A 200-unit property management company that misclassifies security deposits as revenue will overstate income by $120,000–$180,000 in a single year. When the state auditor catches it — and they will — the fines start at $10,000 per violation, plus potential license revocation.

That’s not a bookkeeping error. That’s an existential business risk hiding in your general ledger.

Property management accounting is fundamentally different from every other industry we serve. You’re handling other people’s money across multiple legal entities, juggling trust account regulations that vary by state, and producing financial reports for owners who treat your monthly statement like a report card. Get it wrong, and you lose clients. Get it very wrong, and you lose your license.

This guide covers every financial operations challenge unique to property management — from CAM reconciliation and owner distributions to security deposit compliance and chart of accounts design. If you’re managing 50+ units and generating $1M–$10M in revenue, this is the playbook your accounting function needs.

Most accounting follows a straightforward pattern: revenue comes in, expenses go out, you report the difference. Property management accounting breaks every one of those assumptions.

Every dollar of tenant rent, security deposit, and owner reserve sits in a trust account — money you hold but don’t own. Commingling trust funds with operating funds is illegal in all 50 states, and it’s the single fastest way to lose your property management license.

The compliance requirements are specific. Most states require:

Miss a reconciliation deadline, and state real estate commissions can audit your entire operation. The National Association of Residential Property Managers (NARPM) publishes best practice guides, but compliance ultimately falls on your accounting team.

