CAM reconciliation (Common Area Maintenance reconciliation) is the annual process where a property manager compares estimated CAM charges collected from tenants against actual maintenance costs incurred. If actual costs exceeded estimates, tenants owe the difference. If costs were lower, tenants receive a credit.

If you manage commercial properties, CAM reconciliation is the single most contentious financial process you’ll handle all year. One miscalculated share, one missing invoice, one late notice — and you’re fielding angry calls from tenants who already think their triple-net charges are too high.

The reality: most CAM disputes stem from sloppy reconciliation, not bad-faith charges. A 2024 BOMA International survey found that 43% of commercial tenants have disputed at least one CAM charge in the past three years. The majority of those disputes were resolved when the property manager provided better documentation — meaning the charges were legitimate, but the process failed.

This guide walks through the full CAM reconciliation cycle — from understanding what’s included to preventing disputes before they start. If you’re managing 50+ commercial units and billing $1M–$10M in operating expenses annually, this is the playbook.

Common Area Maintenance (CAM) charges are the tenant’s proportionate share of operating expenses for shared spaces and building systems. They’re a core component of triple-net (NNN) and modified gross leases, where tenants pay base rent plus their share of operating costs.

CAM charges typically fall into two buckets: controllable and uncontrollable expenses.

These are costs the property manager can influence through vendor negotiations, preventive maintenance, and operational decisions:

These are pass-throughs that the property manager has limited ability to reduce:

Pro Tip: Many leases include a CAM cap on controllable expenses — typically 3–5% annual increases. If your lease has a cap, it only applies to controllable expenses unless the lease language explicitly includes uncontrollables. Review every lease’s cap language before running reconciliation. Misstating what falls under the cap is the fastest way to trigger a tenant audit request.

