Most plumbing contractors pay more in federal and state taxes than they need to — not because they are cheating themselves, but because they are missing deductions that are perfectly legal and sitting right in front of them. The average plumber tax deductions gap we see at Steph’s Books is $5,000 to $15,000 per year in unclaimed write-offs. That is real money left on the table because nobody organized the receipts, categorized the expenses correctly, or knew the IRS rules well enough to apply them.

For the full picture, see our complete guide to plumbing bookkeeping. This post narrows the focus to the specific tax deductions plumbing contractors should be claiming in 2026 — from Section 179 on work trucks to 1099 penalties for subcontractors. If you are a plumbing company owner doing $1M to $10M in revenue, treat this as your year-end checklist.

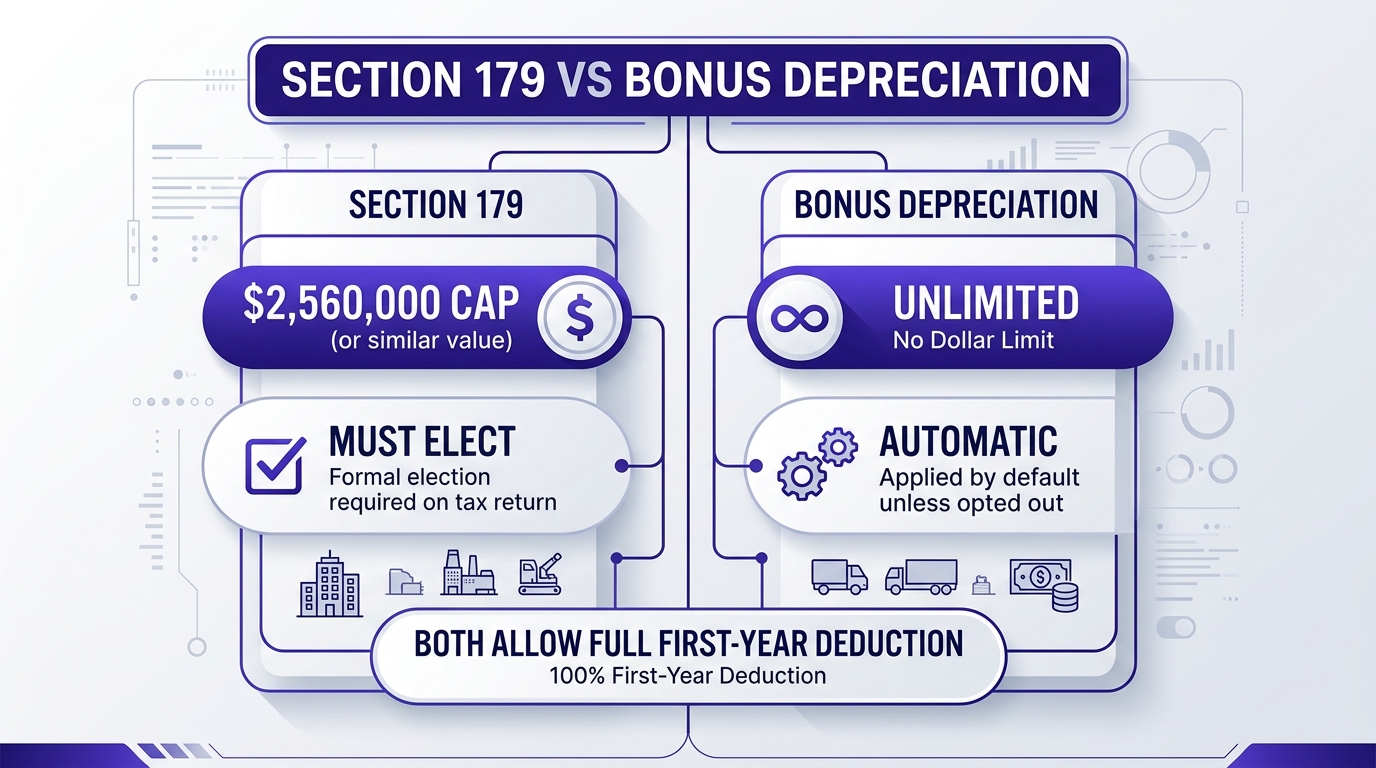

The single biggest deduction most plumbing contractors miss is Section 179 — the IRS provision that lets you deduct the full purchase price of qualifying equipment in the year you buy it, instead of depreciating it over 5-7 years.

A work truck is the most expensive asset most plumbing companies buy. Under IRS Section 179, if your vehicle has a gross vehicle weight rating (GVWR) over 6,000 pounds, you can deduct the full purchase price in year one — up to the Section 179 limit of $1,250,000 for tax year 2025 (indexed annually for inflation).