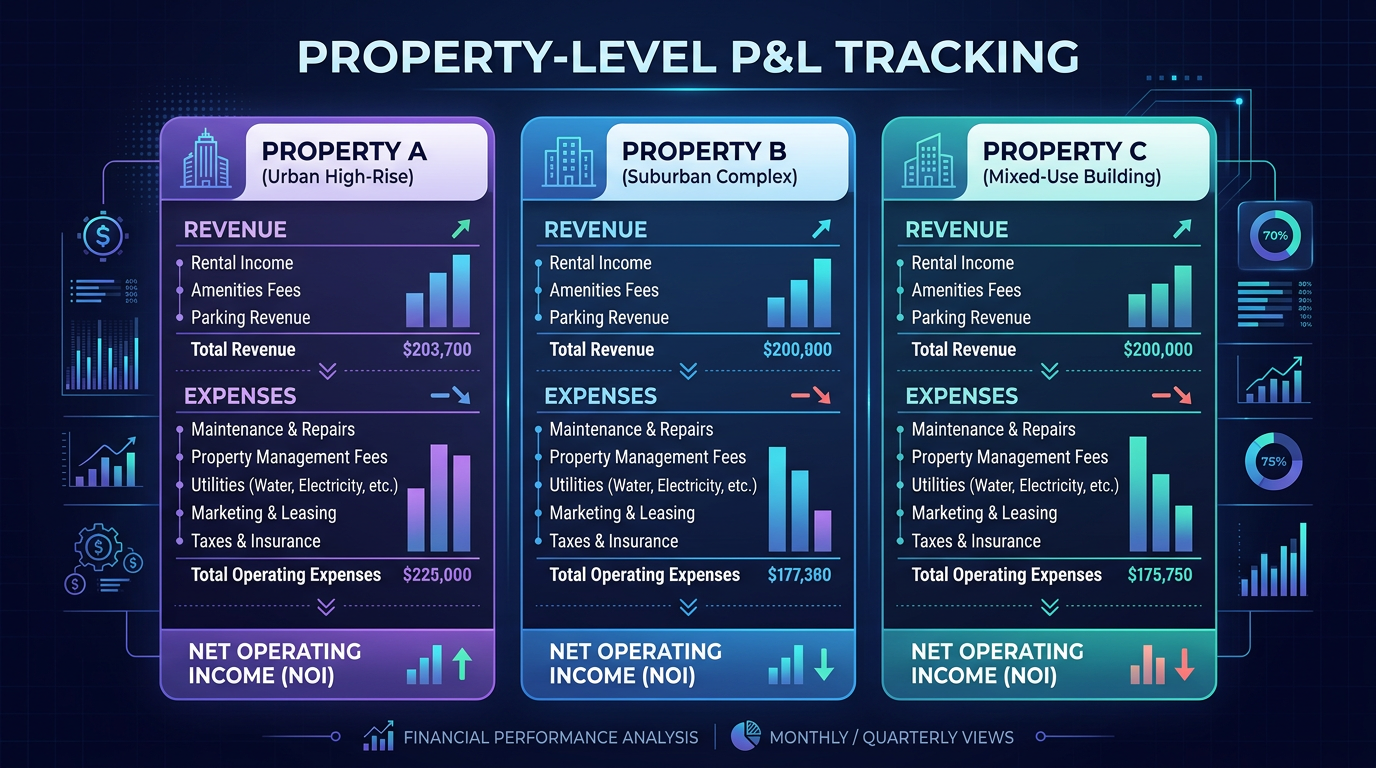

A 150-unit portfolio across 12 properties isn’t one business — it’s 12 separate P&Ls that roll up into one. Every income and expense line must track to a specific property, and often to a specific unit within that property.

Your chart of accounts needs three dimensions:

In QuickBooks Online, that means using Location tracking for properties and Class tracking for property type. In AppFolio or Buildium, property-level tracking is native. Either way, every single transaction needs a property tag — no exceptions.

Your owners aren’t passive investors. They’re checking your monthly statements against their own expectations, comparing your management fees to competitors, and questioning every maintenance charge over $500.

The standard owner report package includes:

If your accounting system can’t generate these reports automatically, your staff is spending 4–8 hours per property per month building them manually. At 50 properties, that’s a full-time employee doing nothing but owner reports.

Property management companies operating across state lines face overlapping regulations. Trust account rules in Illinois differ from Indiana. Security deposit interest requirements in Connecticut don’t apply in Texas. Late fee caps vary by municipality.

Your accounting system must handle:

This regulatory patchwork is why generic bookkeepers fail in property management. You need someone who understands the state real estate commission requirements for every jurisdiction you operate in.

