Section 179 allows contractors to deduct the full purchase price of qualifying equipment — up to $1,250,000 in 2026 — in the year it’s placed in service, instead of depreciating it over multiple years. This includes trucks, heavy equipment, tools, and software.

Every trade contractor buys equipment — trucks, excavators, drain cameras, mowers, diagnostic tools. The question isn’t whether you’re spending money on assets. The question is whether you’re deducting that spending in the most tax-efficient way possible. Section 179 contractors who understand the rules can write off hundreds of thousands of dollars in equipment purchases in the year of acquisition instead of spreading those deductions across five to seven years. The contractors who don’t understand these rules overpay their taxes by thousands every single year.

This guide covers Section 179, bonus depreciation, MACRS schedules, the de minimis safe harbor, and buy vs. lease decisions for trade contractors across HVAC, plumbing, electrical, general contracting, and landscaping. See our guides to HVAC bookkeeping and plumbing bookkeeping for industry-specific financial management. Whether you are buying a single work truck or outfitting an entire fleet, the depreciation strategy you choose determines how much cash stays in your business this year versus five years from now.

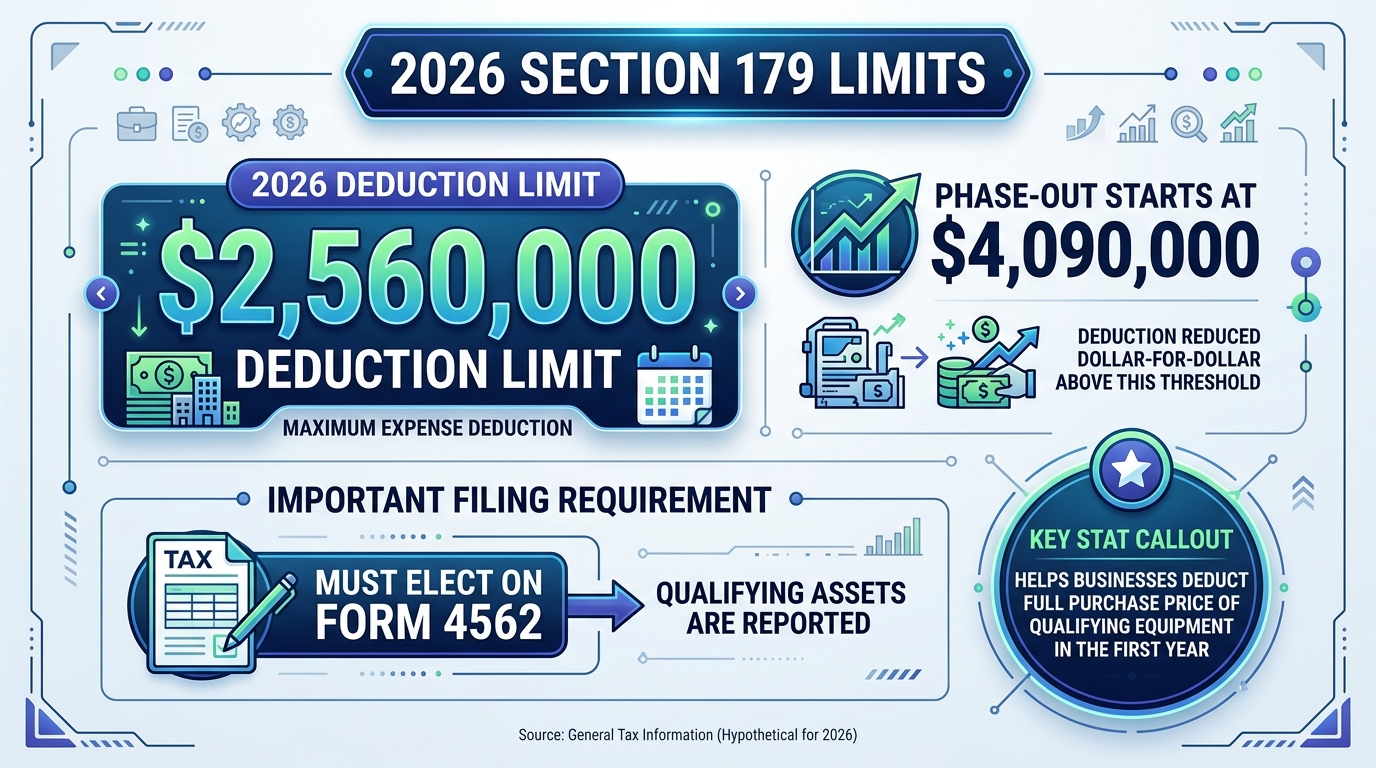

The Section 179 deduction lets you expense the full cost of qualifying equipment in the year it is placed in service — rather than capitalizing it and depreciating it over the asset’s useful life. For 2026, the numbers are:

For most trade contractors doing $1M to $10M in revenue, the $2,560,000 limit is more than sufficient. Even a contractor replacing an entire fleet of trucks and buying major excavation equipment in a single year will rarely hit the cap. The real value of Section 179 is in the first-year cash flow impact — deducting a $55,000 truck immediately instead of taking $11,000 per year over five years.