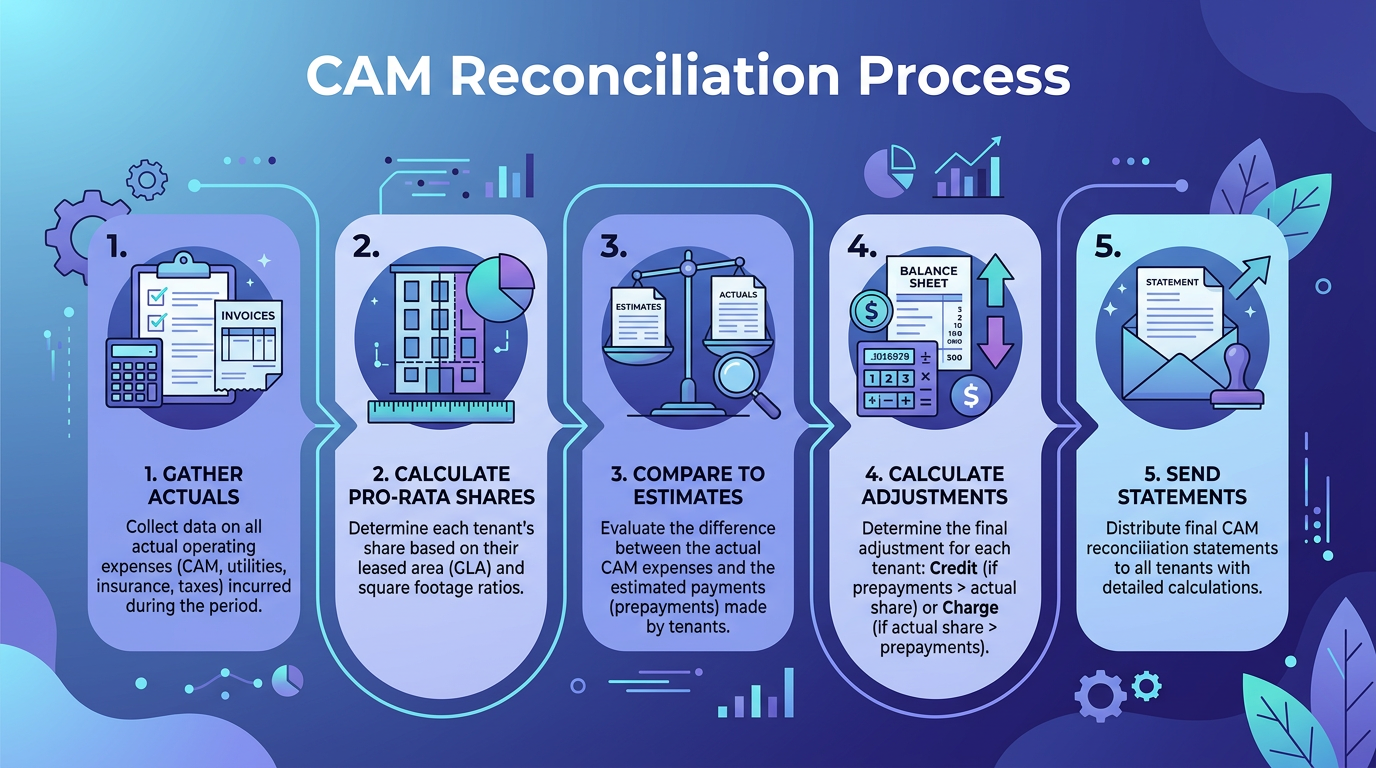

CAM reconciliation compares the estimated CAM charges billed to tenants throughout the year against the actual operating expenses incurred. The result is either a credit (tenants overpaid) or an additional charge (tenants underpaid).

Here’s the process, broken into phases:

Tenant’s Rentable Square Footage ÷ Total Building Rentable Square Footage = Pro Rata Share %

For a tenant occupying 3,200 sq ft in a 40,000 sq ft building: 3,200 ÷ 40,000 = 8.0%

Net amount due or credit

Review statements for accuracy before distributing. Have a second set of eyes — your bookkeeper, accountant, or operations manager — verify the math. A $500 error multiplied across 30 tenants becomes a $15,000 problem.

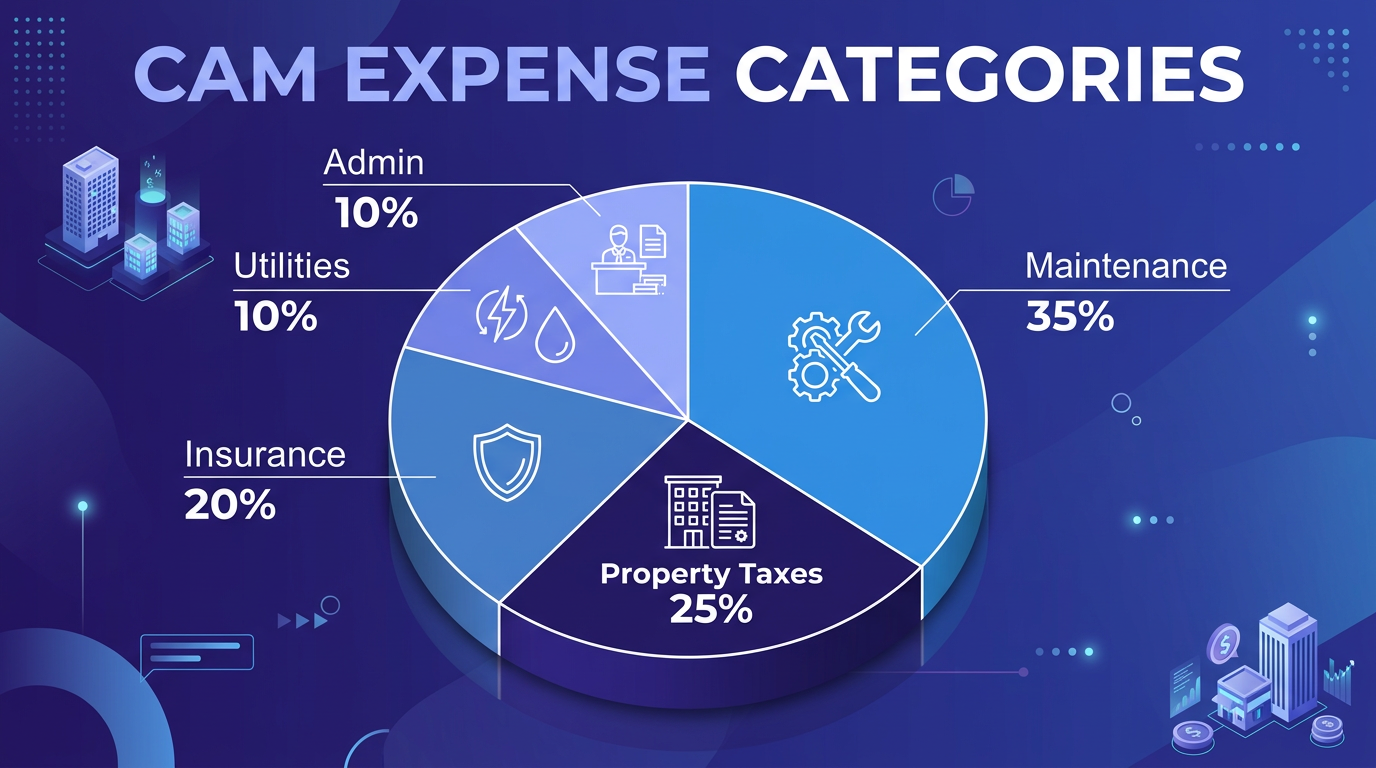

The table below shows typical CAM expense ranges for a Class B suburban office building (40,000–100,000 sq ft). Your numbers will vary by market, property type, and building age.

