instead of waiting three months for the full $50,000. On five concurrent projects, that’s $75,000 in accelerated cash — enough to cover an entire slow month.

Set progress billing terms in your contract before work begins. Don’t try to negotiate milestone payments after the project is underway. The contract should specify exact milestones, invoice amounts, and payment terms (Net 15 for progress payments, not the GC’s standard Net 30-45).

Commercial and new construction plumbing work creates a receivables problem that residential service companies never face. General contractors routinely pay on 60-90 day cycles. Some stretch to 120 days. And on top of that, most commercial contracts include retainage holdbacks of 5-10% — money withheld until the entire project reaches substantial completion, which could be 6-12 months away.

Here’s the math on a $100,000 commercial rough-in contract with 10% retainage:

Your actual collection timeline: $90K at day 75, $10K at day 180. Meanwhile, you paid labor and materials out of pocket starting on day one.

This is why plumbing companies doing significant commercial work need more aggressive cash flow management than pure residential shops. Three strategies help:

Track retainage as a separate receivable. In QuickBooks, create a “Retainage Receivable” account so you can see exactly how much cash is tied up in holdbacks at any given time. A $3M company doing 40% commercial work might have $50K-$120K in retainage outstanding at any moment.

Set credit limits per GC. If a GC owes you $80K and is 60 days past due, don’t start a new $45K project for them. Your exposure is already too high.

Negotiate retainage release at milestones. Some GCs will release retainage on completed phases rather than holding it until the full project closes. A 5% retainage released at rough-in inspection is better than 10% held for six months.

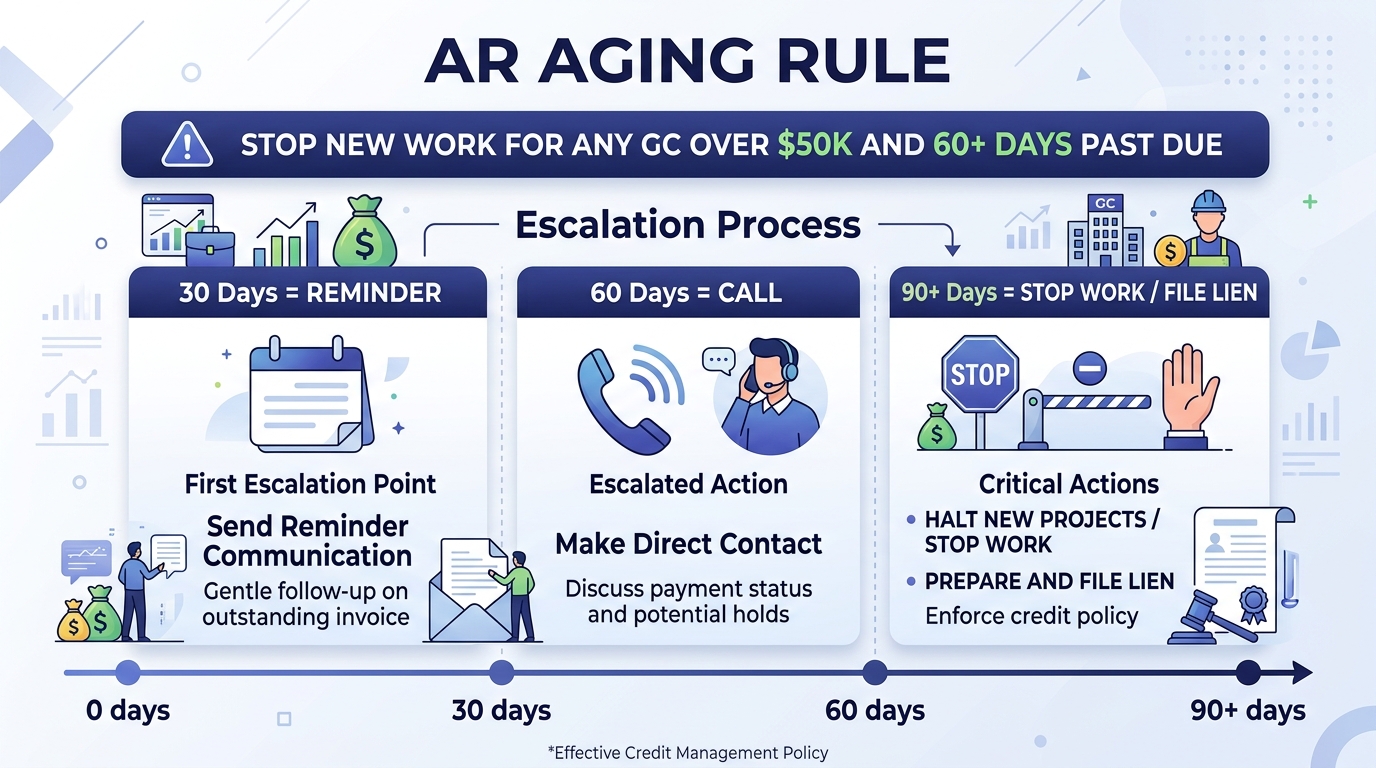

Slow receivables don’t fix themselves. You need a systematic collections workflow tied to your AR aging report. Here’s what works for plumbing companies:

30 days past due: Friendly email reminder with the original invoice attached. “Just checking in — we show invoice #4821 for $12,400 is now past 30 days. Can you confirm payment status?” Most legitimate oversights get resolved here.

