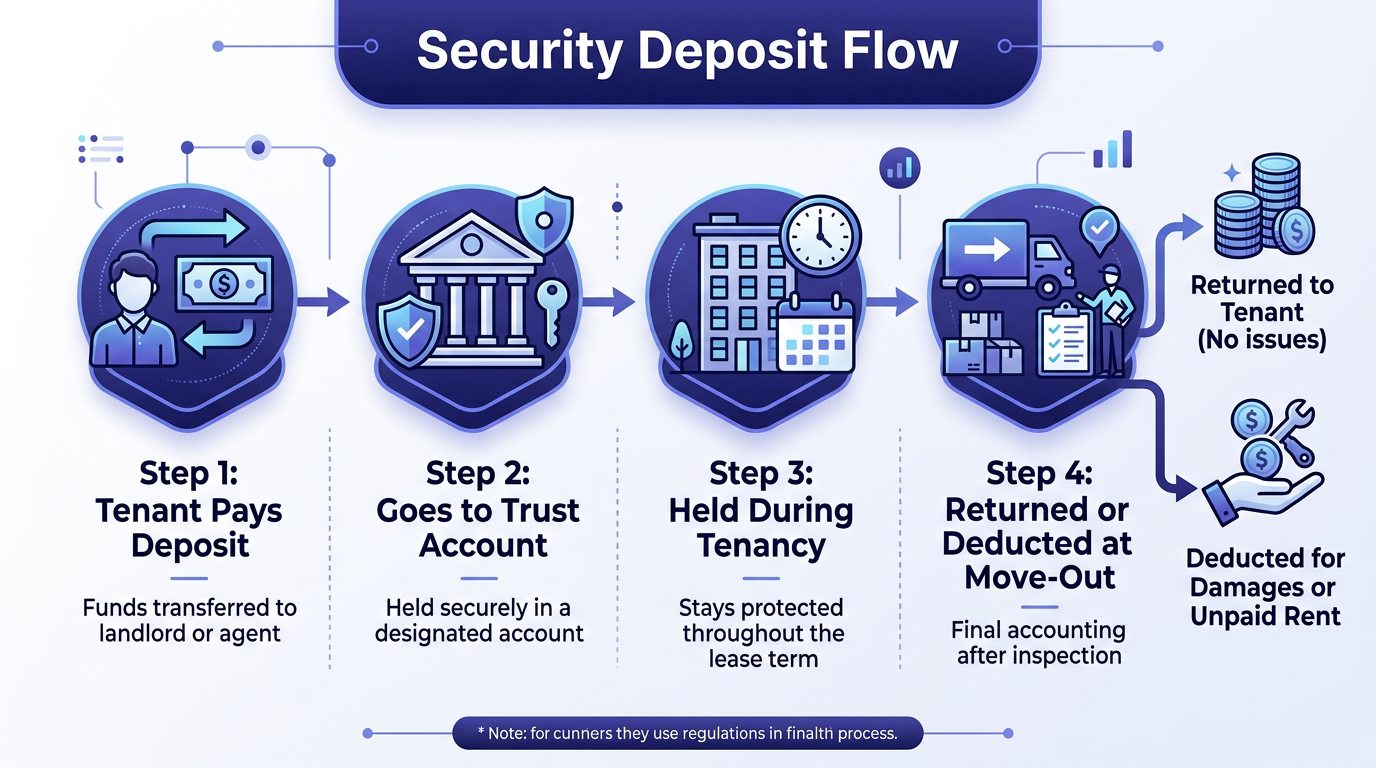

One of the most consequential accounting mistakes property managers make is treating security deposits as income. The moment a tenant hands over a security deposit, that money does not belong to you or the property owner. It belongs to the tenant until the lease ends and you have documented, lawful reasons to retain any portion of it.

In accounting terms, a security deposit is a liability. It sits on your balance sheet under current or long-term liabilities — never on your income statement. When you receive a $2,000 security deposit, your cash increases by $2,000 and your security deposit liability increases by $2,000. Revenue stays untouched.