| Expense Category | Typical $/SF/Year | % of Total CAM | Notes |

|---|---|---|---|

| Property Taxes | $3.00–$8.00 | 25–35% | Varies widely by jurisdiction |

| Property Insurance | $0.75–$2.00 | 8–12% | Rising 5–10% annually in most markets |

| Utilities (Common Area) | $1.50–$3.50 | 12–18% | LED retrofits can cut 20–30% |

| Janitorial/Cleaning | $1.25–$2.50 | 10–15% | Day cleaning vs. night cleaning matters |

| Landscaping/Snow | $0.50–$1.50 | 5–8% | Seasonal variance; multi-year contracts save 10–15% |

| Repairs & Maintenance | $1.00–$3.00 | 10–18% | Preventive maintenance reduces spikes |

| Security | $0.50–$1.50 | 4–8% | Monitored vs. manned makes 3x cost difference |

| Management Fee | $0.75–$1.50 | 6–10% | Usually 3–6% of gross revenue |

| Trash/Recycling | $0.25–$0.75 | 2–4% | Compactor vs. dumpster changes cost significantly |

| Pest Control | $0.10–$0.30 | 1–2% | Quarterly service standard |

| Total CAM | $9.60–$24.55 | 100% | National average: ~$12–$16/SF |

Important: Management fees are a common audit trigger. Some leases exclude management fees from the CAM pool entirely. Others cap them at a fixed percentage (typically 3–5% of collected rents). Always confirm the lease language before including management fees in reconciliation.

After reviewing hundreds of CAM reconciliations for property management clients, these are the errors we see most frequently:

