Certified payroll is one of the most documentation-heavy compliance requirements that contractors face. If your electrical, plumbing, HVAC, or general contracting company has ever bid on a government project — or plans to — you need to understand exactly how certified payroll contractors are required to file, what the Davis-Bacon Act demands, and what happens when you get it wrong. The penalties aren’t theoretical. They include withheld contract payments, fines, and a three-year ban from all federal work.

This post is a cross-trade reference designed to sit alongside our industry-specific guides. If you’re an HVAC contractor, start with our complete HVAC bookkeeping guide. If you’re in plumbing, our plumbing bookkeeping guide covers the broader financial picture. What follows here is the compliance layer that applies to every trade contractor the moment a project involves federal money.

The Davis-Bacon Act requires contractors and subcontractors to pay prevailing wages on all federal construction contracts exceeding $2,000. That threshold is not a typo — virtually every federal construction contract triggers the requirement.

But the reach extends far beyond direct federal projects. Davis-Bacon and Related Acts (DBRA) extend prevailing wage requirements to federally-assisted state and local projects funded through programs like:

The practical impact: if you’re a plumber working on a municipal water treatment upgrade, an HVAC contractor installing systems in a new federal courthouse, or an electrician wiring a public school addition — Davis-Bacon applies. And if Davis-Bacon applies, certified payroll reporting is mandatory.

Key point: The requirement flows down to every subcontractor tier. If you’re a sub on a project where the prime contractor holds a Davis-Bacon contract, you file certified payroll too — regardless of your contract size.