This distinction matters for more than just clean books. Misclassifying deposits as revenue inflates your reported income, distorts owner distribution reports, and can trigger serious legal exposure. Courts in nearly every state treat commingling or misappropriating security deposits as a violation that can result in treble damages, attorney fee awards, and statutory penalties.

If you are managing 50 or more units, the aggregate deposit liability can easily exceed $100,000. That is not a rounding error — it is a fiduciary obligation that demands precise tracking.

Important: Security deposits must be recorded as liabilities from the day they are received. Recognizing deposit funds as revenue — even temporarily — violates GAAP and most state landlord-tenant statutes.

Most states require property managers to hold security deposits in a dedicated trust account (sometimes called an escrow account) that is separate from operating funds. This is not a suggestion. It is a legal requirement with teeth.

A properly structured chart of accounts for property management should include:

Some states allow you to hold deposits in a single pooled trust account. Others require individual accounts per tenant. A few permit you to post a surety bond instead of holding cash. The rules vary — and getting them wrong is expensive.

Trust account bank statements should be reconciled monthly, just like your operating accounts. Any discrepancy between your ledger balance and the bank balance needs immediate investigation. Regulators and auditors look at trust account reconciliation first when examining a property management firm.

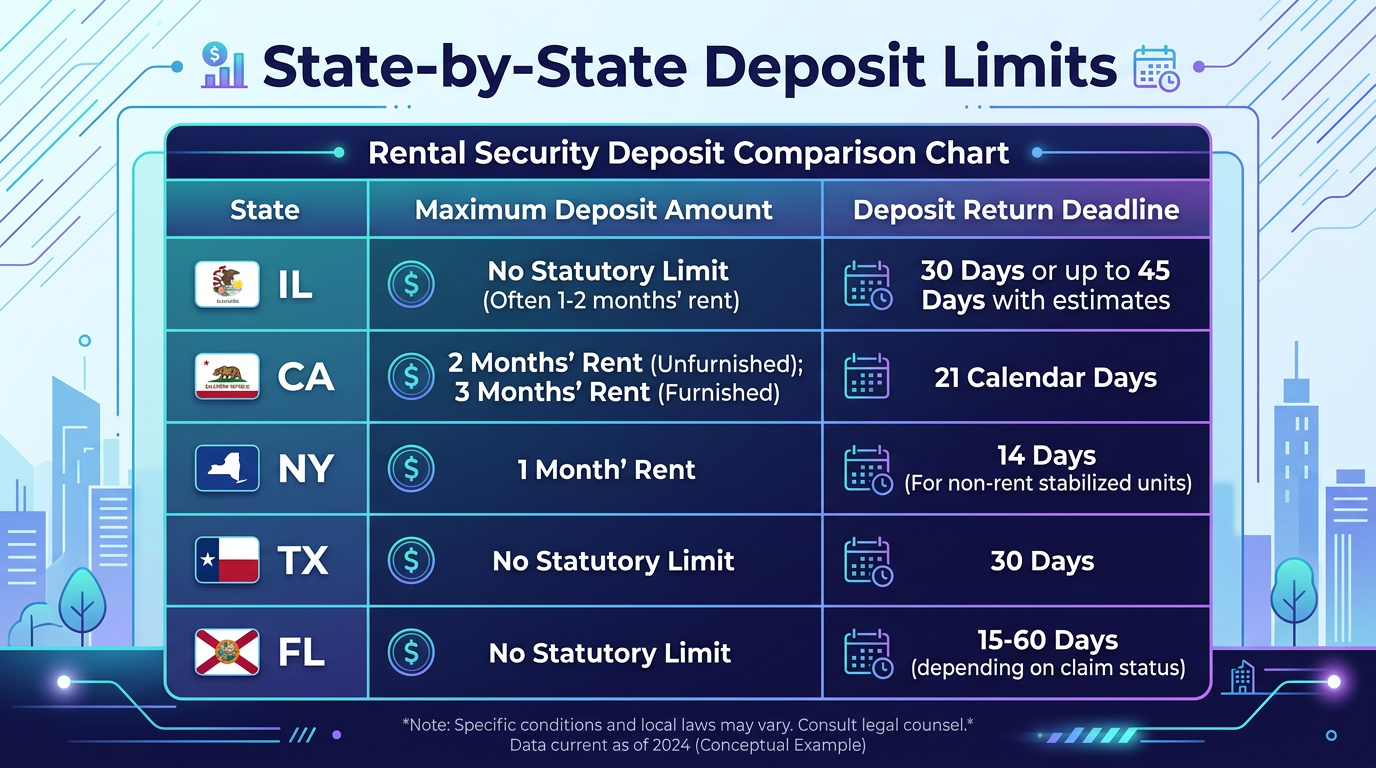

Security deposit regulations vary dramatically across states. What is perfectly legal in Texas could expose you to triple damages in Massachusetts. If you manage properties in multiple states — or even one state with complex rules — you need to know the specifics.

Here is a comparison of key rules for six major states:

| State | Max Deposit | Trust Account Required | Interest Required | Return Deadline | Penalties for Non-Compliance |

|---|---|---|---|---|---|

| Illinois | 1.5x monthly rent | Yes | Yes (25+ units, on deposits held 6+ months) | 30 days (45 if deductions) | 2x deposit + attorney fees |

| California | 1x monthly rent (unfurnished), 2x (furnished) | No (but must not commingle) | No | 21 days | Statutory damages up to 2x deposit |