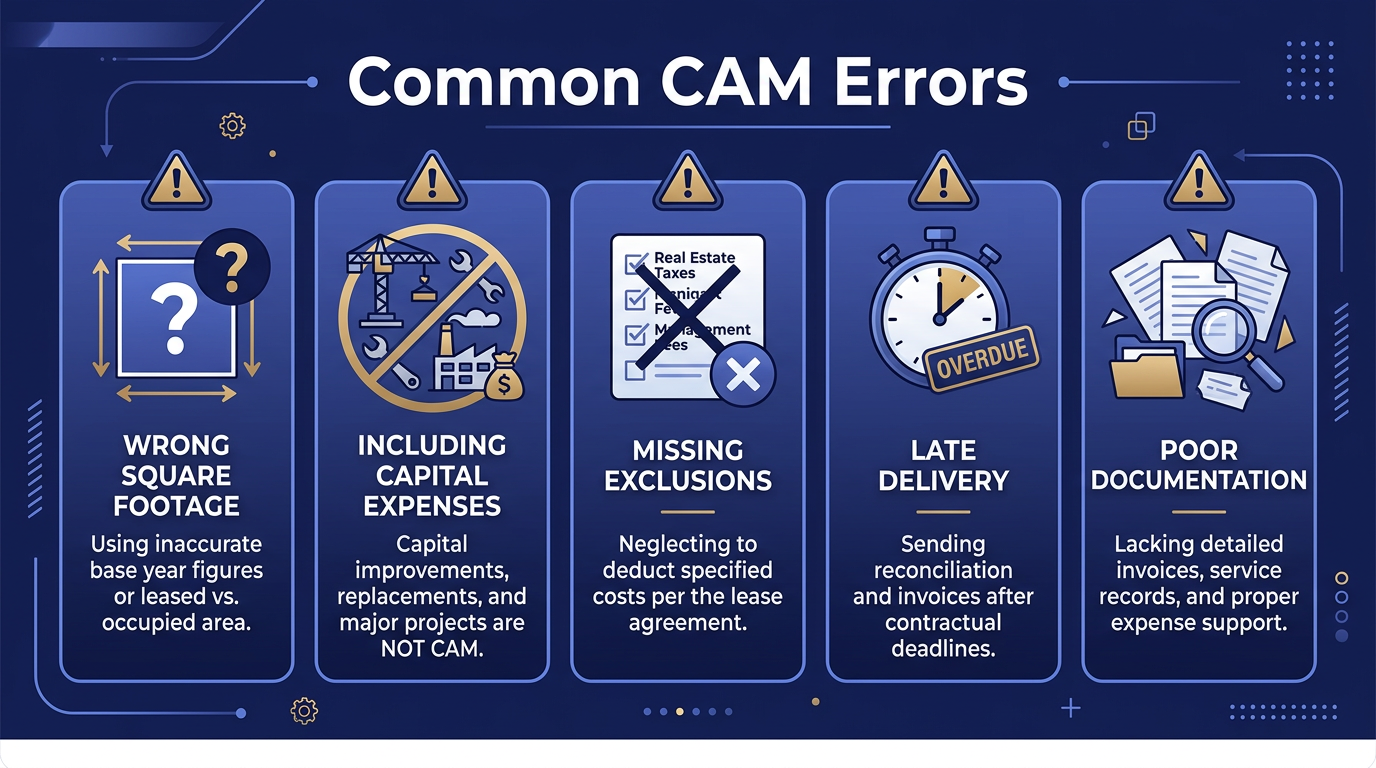

The mistake: A $45,000 parking lot resurfacing gets coded to “Repairs & Maintenance” instead of a capital account. Tenants see a 40% spike in R&M costs and immediately request an audit.

The fix: Establish a clear capitalization threshold in your chart of accounts — $5,000 is standard. Train your AP team to flag invoices above the threshold for capital review. If the lease allows amortized capital pass-throughs, amortize over the asset’s useful life (typically 10–15 years for structural, 5–7 years for mechanical).

The mistake: A tenant moves out June 30 and you bill them for the full year’s CAM share. Or a new tenant moves in September 1 and you don’t bill them at all because “they’ll catch up next year.”

The fix: Prorate to the day. For a tenant occupying 5,000 sq ft from January 1 through June 30 in a 50,000 sq ft building: (5,000 ÷ 50,000) × (181 ÷ 365) = 4.96% of annual CAM, not 10%.

The mistake: Your building is 70% occupied, but you bill tenants based on actual expenses. Those tenants are effectively subsidizing vacant space because fixed costs (security, insurance, management fees) don’t decrease proportionally with vacancy.

The fix: Most leases include a gross-up clause allowing you to adjust variable expenses to what they would have been at 95% occupancy. Apply gross-up to variable expenses only (utilities, janitorial) — not fixed costs like property taxes.

The mistake: Your lease requires statements within 120 days of year-end, but you don’t finish until July because of late vendor invoices and staff turnover.

The fix: Build a reconciliation calendar (see the timeline section below). Accrue December expenses by January 15. Start compiling actuals by February 1. Leave a 30-day buffer before the lease deadline.

Critical: In several states, missing your contractual reconciliation deadline means you forfeit the right to collect shortfalls for that year. The cost of late reconciliation isn’t just tenant frustration — it’s real revenue loss.

The best CAM reconciliation in the world means nothing if tenants don’t trust the numbers. Dispute prevention starts long before you send the statement.

Send tenants a brief notice in October or November letting them know:

This eliminates the element of surprise. A tenant who knows a 6% increase is coming reacts very differently than one who opens an unexpected invoice.

Your reconciliation statement should include:

Most commercial leases give tenants the right to audit CAM charges, typically within 12–24 months of receiving the reconciliation statement. When an audit request comes in: respond promptly, provide organized GL detail and vendor invoices by category, designate a single point person, and be prepared to issue corrected statements immediately if the audit finds legitimate errors. Fighting a valid finding destroys trust and invites legal escalation.

Manual CAM reconciliation in spreadsheets works for a 5-unit strip mall. It breaks down catastrophically at 50+ units across multiple properties. Here’s what works at scale:

AppFolio Property Manager — Handles CAM tracking natively for commercial properties. Allocates expenses by tenant share, tracks estimates vs. actuals, and generates reconciliation statements. Best for managers with 50–5,000 mixed-use units. Pairs well with QuickBooks for property management tracking if you need dual-ledger reporting.

Yardi Breeze Premier / Yardi Voyager — The industry standard for large commercial portfolios. Yardi Voyager handles complex CAM structures including base-year stops, caps with compounding, and gross-up calculations. Yardi Breeze Premier is the lighter version for mid-size operators.