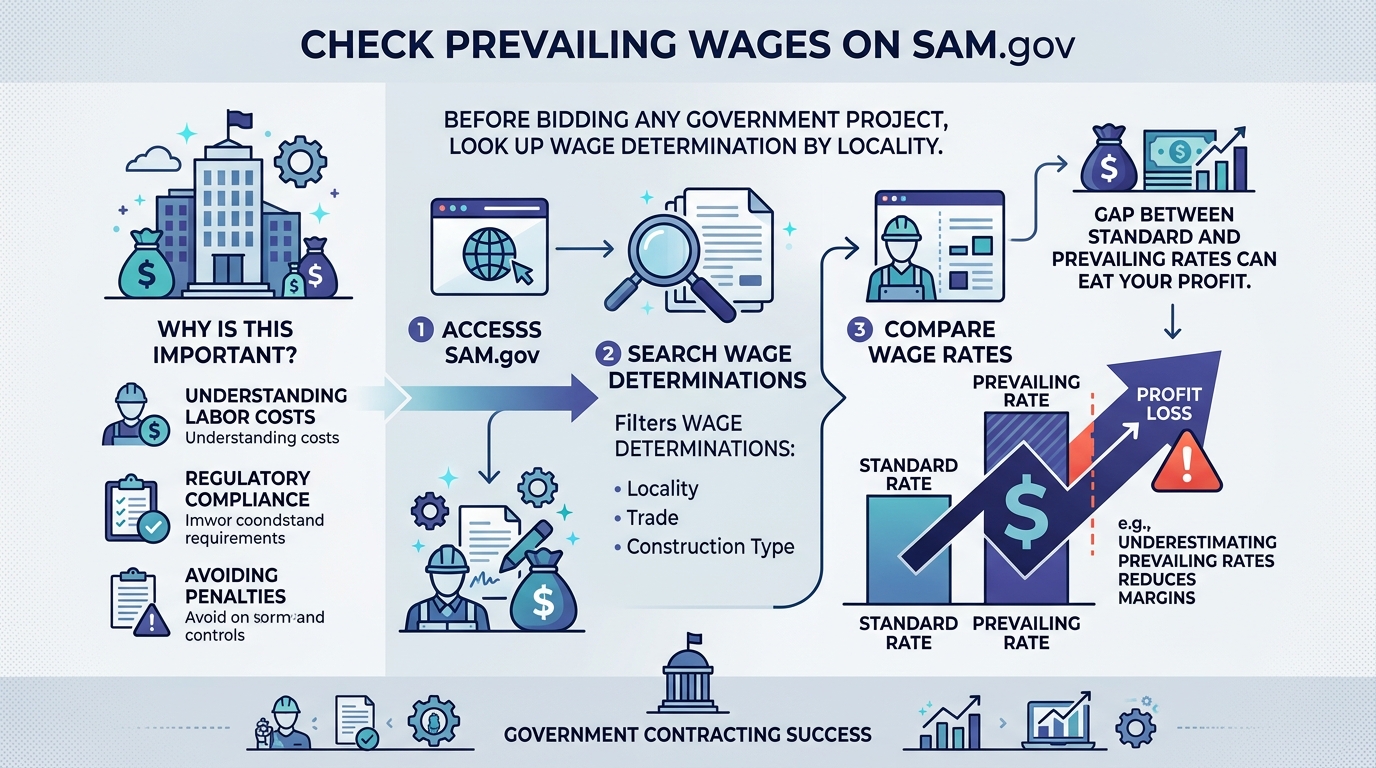

Before you bid a Davis-Bacon project, you need to know what you’re required to pay. Prevailing wage determinations are published by the Department of Labor’s Wage and Hour Division and are available on SAM.gov (System for Award Management).

Here’s how to find the rates:

Each wage determination lists trade classifications with two components:

The total prevailing wage is the sum of both. For example, a wage determination might show:

| Component | Amount |

|---|---|

| Basic hourly rate | $48.75 |

| Fringe benefits | $22.30 |

| Total prevailing wage | $71.05 |

You must pay the full prevailing wage. You can satisfy the fringe portion through cash payments (adding it to the hourly wage), through bona fide benefit plans (health insurance, pension contributions), or through a combination of both.

Important: Wage determinations are locality-specific and updated periodically. A project in Cook County, Illinois will have different prevailing wage rates than one in Springfield. Always verify the wage decision number listed in your contract matches the current determination on SAM.gov before starting work.

The gap between what you normally pay and what Davis-Bacon requires can be significant. Here’s a comparison using representative rates for common trade classifications:

| Trade Classification | Standard Market Rate | Prevailing Wage (Base + Fringe) | Difference |

|---|---|---|---|

| Electrician — Journeyman | $35-$45/hr | $65-$85/hr | +$20-$40/hr |

| Plumber — Journeyman | $32-$42/hr | $60-$80/hr | +$18-$38/hr |

| HVAC Mechanic — Journeyman | $30-$40/hr | $55-$75/hr | +$15-$35/hr |

| General Laborer | $18-$25/hr | $35-$50/hr | +$12-$25/hr |

| Carpenter — Journeyman | $28-$38/hr | $50-$70/hr | +$12-$32/hr |

| Ironworker — Structural | $35-$48/hr | $65-$90/hr | +$17-$42/hr |

| Operating Engineer — Crane | $38-$50/hr | $70-$95/hr | +$20-$45/hr |

These rate differences must be built into your bid. Contractors who estimate government projects using their standard labor rates and then discover the prevailing wage requirement after contract award face an immediate margin problem — sometimes enough to turn a profitable project into a loss.