| New York | 1x monthly rent | Yes (separate from personal funds) | Yes (buildings with 6+ units) | 14 days | Forfeiture of right to retain deposit |

| Texas | No statutory limit | No | No | 30 days | 3x wrongfully withheld amount + $100 + attorney fees |

| Florida | No statutory limit | Yes (separate account required) | Optional (but must notify tenant of terms) | 15 days (if no deductions), 30 days (with deductions) | Forfeiture of right to claim against deposit |

| Massachusetts | 1x monthly rent | Yes (separate, interest-bearing) | Yes (5% annually or actual bank rate) | 30 days | 3x deposit + attorney fees + court costs |

This table is a starting point, not a substitute for legal counsel. State laws change, and local ordinances in cities like Chicago, New York City, and San Francisco often impose additional requirements on top of state rules. Consult Nolo’s state-by-state security deposit guide or your state attorney general’s office for the most current statutes.

Pro Tip: Build a compliance calendar in your property management system that auto-triggers deposit return tasks based on state-specific deadlines. A missed deadline in New York (14 days) or Florida (15 days) can cost you the entire deposit — regardless of legitimate damages.

Several states require landlords and property managers to hold security deposits in interest-bearing accounts and pay that interest to the tenant. Illinois, New York, Massachusetts, Connecticut, Maryland, Minnesota, New Jersey, New Mexico, North Dakota, and Virginia all have some form of interest requirement — though the specifics differ.

In Illinois, for example, if you manage a property with 25 or more units in a municipality with a population over 25,000, you must pay interest on deposits held for more than six months. The rate is set annually by the city (in Chicago, it is published each January). Failure to pay the required interest entitles the tenant to the full deposit back plus penalties.

From an accounting standpoint, interest-bearing deposit accounts require:

For managers with hundreds of units, the interest calculations can become complex. Your property management accounting software should handle per-tenant interest tracking automatically. If it does not, you need a supplemental spreadsheet or a better system.