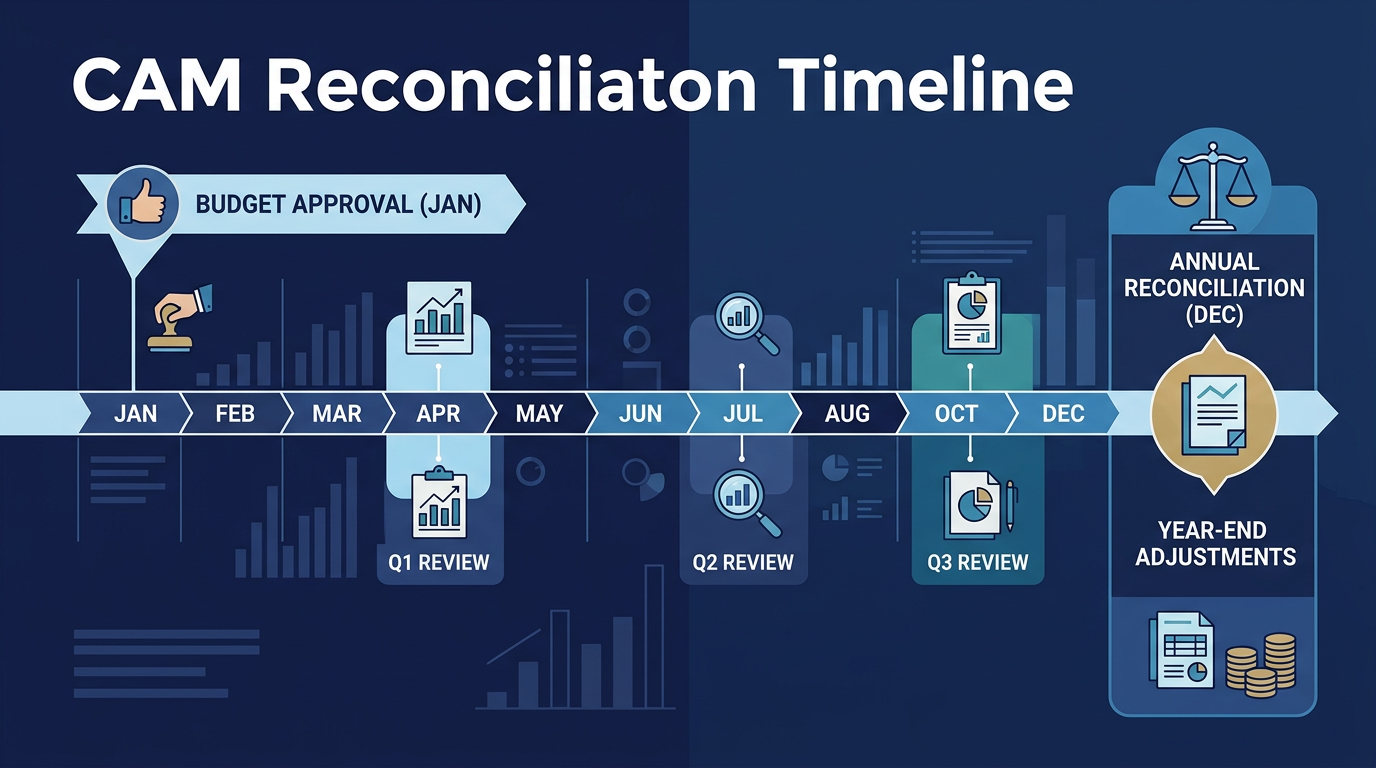

If you manage commercial properties, Common Area Maintenance (CAM) reconciliation is the most labor-intensive accounting task on your calendar. Get it right, and tenants trust your numbers. Get it wrong, and you’re fielding disputes for months.

CAM charges cover shared expenses — parking lot maintenance, landscaping, snow removal, elevator service, lobby cleaning, shared utilities, property insurance, and property taxes. Commercial leases typically require tenants to pay their proportionate share based on square footage.

Here’s the math that matters: if a tenant leases 3,000 square feet in a 30,000 square foot building, their pro rata share is 10%. If total CAM expenses for the year are $180,000, that tenant owes $18,000. Throughout the year, they’ve been paying estimated monthly CAM charges of $1,500/month ($18,000/12). At year-end, you reconcile actual expenses against estimates and issue a credit or bill the difference.

The reconciliation statement must include:

These mistakes trigger tenant disputes every year:

Pro Tip: Start your CAM reconciliation in November, not January. Pull preliminary numbers, identify any expense categories that look off, and resolve discrepancies before year-end closes. This turns a 6-week scramble into a 2-week process. For a detailed walkthrough, see our CAM reconciliation guide.

Step 1: Pull actual expense reports by property. Every expense tagged to the property’s CAM cost pool for the calendar year.

Step 2: Review lease exclusions. Each tenant’s lease may exclude different expense categories. Tenant A’s lease excludes management fees from CAM; Tenant B’s includes them. You need a lease abstract for every tenant.

Step 3: Calculate pro rata shares. Use the rentable square footage as of January 1 (or the lease-specified measurement date). Verify against the latest space plan.

Step 4: Generate reconciliation statements. Show each expense category, the tenant’s share, payments made, and the net adjustment.

Step 5: Distribute statements with backup documentation. Tenants will ask for invoices. Have them ready.

A 100,000 square foot commercial property with 15 tenants typically takes 20–30 hours to reconcile fully. At a blended staff cost of $45/hour, that’s $900–$1,350 per property per year just for CAM reconciliation.

Property-level financial tracking is the foundation of everything else — owner reports, tax filings, portfolio performance analysis, and acquisition/disposition decisions all depend on accurate property-level data.

Your chart of accounts needs to support three levels of reporting: individual property, portfolio roll-up, and management company.

