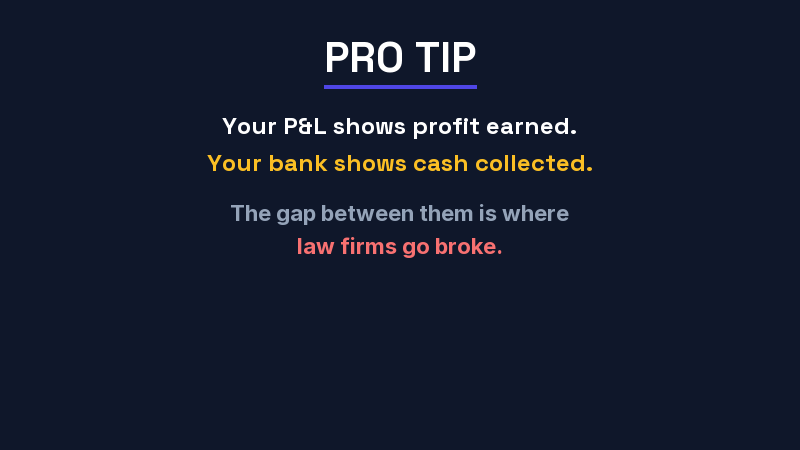

Your P&L says the firm made $400,000 in profit last quarter. Your bank account says you can't cover payroll next Friday. Both are telling the truth — and that disconnect is the most common law firm cash flow problem we see at Steph's Books. The profit is real on paper, but the cash isn't in your account. Understanding why is the difference between a thriving practice and a firm that's one bad month away from crisis.

This isn't a bookkeeping error. It's a structural problem built into how most law firms track revenue, manage trust accounts, and handle partner compensation. Let's break down exactly where your cash is hiding and how to get it back.

The profit and loss statement measures economic activity — revenue earned and expenses incurred during a period. Your bank account measures cash on hand. These are fundamentally different numbers, and the gap between them is where law firms get into trouble.

Here's a simplified example that illustrates the problem:

| Line Item | What the P&L Says | What the Bank Says |

|---|---|---|

| Revenue billed this quarter | $750,000 | $0 (invoices sent, not collected) |

| Revenue collected this quarter | Not shown on P&L | $520,000 (from this and prior quarters) |

| Work in progress (unbilled) | Not shown on P&L | $0 (no invoice = no collection) |

| Retainers in trust (unearned) | Not shown as revenue | $180,000 sitting in IOLTA |

| Operating expenses paid | $350,000 | $350,000 |

| Partner draws / distributions | Not shown on P&L | $200,000 taken out |

| Profit / Cash balance | $400,000 profit | -$30,000 (can't make payroll) |

See the problem? The P&L shows $400,000 profit. The bank shows negative cash. The difference is explained by uncollected receivables, unbilled WIP, trust account balances, and partner draws that don't appear on the income statement.

Every law firm dealing with this issue has at least two or three of these working against them simultaneously. Let's go through each one.

Your attorneys completed $180,000 of work last month. Only $120,000 was billed. The remaining $60,000 is sitting as work in progress (WIP) — time recorded but not yet invoiced. Until it's billed, it can't be collected. Until it's collected, it's not cash.

The industry benchmark for lockup days (the time from when work is performed to when cash is received) is 60–90 days. Many firms we work with are running at 120–150 days. Here's what that costs you:

| Monthly Revenue | Lockup Days | Cash Trapped in Pipeline |

|---|---|---|

| $200,000 | 60 days | $400,000 |

| $200,000 | 90 days | $600,000 |

| $200,000 | 120 days | $800,000 |

| $200,000 | 150 days | $1,000,000 |

A firm billing $200,000 per month with 120-day lockup has $800,000 trapped between work performed and cash received. Cut that to 75 days and you free up $300,000.

Pro Tip: Calculate your firm's lockup days right now. Take your total WIP + Accounts Receivable, divide by your average daily revenue. If it's over 90 days, you have a cash flow problem regardless of what your P&L says. Track this as a leading indicator monthly.

This is one of the most overlooked law firm cash flow problems. You have $180,000 in your IOLTA from client retainers. Some of that money has been earned — the work was completed, the time was billed against the retainer — but nobody transferred the earned portion to the operating account.

We see firms leaving $50,000–$100,000+ of earned fees in trust simply because the process of billing against retainers and transferring earned funds is manual, tedious, and nobody's specific job. That's your cash, sitting in trust, while you can't make payroll from operating.