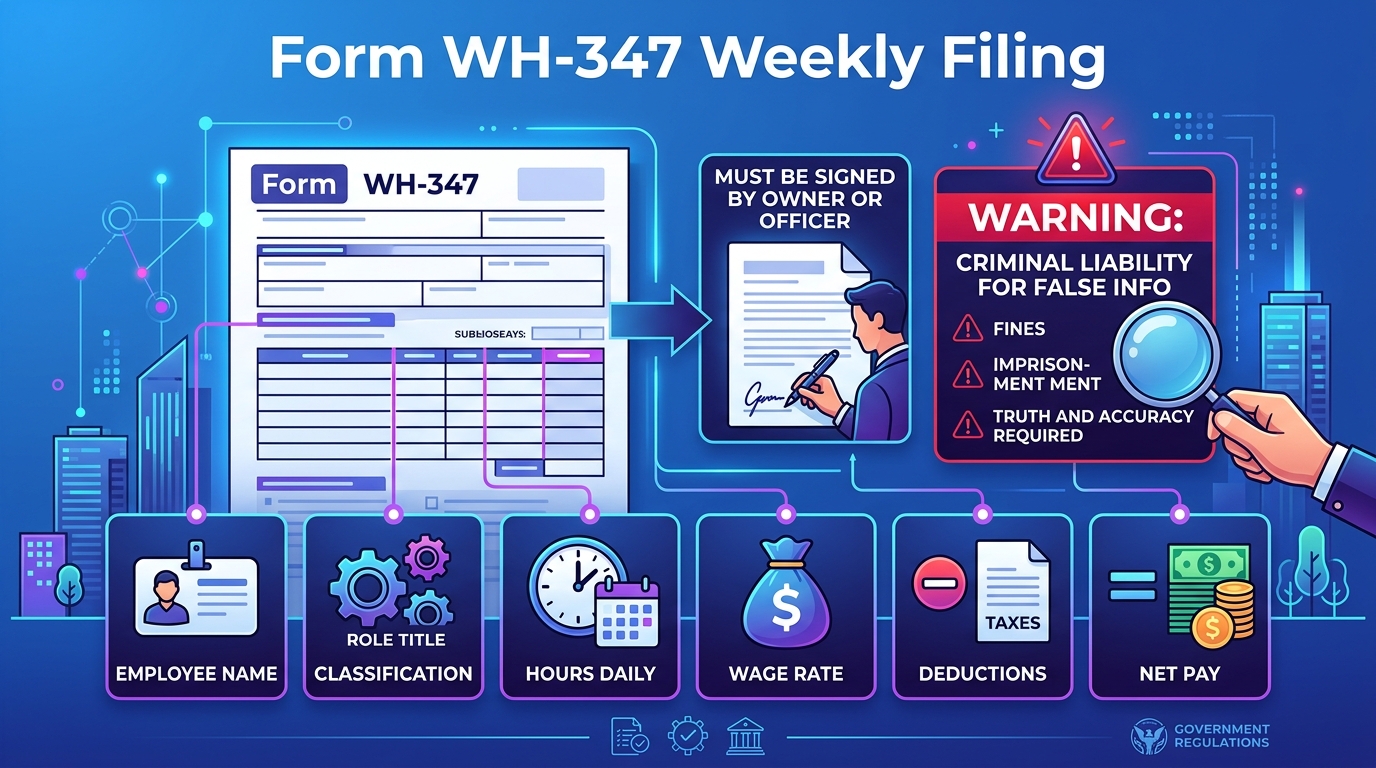

Form WH-347 is the Department of Labor’s standard certified payroll form — officially titled the Statement of Compliance. While its use is not technically mandatory (you can submit equivalent data in another format), it is the accepted standard on virtually every federal project, and most contracting officers require it.

You can download the form from the DOL Wage and Hour Division.

Certified payroll reports are filed weekly. Each report covers a seven-day workweek for every employee who performed work on the covered project during that period. Even if an employee only worked two hours on the project in a given week, that week’s certified payroll must include them.

Each weekly report requires the following for every employee:

Page 2 of Form WH-347 is the Statement of Compliance — this is the “certified” part of certified payroll. An owner, officer, or authorized agent of the company must sign it each week, attesting that:

This signature carries legal weight. Knowingly submitting a false certified payroll report is a federal crime under 18 U.S.C. Section 1001.

Davis-Bacon projects allow apprentices to be paid less than the journeyman prevailing wage — but only under strict conditions. Apprentice rates apply only to workers enrolled in a registered apprenticeship program approved by the Bureau of Apprenticeship and Training (BAT) or a state apprenticeship agency.

The apprentice-to-journeyman ratio must comply with the standards set by the applicable apprenticeship program. These ratios vary by trade and by state:

Critical compliance detail: Ratio compliance is measured daily, not as a weekly average. If you have one journeyman electrician and two electrical apprentices on site on a Tuesday, you’re in violation that day — even if you had four journeymen on site Monday and Wednesday. Daily crew sheets are essential documentation.

For every apprentice on a Davis-Bacon project, you must maintain:

If an apprentice is not properly registered, they must be paid the full journeyman prevailing wage rate — no exceptions.

The fringe benefit component of the prevailing wage creates its own documentation burden. You have two options for meeting the fringe requirement:

Pay the fringe amount directly to the employee as additional hourly compensation. If the prevailing wage determination shows $22.30/hour in fringes, you add $22.30 to each hour worked. This is the simplest approach but increases your payroll tax liability since fringe cash payments are taxable wages.