Income accounts should separate:

Expense accounts should separate:

In QBO, the most effective setup uses Locations for properties and Classes for property types. This gives you two independent dimensions for slicing data.

Every transaction gets both tags. No exceptions. If a transaction doesn’t have a property tag, it’s invisible in your owner reports and your property P&L is understated.

Important: QBO’s Location tracking is available on Plus and Advanced plans only ($99+/month). If you’re on Simple Start or Essentials, you can’t track by property natively — you’ll need to use sub-accounts instead, which creates a bloated chart of accounts. For most PM companies, the QBO Advanced plan ($235/month) pays for itself in reporting capability alone. See our QuickBooks property management tracking guide for setup instructions.

Larger PM operations often hold properties in separate LLCs for liability protection. This creates a multi-entity accounting challenge: each LLC needs its own books, its own bank accounts, and its own tax filings — but you need consolidated reporting for the management company.

Common structure:

In QBO, you handle this with separate QBO files per entity, or with QBO Advanced’s multi-entity consolidation feature. AppFolio and Yardi handle multi-entity natively.

The intercompany transactions add complexity: management fees flow from Property LLCs to the Management Company LLC. These must be recorded on both sides — expense in the property entity, revenue in the management entity — and eliminated in any consolidated reporting.

Trust accounting is the part that has to be right

Owner distributions, security deposits, and per-property P&Ls, reconciled monthly and ready for the annual review.