45 days past due: Phone call to the project manager or AP contact. Document the conversation. Get a specific payment date commitment. Follow up in writing: “Per our conversation, confirming payment of $12,400 will be issued by [date].”

60 days past due: Escalate to the GC’s owner or controller. Send a formal demand letter via certified mail. Reference your contract terms. Mention that you’ll be pausing any in-progress work until the account is brought current.

90 days past due: Decision time. For amounts over $5,000, consult with a construction attorney about filing a mechanics lien. In most states, you have 60-90 days from last day of work to file. Miss that window and you lose the right. For amounts under $5,000, weigh the cost of collection against the balance and decide whether to pursue or write off.

The hard rule: Stop performing new work for any customer over 60 days past due. Period. Every week you keep working while they don’t pay, your exposure grows. This is the most violated cash flow principle in the trades — and the one that sinks the most companies.

The most cash-flow-stable plumbing companies have one thing in common: recurring revenue from maintenance contracts. Service agreements provide predictable monthly or annual income that doesn’t depend on weather, construction cycles, or emergency calls.

Profitable service agreement offerings for plumbing companies include:

A plumbing company with 200 residential service agreements at $250/year generates $50,000 in predictable annual revenue — roughly one full month of operating costs covered before a single service call comes in. Scale that to 500 agreements and you’ve covered your slowest quarter.

Service agreements also create high-value customer relationships that generate emergency and project revenue on top of the contract value. Agreement customers call you first when something breaks. They don’t price-shop. They convert at higher rates on recommended repairs.

This is the cash flow issue that confuses more plumbing company owners than any other. Your accrual-basis P&L shows $180K in net profit for the year. Your CPA confirms it. But your bank account is lower than it was 12 months ago. How?

Accrual accounting recognizes revenue when earned, not when collected. That $85,000 in outstanding receivables? It’s already counted as revenue on your P&L. The $22,000 in retainage holdbacks? Also counted. Your profit is real on paper, but the cash hasn’t arrived yet.

Add in principal payments on equipment loans (which reduce your balance sheet liability but don’t show on the P&L as expenses), owner distributions, and the timing of quarterly tax payments — and it’s entirely possible to be profitable on an accrual basis while running negative on cash.

The fix is running two views of your business: the accrual P&L (which tells you if you’re profitable) and a cash flow statement (which tells you if you can make payroll). Your bookkeeper should produce both monthly. If your accountant only gives you a P&L and balance sheet, you’re missing the report that actually prevents insolvency. Consider getting a free assessment to see where the gaps are.

A 13-week rolling cash flow forecast is the most practical forecasting tool for plumbing companies. It’s short enough to be accurate, long enough to see trouble coming, and simple enough that you’ll actually maintain it.

Here’s how to build one:

Week 1: Start with your current bank balance. Add expected deposits (invoices due this week, scheduled service agreement payments). Subtract expected outflows (payroll, rent, insurance drafts, material supplier payments, truck payments).

Weeks 2-4: Use your AR aging report for expected inflows and your AP aging plus recurring obligations for outflows. Flag any week where the projected ending balance drops below your minimum operating balance (typically $30K-$75K for a $1M-$3M company).

Weeks 5-13: Project based on historical seasonal patterns and your current backlog. This is where you spot the October cash crunch in July — early enough to build reserves, delay discretionary spending, or arrange a credit line.

Update it every Monday. It takes 20 minutes once the template is built. Those 20 minutes will save you from the “surprise” cash crisis that isn’t actually a surprise — it’s a failure to forecast.

A business line of credit is insurance against cash flow gaps — and like all insurance, you need to secure it before you need it. Banks approve credit lines based on financial health. Apply when your books look strong (spring, after a profitable year) rather than in October when your balance is dropping.

How much: For plumbing companies between $1M and $3M in revenue, a $50,000-$200,000 line of credit provides adequate coverage for seasonal gaps and slow-paying receivables. The SBA recommends maintaining access to working capital equal to 2-3 months of operating expenses.

When to draw: Use the line of credit for timing mismatches, not for operating losses. If you’re drawing because a $60K receivable is 45 days late but the money is coming, that’s a legitimate use. If you’re drawing because your monthly expenses exceed your monthly revenue and there’s no receivable coming to cover it, that’s a warning sign — not a cash flow problem, but a profitability problem.

When to use cash instead: If your reserve fund can cover the gap without dropping below your minimum balance (one month of fixed costs), use cash. Line of credit interest — even at 8-10% — adds up when you’re carrying a balance for weeks at a time.

Every strategy in this article depends on one thing: accurate, timely financial data. You can’t build a 13-week forecast if your books are two months behind. You can’t manage AR aging if invoices aren’t entered when work is completed. You can’t calculate your cash reserve target if you don’t know your real monthly fixed costs.

The plumbing companies that survive seasonal swings aren’t the ones with the most revenue. They’re the ones whose job costing is tight, whose receivables are tracked weekly, and whose bookkeeping gives them the visibility to act before problems become crises.

Related Reading:

– The Complete Guide to Plumbing Bookkeeping

– Job Costing for Plumbing Contractors

– Bookkeeping Services for Plumbing Contractors

Ready to get your plumbing company’s cash flow under control? Steph’s Books provides outsourced bookkeeping built for trade contractors — including 13-week cash flow forecasts, AR aging management, and monthly financial reporting that shows you both profit and cash position. Get a free quote and see what’s possible.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.