That means a $50,000 Ford F-250 or Ram 2500 (both over 6,000 lb GVWR) can be written off entirely in the year of purchase. A lighter van under 6,000 lb GVWR is subject to the luxury auto depreciation limits, which cap your first-year deduction at roughly $20,400.

Practical impact: A plumbing company that buys two work trucks at $50,000 each and expense them under Section 179 saves approximately $24,000 in federal taxes (at the 24% bracket) compared to straight-line depreciation over five years. That is cash flow you keep in year one instead of waiting half a decade.

Section 179 applies to far more than trucks. Qualifying plumbing equipment includes:

All of this can be deducted in full in the year of purchase under Section 179, rather than depreciated over the asset’s useful life.

In addition to Section 179, 100% bonus depreciation was restored for assets placed in service starting in 2025. This is significant because bonus depreciation has no dollar cap (unlike Section 179’s $1,250,000 limit) and can create a net operating loss that carries forward. For plumbing companies making large capital investments — fleet replacements, shop buildouts, major equipment purchases — bonus depreciation can be more powerful than Section 179 alone.

Here is where most plumbing contractors leave money on the table without realizing it. The IRS de minimis safe harbor rule lets you immediately expense any item costing $2,500 or less per item (or per invoice) — no depreciation schedule required. You just need to elect it on your tax return and have a written accounting policy in place.

For plumbers, this covers nearly every hand tool and small power tool you buy:

Anything over $2,500 must be capitalized and depreciated — unless it qualifies for Section 179 or bonus depreciation. The distinction matters because the de minimis rule is simpler (no asset tracking required) and applies even if you have already exhausted other deduction thresholds.

The mistake we see: Plumbing companies that do not have a written de minimis policy end up capitalizing $800 wrenches and depreciating them over seven years. That is pennies of annual depreciation on items that should have been fully expensed on day one.