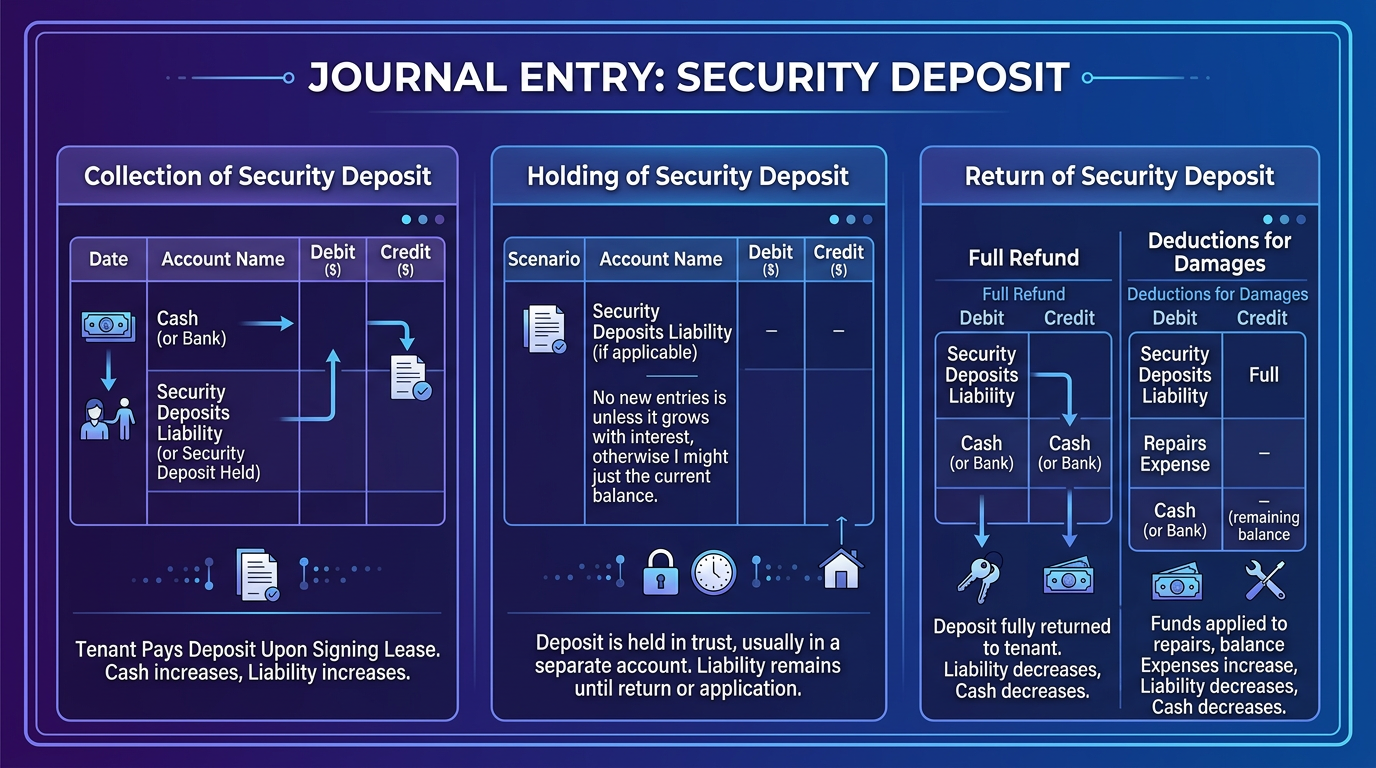

When a new tenant moves in and pays a security deposit, the journal entry is straightforward:

Move-in — Security deposit received ($2,000):

| Account | Debit | Credit |

|---|---|---|

| Cash — Security Deposit Trust Account | $2,000 | |

| Security Deposits Held (Liability) | $2,000 |

Notice that this entry touches the balance sheet only. No revenue is recognized. The cash goes into the trust account, and a corresponding liability is recorded. If you are tracking deposits at the tenant level (which you should be), this entry also creates a sub-ledger record tied to the specific lease.

If the tenant also pays first and last month’s rent at move-in, those amounts are recorded separately — rent goes to revenue or prepaid rent, while the deposit remains a liability.