You buy a qualifying asset. You place it in service (meaning it’s ready and available for use in your business — not sitting in a dealer lot). You elect Section 179 treatment on IRS Form 4562 when you file your tax return. The full cost hits your P&L as a deduction in the year of purchase.

The election is not automatic. If your CPA files your return without making the Section 179 election, you default to standard MACRS depreciation — and you cannot go back and amend to claim Section 179 retroactively for most asset classes. This is the single most common mistake we see with Section 179 contractors who buy expensive equipment but never coordinate the election with their tax preparer.

The vehicle weight threshold is the most consequential — and most misunderstood — rule in Section 179 for contractors. It determines whether you deduct the full purchase price of a truck in year one or get stuck with luxury vehicle depreciation limits that cap your first-year write-off at a fraction of the cost.

Vehicles over 6,000 lbs GVWR qualify for the full Section 179 deduction with no luxury automobile cap. Buy a $55,000 Ford F-250 that weighs 6,500 lbs and you deduct the entire $55,000 in the year of purchase.

Vehicles under 6,000 lbs GVWR are subject to the luxury automobile depreciation limits under IRC Section 280F. For 2026, those limits cap your first-year deduction at approximately $12,400 without bonus depreciation or $20,400 with bonus depreciation. On that same $55,000 vehicle, you would wait four to six years to fully recover the cost.

That is a $34,600 difference in year-one deduction — solely based on whether the truck clears the 6,000-pound threshold.

Most full-size work trucks and cargo vans used by HVAC contractors, plumbing contractors, and general contractors exceed 6,000 lbs GVWR:

Compact cargo vans, small pickups, and light-duty work vehicles often fall under the threshold:

The rule of thumb: Check the GVWR on the driver’s side door jamb sticker before you sign any purchase order. Don’t rely on the dealer’s estimate. A few hundred pounds can mean a $30,000 swing in your first-year tax deduction.

After declining from 100% in 2022 to 80% in 2023, 60% in 2024, and 40% in 2025, 100% bonus depreciation was fully restored by the One Big Beautiful Bill Act (OBBBA) for assets placed in service after January 19, 2025. This is a major development for contractors making significant capital purchases in 2026.

Bonus depreciation applies to both new and used equipment — as long as the asset is new to your business (you haven’t used it before). It works alongside Section 179 and has no dollar cap, unlike Section 179’s $2,560,000 limit. If your total qualifying purchases exceed the Section 179 threshold, bonus depreciation picks up the remainder.

For most contractors, Section 179 and bonus depreciation produce the same result: a full first-year deduction. The strategic difference matters in three scenarios:

See IRS Publication 946 for full depreciation rules, asset class definitions, and recovery period tables.

Pro Tip: If you’re choosing between Section 179 and bonus depreciation for the same asset, the practical difference is usually about state taxes and NOL planning. Talk to your CPA — but make sure your bookkeeper has flagged the purchase, the placed-in-service date, and the GVWR (for vehicles) before that conversation happens.