Credit contributions to qualifying benefit plans — health insurance, pension, vacation funds, apprenticeship training funds — toward the fringe obligation. You must document:

Annualization example: If you pay $850/month for an employee’s health insurance and the employee works 173 hours/month on average, the hourly credit is $4.91/hr ($850 / 173). Only the annualized hourly amount counts toward the fringe obligation — not the flat monthly cost divided by a standard 2,080 annual hours.

Most contractors use a combination of cash and benefits to meet the total fringe requirement. Whatever mix you choose, the documentation must show that the total hourly value of cash payments plus benefit contributions meets or exceeds the fringe rate in the wage determination.

Pro tip: Fringe benefit calculations should be reviewed monthly. Employee benefit costs change (premium renewals, new hires on the plan), and the annualized hourly credit shifts with actual hours worked. A quarterly review is not frequent enough — a discrepancy that runs three months creates a back-pay liability that’s far harder to correct.

Davis-Bacon requires contractors to retain all payroll records for a minimum of three years after the project is completed. In practice, keep them for at least five years — many state prevailing wage laws have longer retention periods, and DOL investigations can be initiated years after project completion.

Records must be accessible on demand to Department of Labor Wage and Hour Division investigators. “On demand” means within a reasonable timeframe — not “we’ll get back to you in three weeks.” Required records include:

Digital records are acceptable as long as they’re organized, complete, and can be produced in a readable format. A shoebox of paper timesheets from a 2024 project will not satisfy an investigator in 2027.