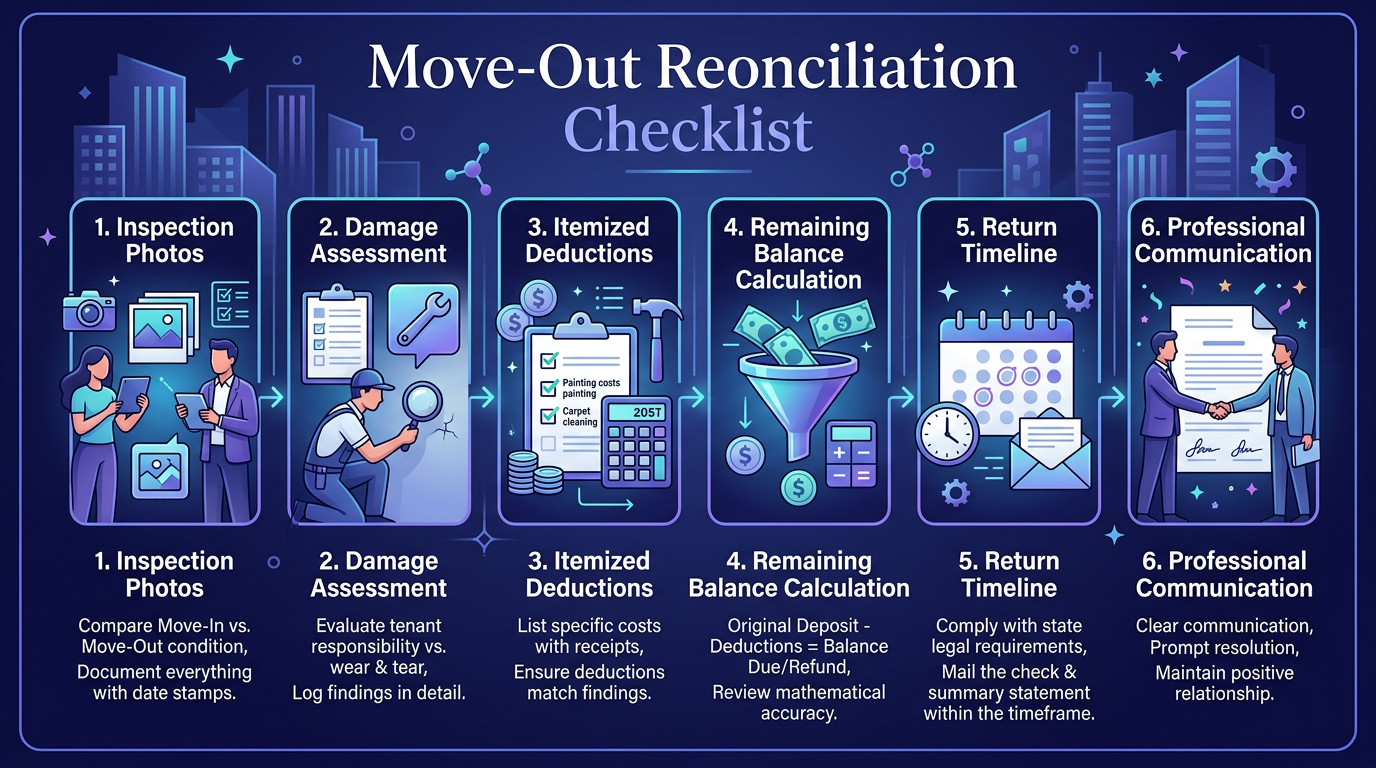

Move-out accounting is where security deposit management gets complicated. When a tenant vacates, you need to inspect the unit, document any damages beyond normal wear and tear, calculate deductions, and return the remaining balance — all within your state’s statutory deadline.

Scenario: Tenant moves out. $600 withheld for damages, $1,400 returned.

| Account | Debit | Credit |

|---|---|---|

| Security Deposits Held (Liability) | $2,000 | |

| Cash — Security Deposit Trust Account | $1,400 | |

| Maintenance/Repair Expense (or Owner Revenue) | $600 |

The $600 deduction is only now recognized as revenue or allocated to repair expense — not before. The liability is fully relieved, and the trust account balance decreases by the full $2,000 (the returned portion plus the retained portion transferred to operating).