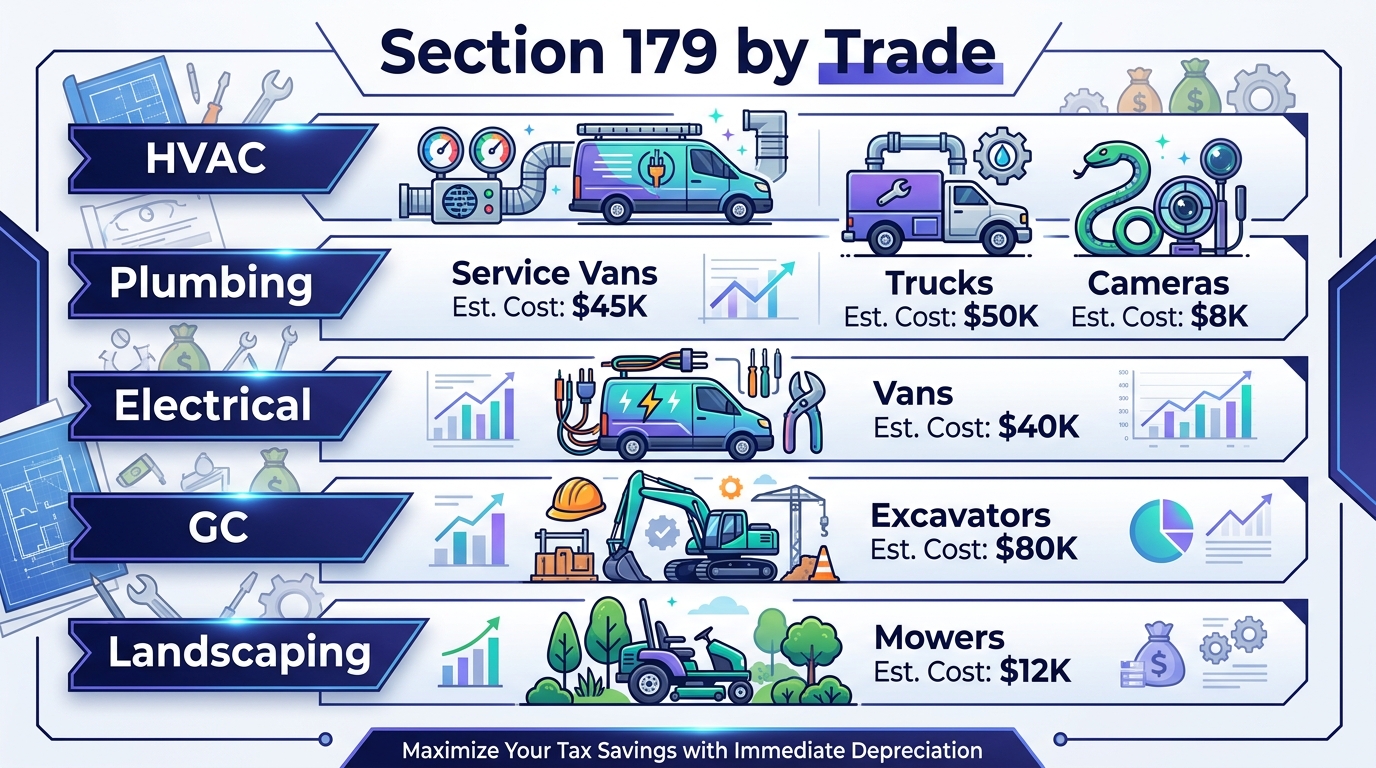

Every trade has its own equipment mix. The table below shows common qualifying assets, typical purchase costs, and the depreciation treatment under Section 179 versus MACRS:

| Trade | Equipment | Typical Cost | Section 179 Eligible? | MACRS Recovery Period |

|---|---|---|---|---|

| HVAC | Service vans (over 6,000 lbs) | $45,000 | Yes — full deduction | 5 years |

| HVAC | Refrigerant recovery machines | $3,000 | Yes — full deduction | 7 years |

| HVAC | Diagnostic equipment (analyzers, gauges) | $5,000 | Yes — full deduction | 7 years |

| Plumbing | Work trucks (over 6,000 lbs) | $50,000 | Yes — full deduction | 5 years |

| Plumbing | Drain inspection cameras | $8,000 | Yes — full deduction | 7 years |

| Plumbing | Hydrojetting equipment | $15,000 | Yes — full deduction | 7 years |

| Electrical | Cargo vans (over 6,000 lbs) | $40,000 | Yes — full deduction | 5 years |

| Electrical | Wire pulling machines | $6,000 | Yes — full deduction | 7 years |

| Electrical | Testing equipment (megohmmeters, analyzers) | $4,000 | Yes — full deduction | 7 years |

| GC | Pickup trucks (over 6,000 lbs) | $55,000 | Yes — full deduction | 5 years |

| GC | Excavators | $80,000 | Yes — full deduction | 5 years |

| GC | Concrete equipment (mixers, saws, forms) | $25,000 | Yes — full deduction | 7 years |

| Landscaping | Zero-turn mowers | $12,000 | Yes — full deduction | 7 years |

| Landscaping | Enclosed trailers | $10,000 | Yes — full deduction | 5 years |

| Landscaping | Skid steers | $35,000 | Yes — full deduction | 5 years |

Key takeaway: Virtually every piece of equipment a trade contractor buys — from a $3,000 recovery machine to an $80,000 excavator — qualifies for full Section 179 expensing in year one. The only question is whether you make the election on your tax return.

For items that cost $2,500 or less per unit, the de minimis safe harbor offers an even simpler path than Section 179. You expense the full cost immediately — no Form 4562 required, no asset tracking, no depreciation schedule.