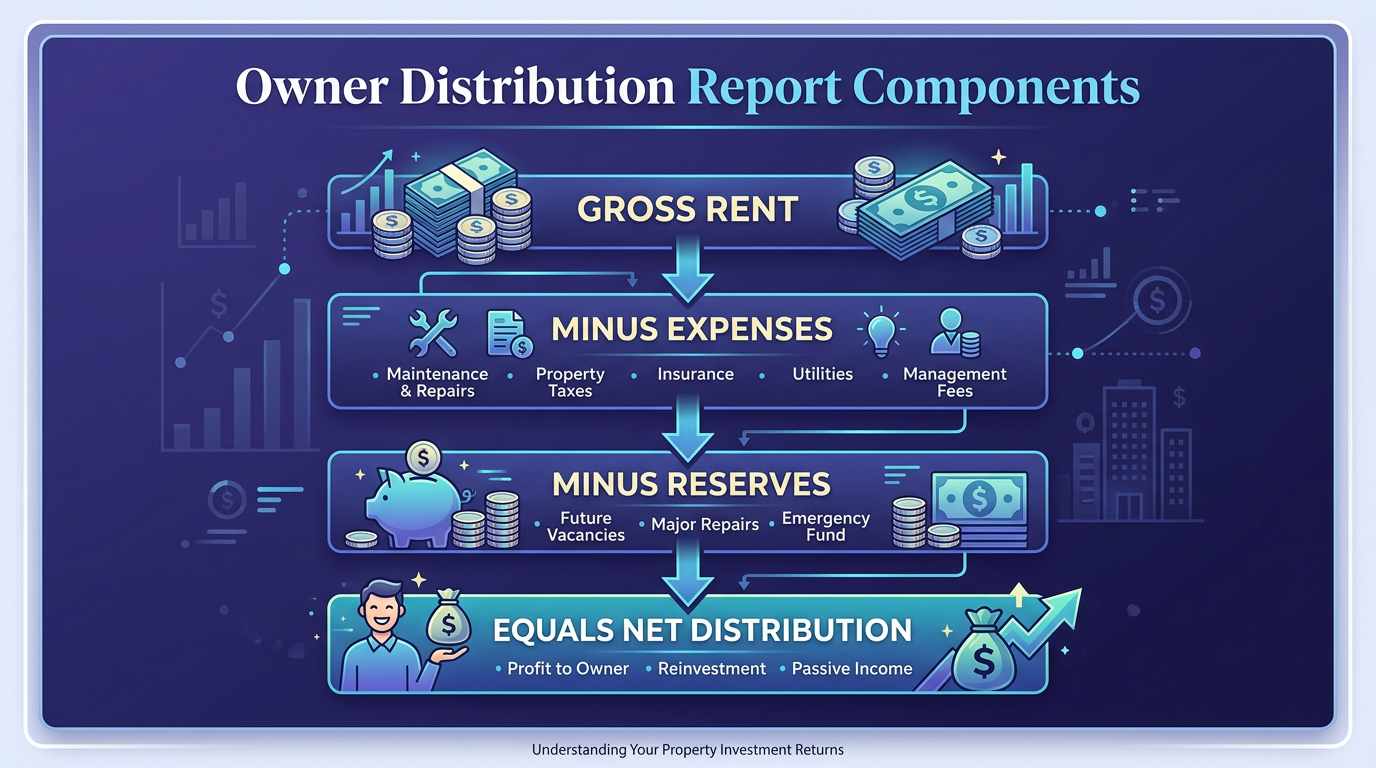

Get an instant quoteTalk to us firstOwner distributions are the moment of truth in property management accounting. The monthly (or quarterly) distribution report is how property owners evaluate your performance — and decide whether to renew your management agreement.

Every owner wants to answer three questions:

That third question is where most PM companies lose trust. The gap between net operating income and the actual distribution includes management fees, reserve contributions, pending repairs, and insurance deductions. If your report doesn’t explain every dollar of that gap, owners fill the void with suspicion.

A professional owner distribution package includes:

| Report Component | Purpose | Frequency |

|---|---|---|

| Income Statement (P&L) | Shows rental income minus all expenses | Monthly |

| Cash Flow Statement | Explains money in, money out, ending balance | Monthly |

| Distribution Summary | Net amount being wired/ACH’d to owner | Monthly |

| Reserve Balance | Current reserve fund amount and recent activity | Monthly |

| Rent Roll | Unit-by-unit occupancy, lease terms, rent amounts | Monthly |

| Maintenance Detail | Every work order with cost and vendor | Monthly |

| Budget vs. Actual | Year-to-date performance against annual budget | Quarterly |

| Capital Expenditure Summary | Major improvements completed or planned | Quarterly |

| 1099 Package | Year-end tax reporting for distributions | Annually |

Standard distribution timing is the 15th of the following month. January rents collected → distributed by February 15th. This gives you time to clear pending charges, confirm all deposits have settled, and run your reconciliation.

Reserve withholding is critical. Most management agreements authorize holding back 5–10% of gross rents as an operating reserve. On a property generating $20,000/month in rent, that’s $1,000–$2,000 held back per month. Owners accept this when it’s disclosed upfront; they revolt when it shows up as a surprise deduction.

Pro Tip: Set a reserve cap in your management agreement — typically 1–2 months of operating expenses. Once the reserve reaches the cap, excess funds flow through to the owner. This prevents the reserve from growing indefinitely and triggering owner complaints. For detailed templates and best practices, see our owner distribution reports guide.

Here’s the actual math for a 20-unit residential property:

Gross Rent Collected: $32,000

Minus Operating Expenses:

– Maintenance/repairs: ($2,400)

– Utilities (common area): ($1,200)

– Insurance: ($950)

– Property taxes: ($2,800)

– Landscaping: ($600)

– Management fee (8%): ($2,560)

Net Operating Income: $21,490

Minus Reserve Contribution (5%): ($1,600)

Minus Pending Invoice (HVAC repair): ($1,850)

Owner Distribution: $18,040

Every line in that calculation must appear on the distribution report. If the owner sees $32,000 in rent and a $18,040 check, they need to trace every dollar of the $13,960 difference.

Security deposits are the single highest-risk accounting item in property management. They’re not your money, they’re subject to state-specific regulations, and mishandling them triggers lawsuits faster than any other accounting error.

Security deposits are liabilities, not income. They sit on your balance sheet as a liability until the tenant moves out and you either return the deposit or apply it against damages. Recording a security deposit as revenue is not just wrong — in most states, it’s a violation of trust accounting law.