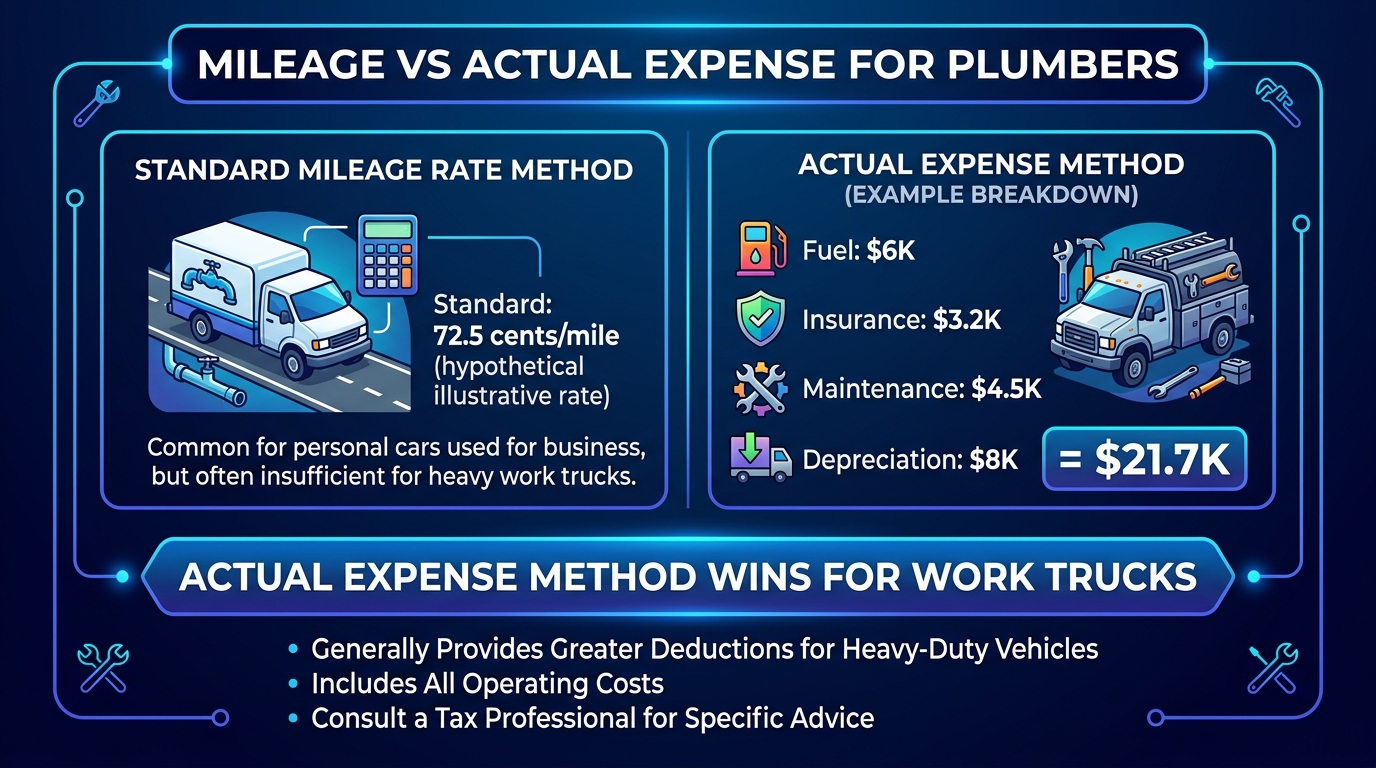

Plumbing contractors have two options for deducting vehicle expenses: the IRS standard mileage rate (72.5 cents per mile in 2025) or the actual expense method (fuel, insurance, repairs, depreciation, registration, tolls).

For most plumbing companies with dedicated work trucks that are used 100% for business, the actual expense method almost always wins. Here is why:

The standard mileage rate tends to favor employees with personal cars who occasionally drive for business. It rarely favors trade contractors with heavy-duty work vehicles.

Important: Once you claim actual expenses on a vehicle, you cannot switch to the standard mileage rate for that vehicle in later years. Choose carefully in year one.

These are fully deductible business expenses that plumbing contractors sometimes underreport because they are paid annually or semi-annually and slip through the cracks.

Insurance is one of the largest overhead line items for plumbing companies:

| Insurance Type | Typical Annual Cost | Deductible? |

|---|---|---|

| General liability (GL) | ~$4,361/year (industry average) | Yes — 100% |

| Workers’ compensation | ~$2.65 per $100 of payroll | Yes — 100% |

| Commercial auto | $2,400–$6,000/year per vehicle | Yes — 100% |

| Inland marine (tools/equipment) | $500–$1,500/year | Yes — 100% |

| Umbrella/excess liability | $1,200–$3,000/year | Yes — 100% |

| Surety bond premium | $500–$3,000/year (varies by bond amount) | Yes — 100% |

Workers’ comp alone on a plumbing company with $1.5M in payroll runs roughly $39,750 per year at the $2.65/$100 rate. That is a material deduction.

Plumbing is a licensed trade, and the IRS allows deductions for education and training that maintains or improves skills required in your current business.

Deductible training expenses include:

Apprentice wages during training hours are particularly valuable because they are deductible as labor expense AND they build your licensed workforce pipeline.

Every dollar spent on personal protective equipment is deductible. For plumbing contractors, this includes:

Uniforms must be required as a condition of employment and not suitable for everyday wear to qualify. Company-branded polos with your logo meet this test. Plain khakis do not.

If you pay a subcontractor $600 or more in a calendar year, you are required to file Form 1099-NEC with the IRS and provide a copy to the sub. This is not optional.

The penalty for failure to file is $310 per form in 2025 (indexed for inflation). A plumbing company that uses 20 subs and misses every 1099 is looking at $6,200 in penalties — for a filing requirement that takes an afternoon with proper bookkeeping.

What you need from every sub before you pay them:

Get the W-9 before the first payment, not during January’s 1099 scramble.