Full refund scenario ($2,000 returned, no deductions):

| Account | Debit | Credit |

|---|---|---|

| Security Deposits Held (Liability) | $2,000 | |

| Cash — Security Deposit Trust Account | $2,000 |

Clean and simple. The liability is zeroed out, and the trust account balance drops accordingly.

Courts overwhelmingly side with tenants when property managers cannot produce detailed documentation supporting deposit deductions. “The carpet was stained” is not sufficient. You need evidence.

A defensible damage deduction file should include:

Most states require you to send the tenant an itemized statement along with any remaining deposit balance. Some states (like California) require you to provide copies of repair invoices or estimates. Keep every document for at least 4-7 years after the tenant vacates.

Critical: Never deduct for pre-existing conditions. If you did not document the unit’s condition at move-in with photos and a signed checklist, you have essentially waived your right to claim damages. Courts will assume the unit was in the condition the tenant describes.

Missing a deposit return deadline is one of the fastest ways to lose a security deposit dispute — even when the deductions are legitimate. Many state statutes provide that failure to return the deposit within the required timeframe automatically forfeits the landlord’s right to retain any portion.

Best practices for return timeline compliance:

For multi-state portfolios, this is where a structured process inside your property management accounting system becomes indispensable. A 14-day deadline in New York and a 30-day deadline in Texas require different workflows, and a manual tracking system will eventually fail.

Security deposit disputes are among the most frequently litigated issues in landlord-tenant law. Many of these lawsuits are entirely preventable. Here are the mistakes that generate the most legal exposure for property managers:

1. Commingling deposits with operating funds. This is the cardinal sin. If your security deposits sit in the same bank account as rent collections and vendor payments, you are violating trust accounting rules in most states. Even one commingling violation can result in penalties applied to your entire portfolio.

2. Failing to provide an itemized deduction statement. Withholding $800 for carpet cleaning means nothing if you did not send a written, itemized breakdown to the tenant within the statutory deadline. Many states treat the absence of an itemized statement as an automatic forfeiture of the right to retain any funds.

3. Charging for normal wear and tear. Faded paint after a 5-year tenancy is wear and tear. Holes punched in drywall are damages. Courts draw this line strictly, and property managers who cannot articulate the difference lose.

4. Missing the return deadline. As discussed above, a late return — even by one day — can result in statutory penalties of 2-3x the deposit amount plus attorney fees.

5. Not tracking deposits at the unit/tenant level. If you manage 200 units with a pooled trust account and cannot produce an individual ledger showing each tenant’s deposit balance, receipt date, and any interest accrued, you have a reconciliation problem that will surface at the worst possible time.

6. Deducting for cleaning when the unit was not clean at move-in. If you do not have a signed move-in checklist documenting the unit’s condition, you cannot credibly claim the tenant left it in worse shape.

7. Ignoring local ordinances. Chicago, San Francisco, Seattle, Washington D.C., and dozens of other cities have deposit regulations that exceed state requirements. Managing to state law alone is not sufficient in these jurisdictions.

Security deposit accounting is not glamorous, but it is one of the highest-risk areas in property management finance. The combination of strict state regulations, fiduciary trust obligations, and aggressive tenant attorneys means that sloppy deposit management will eventually cost you — in penalties, legal fees, and reputation.

The property managers who avoid these problems share a few common traits: they use dedicated trust accounts with monthly reconciliation, they document everything with photos and signed checklists, they track deposits at the individual tenant level, and they have automated systems that enforce return deadlines.

If your current accounting setup cannot handle these requirements reliably, it is time to upgrade your processes — or bring in a team that specializes in property management accounting.

Ready to get your property management accounting right? Steph’s Books specializes in bookkeeping for property managers — including trust account management, security deposit tracking, and owner reporting. Schedule a free consultation and let us handle the complexity so you can focus on growing your portfolio.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.