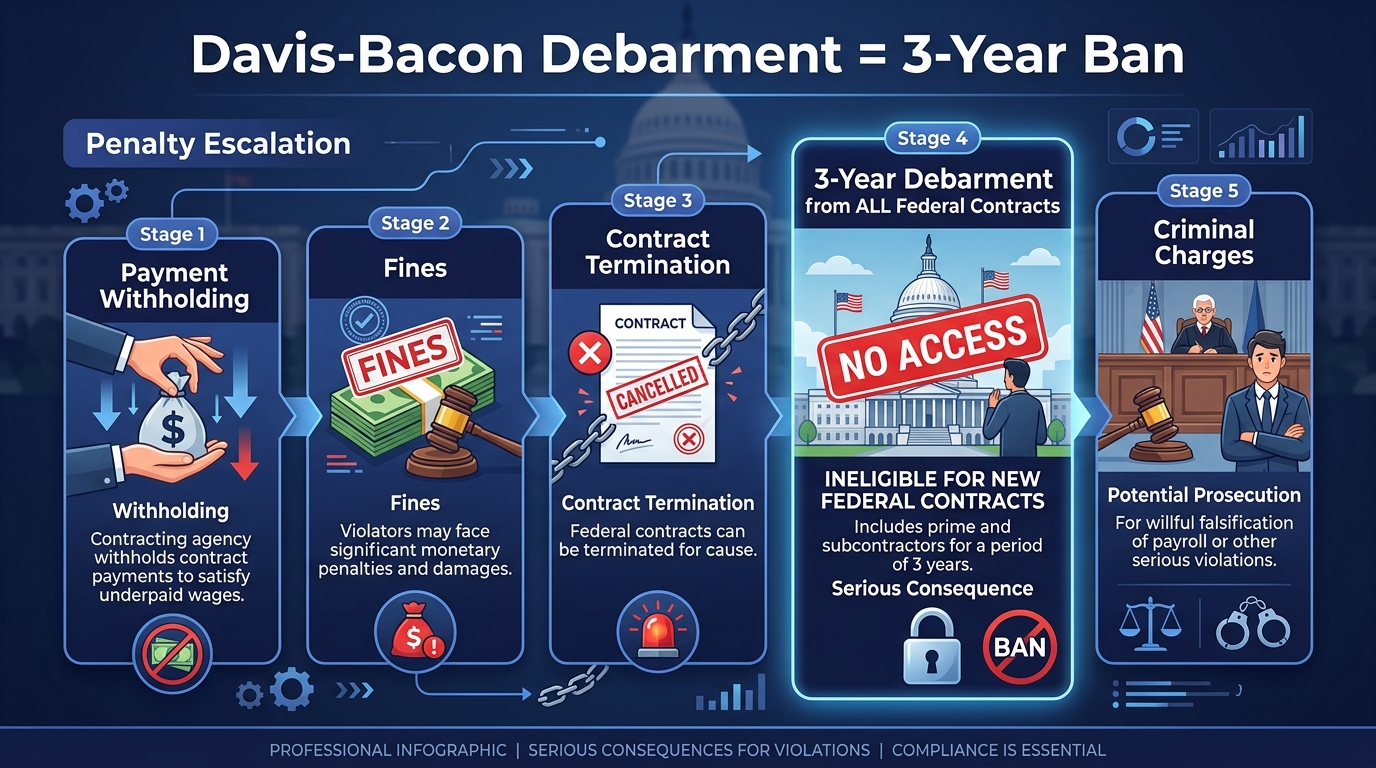

The enforcement framework for Davis-Bacon violations is structured to escalate:

Withholding of contract payments. The contracting agency can withhold funds from progress payments to cover back wages owed to underpaid workers. This hits your cash flow immediately.

Back wages. You must pay the difference between what was paid and what was required — including fringe benefits — for every hour of non-compliant work, plus interest.

Civil penalties. Fines of up to $2,325 per violation (adjusted for inflation) for each affected worker.

Contract termination. The agency can terminate the contract for cause, making you liable for excess costs of re-procurement.

Debarment. The most severe administrative penalty: a three-year ban from all federal and federally-assisted contracts. For a contractor whose pipeline includes government work, debarment is existential.

Criminal penalties. Knowingly falsifying a certified payroll report is a federal crime punishable by fines and imprisonment. This isn’t a theoretical risk — DOL refers cases to the Department of Justice.

This is where the compliance requirement becomes a bookkeeping problem. Certified payroll doesn’t just add paperwork — it changes the structure of how you track labor costs, allocate overhead, and calculate project profitability.

Every Davis-Bacon project requires its own payroll tracking. If an employee works on a prevailing wage project Monday through Wednesday and a private project Thursday and Friday, you need separate wage records for each — at different rates. Your bookkeeping system must support project-level payroll allocation, not just company-wide payroll runs.

Many contractors pay employees their standard rate on private work and the prevailing wage rate on Davis-Bacon projects. Your payroll system needs to handle multiple pay rates per employee per pay period, with the correct rate applied to the correct project hours. Flat-rate payroll software won’t cut it.

If you’re crediting benefits toward the fringe obligation, those benefit costs must be allocated to the specific project — not spread across all jobs as general overhead. This changes your job costing and your overhead rate calculations.

Higher prevailing wage labor costs increase your project-level COGS. If you’re using a markup-on-cost pricing model, the higher labor base inflates your bid price. If you’re using a fixed-price bid, the higher labor costs compress your margin. Either way, your bookkeeper needs to understand that prevailing wage projects have fundamentally different cost structures than private work.

While Davis-Bacon applies to all construction trades, some encounter it more frequently than others:

Use payroll software with certified payroll support. Systems like Foundation Software, Sage 300 CRE, and Viewpoint Vista can generate WH-347 reports directly from payroll data. Manual preparation is error-prone and time-consuming at scale.

Maintain separate job codes for every Davis-Bacon project. Your QuickBooks or accounting software should have a unique job code for each prevailing wage project so labor costs, fringe allocations, and overhead are tracked independently.

Track fringe benefits monthly. Recalculate annualized hourly fringe credits each month based on actual hours worked and current benefit costs. Don’t use static annual estimates.

Build a certified payroll calendar. Weekly filing deadlines stack up fast when you’re running multiple prevailing wage projects simultaneously. A missed filing is a red flag to investigators.

Keep daily crew logs. Apprentice ratio compliance is measured daily. A simple spreadsheet showing which employees were on site each day, their classifications, and the journeyman-to-apprentice count protects you during audits.

Brief your project managers. PMs need to understand that worker classifications on certified payroll must match the work actually performed. If a journeyman plumber spends a day doing laborer tasks, the wage determination for the classification of work performed applies — which may actually be lower, but misclassification in either direction is a violation.

Need help with certified payroll bookkeeping? Steph’s Books works with trade contractors who run prevailing wage projects. We handle the project-level payroll tracking, fringe benefit allocation, and job costing that Davis-Bacon compliance demands. Get an instant quote or schedule a free consultation to see what specialized contractor bookkeeping looks like.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.