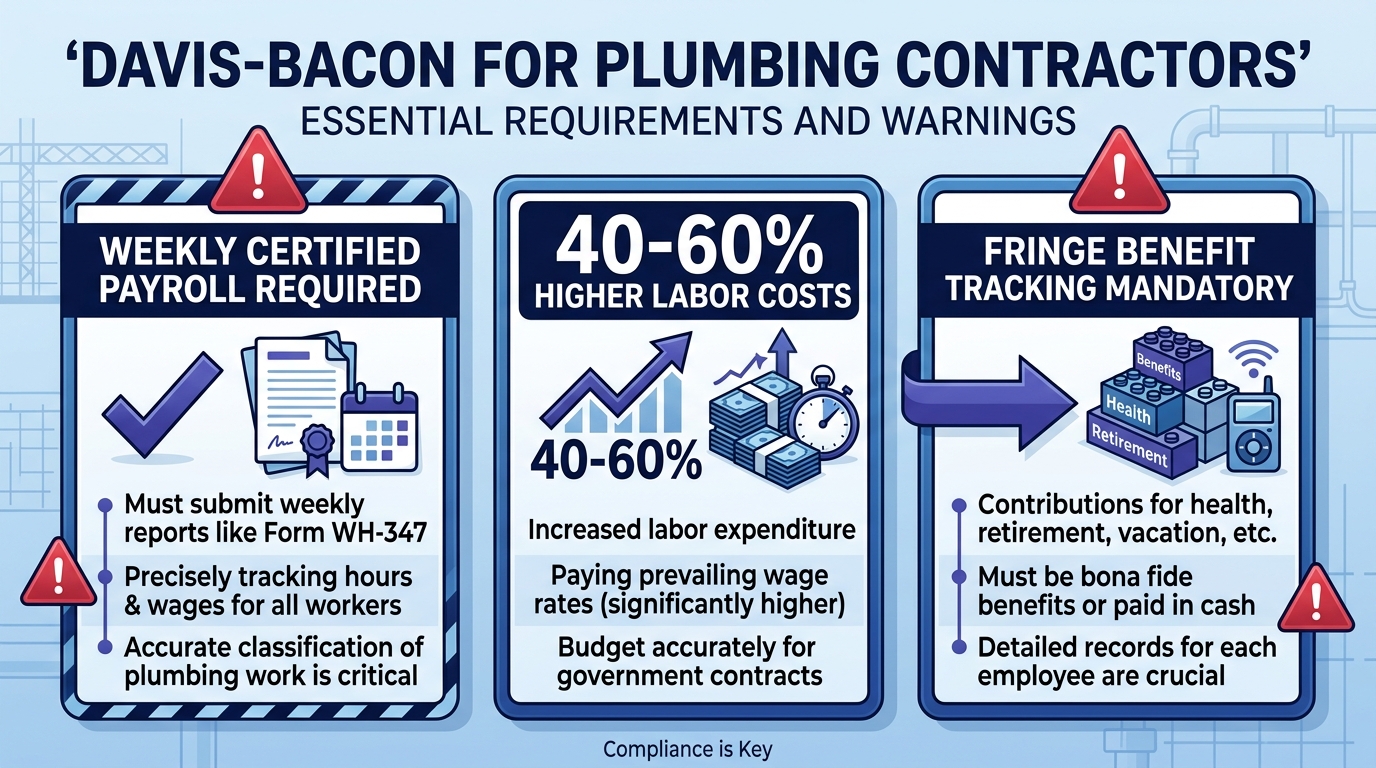

Plumbing contractors who bid on municipal water and sewer projects, school construction, or federally funded infrastructure work must comply with Davis-Bacon prevailing wage requirements. These jobs require paying union-scale wages and benefits, which are higher than your standard labor rates.

The bookkeeping impact is significant:

If you are pursuing government work, your bookkeeping system needs to handle certified payroll and fringe benefit tracking. This is not something a general bookkeeper can improvise.

Here is a consolidated table of the most common plumber tax deductions with typical annual dollar amounts for a $2M-$4M plumbing company:

| Deduction Category | Typical Annual Amount | Notes |

|---|---|---|

| Section 179 — Vehicles (2 trucks) | $80,000–$120,000 | First-year deduction; 6,000+ lb GVWR |

| Section 179 — Equipment | $15,000–$50,000 | Cameras, jetters, pipe lining |

| De minimis tools (under $2,500 each) | $8,000–$15,000 | Hand tools, power tools, small equipment |

| Vehicle operating costs (actual method) | $24,000–$54,000 | Fuel, maintenance, insurance, 4-6 trucks |

| General liability insurance | $3,500–$6,000 | Industry avg ~$4,361 |

| Workers’ compensation | $25,000–$50,000 | $2.65/$100 payroll |

| Commercial auto insurance | $9,600–$24,000 | $2,400–$6,000/vehicle x 4-6 trucks |

| Licensing and permits | $1,500–$4,000 | State, city, specialty licenses |

| Training and education | $3,000–$8,000 | CEU, apprentice programs, certifications |

| Safety gear and uniforms | $2,000–$5,000 | PPE, branded uniforms |

| Subcontractor payments (1099-deductible) | $50,000–$200,000+ | Fully deductible as COGS |

| Software and technology | $3,000–$8,000 | ServiceTitan, QBO, fleet tracking |

Total potential deductions beyond standard expenses: $224,600–$544,000+

The gap between a plumbing company that claims all of these and one that misses Section 179, skips the de minimis election, and uses standard mileage instead of actual cost? $5,000 to $15,000 in unnecessary tax payments — every single year.

The pattern is consistent across the plumbing contractors we work with at Steph’s Books:

A specialized bookkeeper who understands trade contractor finances catches all five of these in the first month. A general bookkeeper who treats your plumbing company like a retail store will miss most of them indefinitely.

Ready to stop leaving deductions on the table? Steph’s Books specializes in bookkeeping for plumbing contractors. We set up your chart of accounts, track your Section 179 assets, handle 1099 filings, and make sure every deductible dollar gets claimed. Schedule a free assessment and find out what you have been missing.

Get a free quote and see how Steph's Books can save you 40-60% vs hiring in-house.