This covers most hand tools and portable equipment that contractors buy regularly: pipe wrenches, cordless drills, multimeters, testing probes, levels, laser measures, sawzalls, impact drivers, and similar items.

Requirements to use the de minimis safe harbor:

Without the de minimis election, a $1,800 combustion analyzer gets capitalized and depreciated over seven years — giving you roughly $257 per year in depreciation expense. With the election, you deduct the full $1,800 in the year of purchase. Multiply that across 10-15 tool purchases per year and the difference adds up fast.

Not every asset qualifies for Section 179 or bonus depreciation. Real property improvements, certain listed property, and assets where you choose not to elect Section 179 default to the Modified Accelerated Cost Recovery System (MACRS). Here are the recovery periods relevant to contractors:

| Asset Class | MACRS Recovery Period | Examples |

|---|---|---|

| Vehicles (cars, trucks, vans) | 5 years | Work trucks, cargo vans, service vehicles |

| Equipment & machinery | 7 years | Generators, compressors, power tools, diagnostic equipment |

| Office furniture & fixtures | 7 years | Desks, shelving, shop furniture |

| Land improvements | 15 years | Parking lots, fencing, landscaping, drainage |

| Nonresidential real property | 39 years | Shop buildings, warehouses, offices |

MACRS uses accelerated front-loading (200% declining balance for 5- and 7-year property), so you still get larger deductions in the early years — just not as large as the full first-year write-off under Section 179. For a $50,000 truck on a 5-year MACRS schedule, your first-year deduction is approximately $10,000 (20%). Under Section 179, it’s $50,000 (100%).