Security deposit rules vary dramatically across states. Here are the key variables:

Critical: If you manage properties across state lines, you need a compliance matrix mapping every property to its jurisdiction’s deposit rules. A deposit returned on day 31 in a state with a 30-day deadline can result in forfeiture of the right to claim damages — plus statutory penalties of 2x or 3x the deposit amount. See our security deposit accounting guide for state-by-state requirements.

Most states require security deposits to be held in one of two ways:

The pooled trust approach is standard for PM companies managing 50+ units. The key requirement: your subsidiary ledger must reconcile to the bank balance every month. If you’re holding $340,000 in security deposits across 200 units, your trust account bank statement must show at least $340,000. Any shortfall means you’ve commingled funds — an immediate compliance violation.

In states requiring interest on deposits (Illinois requires it for buildings with 25+ units, for example), you must:

The accounting for interest-bearing deposits adds a layer of complexity. Interest accrues monthly, gets allocated across tenants based on deposit amounts and holding periods, and must be reported to tenants. Most PM-specific software handles this natively. In QBO, you’ll need a custom tracking system.

When a tenant moves out, the security deposit accounting process is:

The journal entry for a $2,000 deposit with $650 in damages:

That $650 in retained deposit is revenue — but only at move-out, not at move-in. This timing distinction is where most accounting errors occur.

A well-designed chart of accounts is the difference between a PM company that generates accurate reports in minutes and one that spends days manually adjusting Excel exports.

Your chart of accounts should follow this hierarchy:

| Account Number Range | Category | Examples |

|---|---|---|

| 1000–1999 | Assets | Operating cash, trust cash, security deposit accounts, prepaid insurance, fixed assets |

| 2000–2999 | Liabilities | Security deposits held, owner reserves, accrued expenses, loans payable |

| 3000–3999 | Equity | Owner’s equity, retained earnings |

| 4000–4499 | Rental Income | Rent, late fees, pet rent, parking, laundry, application fees |

| 4500–4999 | Other Income | Management fees earned, CAM reimbursements, interest income |

| 5000–5999 | Property Expenses | Repairs, utilities, insurance, taxes, landscaping, HOA fees |

| 6000–6999 | Management Company Expenses | Staff salaries, office rent, software, marketing, insurance, legal |

| 7000–7999 | Capital Expenditures | Roof replacement, HVAC systems, parking lot resurfacing |

This distinction is critical and most PM companies get it wrong.

Property-level accounts (4000–5999) track income and expenses that belong to individual properties — and ultimately to the property owners. These accounts always have a Location tag in QBO.

Company-level accounts (6000–6999) track income and expenses that belong to the management company itself. Your staff salaries, office lease, software subscriptions, and marketing costs are company-level. These do not get a property Location tag.

When you blend property-level and company-level expenses in the same account ranges, your owner reports include expenses that aren’t theirs, and your management company P&L is missing costs that are.

Mistake 1: One “Repairs” account for everything. A $200 faucet replacement and a $15,000 roof repair should not land in the same account. Separate maintenance (routine repairs under $2,500) from capital improvements (major repairs that extend the asset’s useful life). The IRS treats these differently for depreciation purposes.

Mistake 2: No sub-accounts for utility types. “Utilities” as a single line item tells the owner nothing. Break it into water/sewer, electric, gas, and trash. When water costs spike 40% in July, the owner wants to know it’s water specifically — not a vague “utilities went up.”

Mistake 3: Mixing management fee income with rental income. Your management fee is earned income for the management company. Rent is pass-through income that belongs to the owner. If these hit the same income account, your management company revenue is overstated by the full rent amount.

Mistake 4: No reserve tracking accounts. Owner reserves need a dedicated liability account (2500 – Owner Reserves Held) and a corresponding asset account (1500 – Reserve Cash). When you commingle reserves with operating funds, you can’t prove the reserve exists.

For a complete template with QBO import instructions, see our property management chart of accounts guide.