MRI Software — Enterprise-level with deep CAM reconciliation modules. Handles multi-entity, multi-currency, and complex lease structures. Typically for portfolios exceeding 1M sq ft.

QuickBooks Online + Custom Templates — Some managers track CAM in QBO using class tracking and custom reports. This requires discipline and a bookkeeper who understands property management accounting. For the full comparison, see our best software for property management accounting breakdown.

Pro Tip: Whichever platform you choose, make sure it can generate a tenant-facing reconciliation statement directly — not just internal reports you have to reformat in Excel. The time you save on statement generation alone pays for the software upgrade.

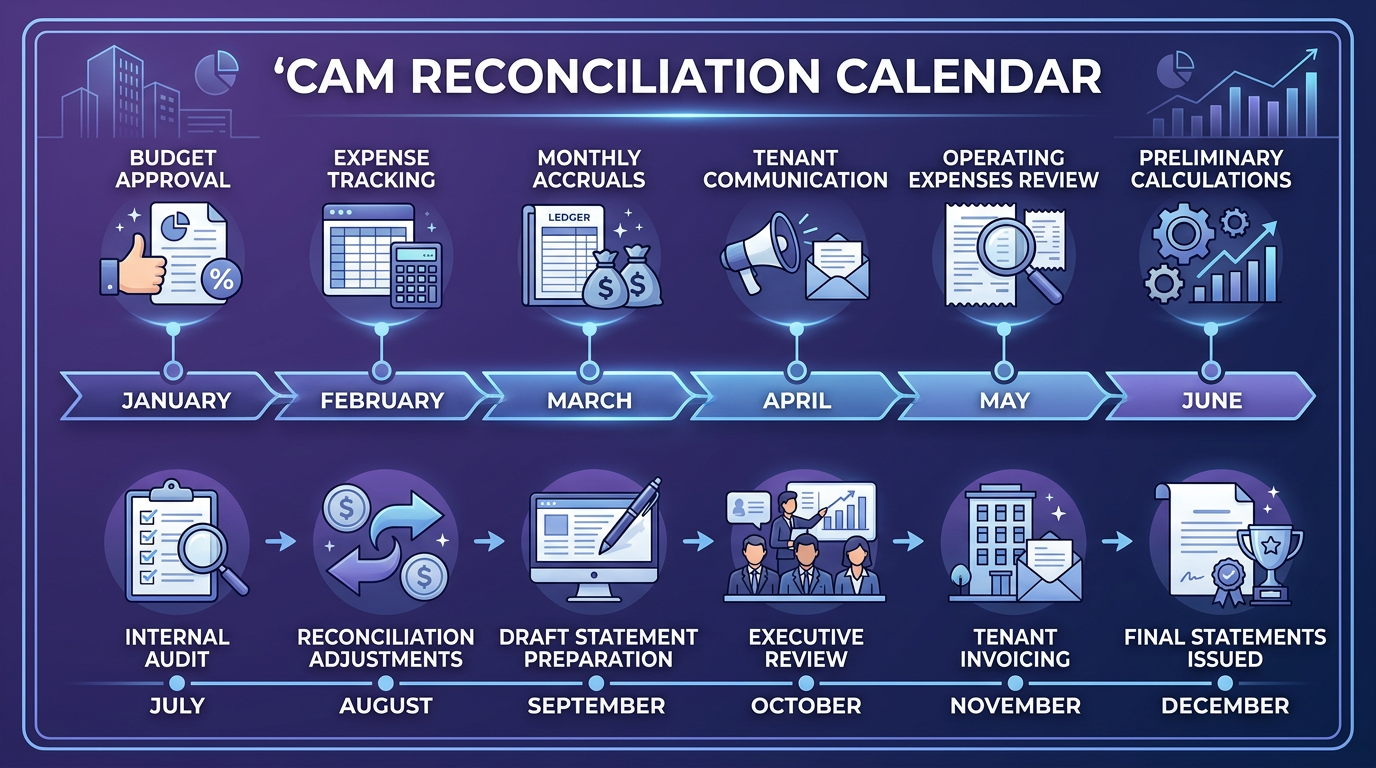

A tight reconciliation calendar is the difference between finishing on time and scrambling in May. Here’s the timeline we recommend for a December 31 fiscal year-end:

Ready to get your property management books under control? CAM reconciliation is just one piece of the puzzle. Steph’s Books provides outsourced bookkeeping built specifically for property management companies — from trust accounting to CAM tracking to owner distributions. Schedule a free consultation →

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.