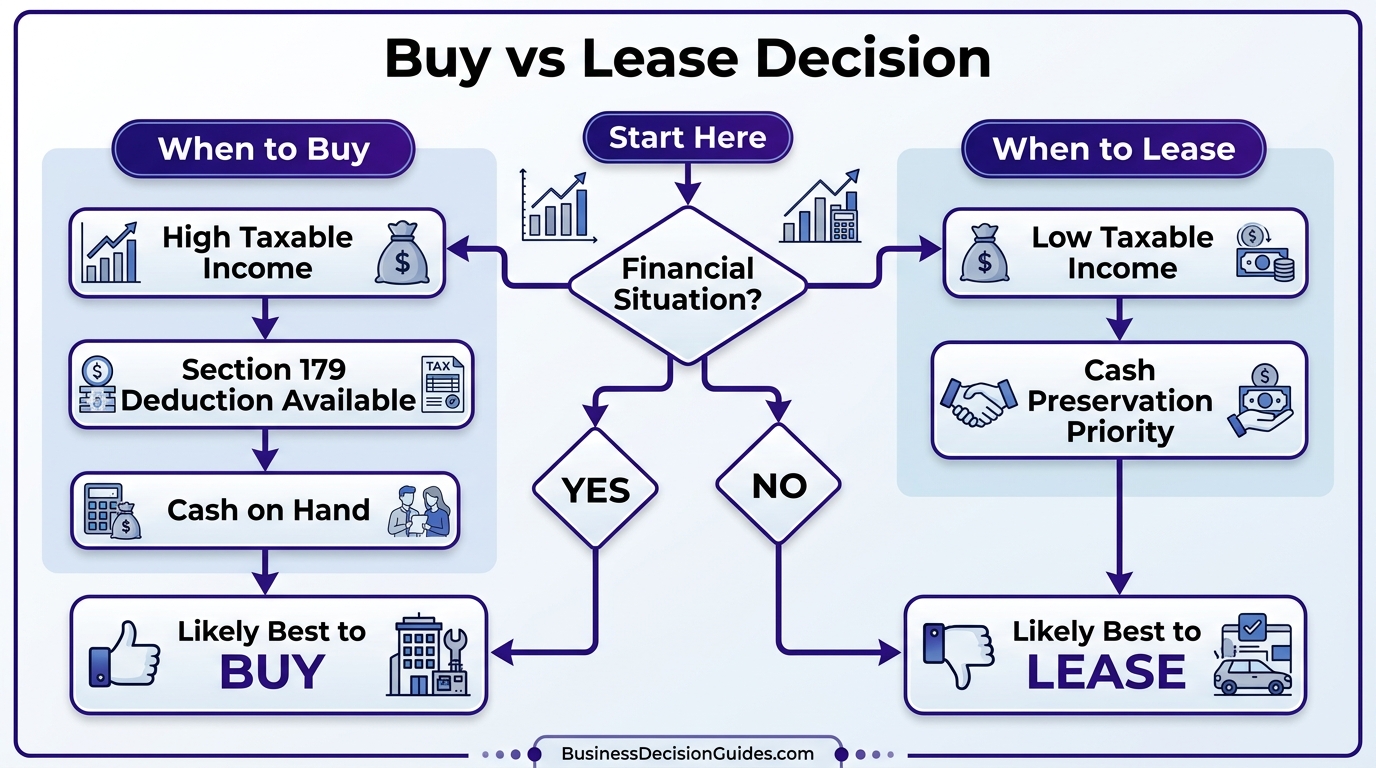

The buy vs. lease decision changes fundamentally when Section 179 is in play. Without Section 179, leasing spreads your cash outflow and gives you a predictable monthly expense. With Section 179, buying produces a massive first-year tax deduction that leasing cannot match.

The math example: A plumbing contractor buys a $50,000 work truck (over 6,000 lbs GVWR) and elects Section 179. At a 24% federal tax bracket, the $50,000 deduction saves $12,000 in federal taxes in year one. A lease on the same truck at $1,100/month produces a $13,200 annual deduction — but spread evenly over the lease term. The purchase produces a $12,000 tax savings immediately; the lease produces roughly $3,168 in year-one tax savings ($13,200 x 24%). Over time, the total deductions may be similar — but the time value of money favors the purchase with Section 179.

For more on how equipment costs fit into your overall bookkeeping strategy, including job costing and overhead allocation, see our contractor services page.

Section 179 requires that the asset be used more than 50% for business purposes in the year it is placed in service. If business use drops to 50% or below in a subsequent year, you must recapture a portion of the Section 179 deduction — meaning you’ll owe additional tax.

For most contractor-owned equipment, this isn’t an issue. A drain camera or an excavator is used 100% for business. But vehicles are where problems arise. If a work truck is also the owner’s personal vehicle — weekend trips, family errands, personal use — the IRS can challenge the business use percentage.

If you claim 100% business use and get audited, the IRS will ask for documentation. “I only use it for work” is not sufficient. You need a contemporaneous log.

1. Not electing Section 179 on the tax return. The election is made on Form 4562, attached to your return for the year the asset was placed in service. If you or your CPA forgets, you default to MACRS depreciation — and you generally cannot amend to claim Section 179 after the fact for that tax year.

2. Mixing personal and business use without documentation. You buy a $60,000 truck, claim full Section 179, and drive it to your kid’s soccer games three times a week. Without a mileage log showing over 50% business use, the IRS can deny the entire Section 179 deduction and recapture what you’ve already claimed.

3. Failing to document the placed-in-service date. Section 179 applies in the year the asset is placed in service — not the year you ordered it, not the year you paid for it. If you buy a truck in December but it’s not delivered and ready for use until January, the deduction moves to the following tax year. Keep delivery receipts, registration dates, and first-use documentation.

4. Ignoring the vehicle weight threshold. We’ve seen contractors buy two or three vans in a year — some over 6,000 lbs, some under — and claim the full Section 179 deduction on all of them. The under-6,000 lb vehicles are subject to luxury auto limits and will get flagged in an audit.

5. Not coordinating between bookkeeper and CPA. Your bookkeeper tracks the purchase. Your CPA files the return. If they don’t communicate about Section 179 elections, placed-in-service dates, and vehicle weights before filing, opportunities get missed and mistakes get made.

| Item | 2026 Rule |

|---|---|

| Section 179 deduction limit | $2,560,000 |

| Phase-out threshold | $4,090,000 |

| Bonus depreciation rate | 100% (assets placed in service after Jan 19, 2025) |

| Vehicle GVWR threshold | Over 6,000 lbs = full deduction |

| Luxury auto limit (under 6,000 lbs, with bonus) | ~$20,400 year one |

| Luxury auto limit (under 6,000 lbs, no bonus) | ~$12,400 year one |

| De minimis safe harbor threshold | $2,500 per item |

| MACRS recovery — vehicles | 5 years |

| MACRS recovery — equipment | 7 years |

| Business use requirement | More than 50% |

For the full IRS rules, see IRS Publication 946 and the Section 179 deduction calculator at Section179.org.

Equipment purchases shouldn’t be a tax guessing game. Steph’s Books specializes in bookkeeping for trade contractors — HVAC, plumbing, electrical, GC, and landscaping. We track vehicle weights, flag Section 179 opportunities, and coordinate with your CPA before year-end so nothing gets missed. Get an instant quote or schedule a free consultation to see how much you could save.

Answer a few quick questions for an instant, no-obligation quote — no sales call required. See how Steph's Books saves you 40-60% vs. hiring in-house.