Pro Tip: Export your current chart of accounts to CSV and audit it against this template. Most PM companies have 30–50% more accounts than they need (duplicates, obsolete accounts, one-off categories created years ago). A clean chart of accounts with 60–80 accounts beats a bloated one with 200+. Fewer accounts means fewer categorization errors and faster month-end closes.

Your accounting software choice determines whether month-end close takes 3 days or 3 hours. The right stack depends on your portfolio size, property types, and whether you need integrated PM operations or standalone accounting.

50–150 units: Buildium ($62–$375/month) handles accounting, tenant portals, maintenance tracking, and owner reporting in one platform. Trust accounting is native. QBO integration available if your bookkeeper requires it.

150–500 units: AppFolio ($1.49/unit/month, minimum $280/month) scales better for larger portfolios. Automated owner statements, built-in CAM reconciliation, and bank-grade trust accounting. The reporting engine is significantly more powerful than Buildium’s at this scale.

500+ units: Yardi Breeze Premier ($3/unit/month) or full Yardi Voyager for enterprise operations. Multi-entity support, commercial and residential in one system, and institutional-grade reporting for investor clients.

Any size, accounting-only: QuickBooks Online Advanced ($235/month) with Location and Class tracking enabled. Pair with any PM platform via integration or manual journal entries. Best when your accounting team is QBO-native and doesn’t want to learn a new system.

For a detailed comparison of every platform with pricing, features, and trust accounting capabilities, see our best software for property management accounting guide.

The most common setup for mid-size PM companies (100–300 units) is a PM platform as the system of record with a one-way sync to QBO for tax preparation and CPA access.

How data flows:

The critical limitation: PM-to-QBO integrations push summary journal entries, not line-item detail. Your QBO file will show “January Rent Income — Riverside Apartments: $45,000” as a single entry, not 30 individual tenant payments. Detailed transaction history stays in the PM platform.

This is fine for tax prep and high-level reporting. It’s not fine if your CPA needs to audit individual tenant accounts — they’ll need PM platform access for that.

There’s a specific inflection point where every PM company faces the same decision: keep doing accounting in-house with overloaded staff, or bring in a specialized bookkeeping partner.

You’re past the tipping point if any three of these are true:

| Factor | In-House Bookkeeper | Outsourced PM Bookkeeping |

|---|---|---|

| Monthly Cost (100 units) | $4,500–$6,000 (salary + benefits) | $1,500–$3,000 |

| Monthly Cost (250 units) | $6,000–$8,500 (may need 1.5 FTE) | $3,000–$5,000 |

| Monthly Cost (500 units) | $12,000–$16,000 (2+ FTE) | $5,000–$8,000 |

| Trust Account Expertise | Varies — requires training | Built-in (if PM-specialized) |

| Software Proficiency | Single platform typically | Multi-platform experience |

| Backup Coverage | None (PTO = backlog) | Team-based, always covered |

| Scalability | Step-function (hire in increments) | Linear (scales with portfolio) |

| Year-End/Tax Season | Overtime or missed deadlines | Staffed for peak periods |

| Turnover Risk | High (average tenure 2.3 years) | Provider’s problem, not yours |

The math at 200 units: An in-house bookkeeper costs $5,500/month fully loaded. An outsourced team costs $2,500–$4,000/month. That’s $18,000–$36,000/year in savings — enough to fund a part-time leasing agent who actually generates revenue.

Non-negotiable requirements:

Red flags:

The right outsourced bookkeeping partner for property management isn’t a generalist firm that “also does property management.” It’s a firm that understands the regulatory landscape, speaks your language, and has PM-specific workflows built into their process. For more on evaluating outsourced options, see our complete outsourced bookkeeping guide.

Your accounting system should produce these metrics automatically — if it can’t, your chart of accounts or reporting setup needs work.

Ready to clean up your property management accounting? Steph’s Books specializes in bookkeeping for property management companies managing 50–500+ units. Trust account reconciliation, owner distributions, CAM reconciliation, and 1099 preparation — all handled by a team that understands property management inside out. Get started with a free consultation.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.