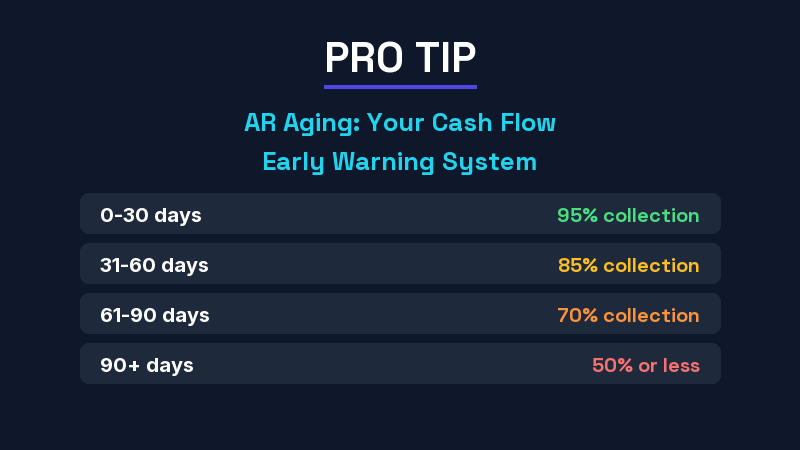

You billed $750,000 this quarter but only collected $520,000. Where's the other $230,000? It's sitting in accounts receivable — invoices that clients haven't paid yet. The older those invoices get, the less likely you are to collect them.

| Invoice Age | Collection Probability | Action Required |

|---|---|---|

| 0-30 days | 95% | Standard follow-up |

| 31-60 days | 85% | Personal call from billing partner |

| 61-90 days | 70% | Payment plan or escalation |

| 91-120 days | 50% | Final demand; consider write-off |

| 120+ days | 25% | Collection agency or write-off |

If 30% of your receivables are over 90 days, you've effectively given your clients an interest-free loan — and written off a quarter of that revenue without realizing it.

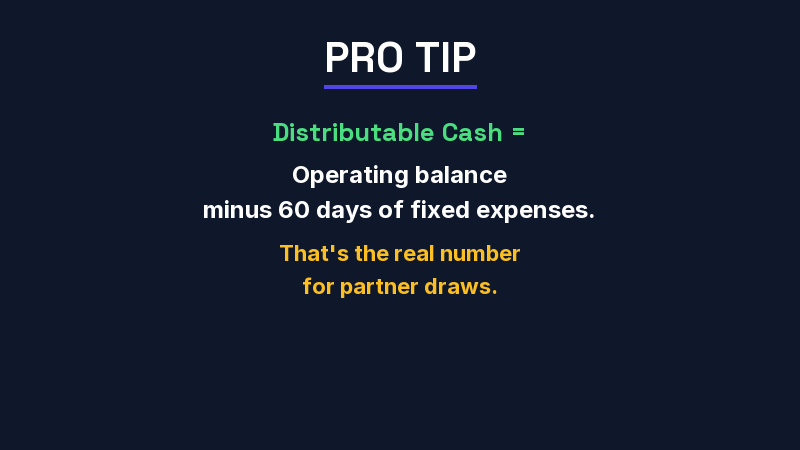

Partners see a profitable P&L and take draws accordingly. The problem: partner draws come from cash, not from profit. If the firm earned $400,000 in profit but only collected $200,000 in cash (after expenses), partners can't take $300,000 in draws without draining the operating account.

This is the most politically difficult cash flow problem to address because it requires partners to accept that profit is not the same as distributable cash. A firm generating $400,000 in accrual-basis profit might only have $150,000 available for distribution after accounting for WIP, receivables, and operating reserves.

Some firms run on cash basis for tax purposes but manage operations on accrual basis (or vice versa). This creates confusion about what "profit" actually means. On cash basis, you only recognize revenue when cash is received — so your P&L more closely mirrors your bank account. On accrual basis, you recognize revenue when it's earned (billed), regardless of collection.

If your P&L is accrual-based and you're making cash-based decisions, you'll overspend every time. Read our deep dive on cash vs. accrual accounting for law firms to understand which method fits your firm.

These aren't theoretical suggestions. They're the exact steps we implement when onboarding law firms at Steph's Books.

The fastest way to improve cash flow is to shorten the billing cycle. Most firms bill monthly. Switch to weekly billing for matters over $5,000 and you'll cut 21 days off your lockup immediately. For contingency matters, bill costs monthly even if fees are deferred.

Set a standing weekly process: review all trust balances, identify earned fees, and transfer them to operating. This should take 30 minutes per week. If you're not doing it, you're sitting on your own cash.

At 30 days past due, send a reminder. At 45 days, the billing partner calls. At 60 days, require a payment plan or stop work. Zero exceptions. The firms that enforce this collect 90%+ of billings. The firms that don't enforce it write off 15-25%.

Calculate distributable cash monthly: Operating cash balance minus 60 days of fixed expenses minus any payroll/tax obligations. That's the maximum available for partner distributions. Not the P&L profit. Not the revenue. The actual cash after obligations.

Most law firms look at the P&L and balance sheet. Almost none look at the cash flow statement. This report shows exactly where cash came from and where it went — broken into operating activities, investing activities, and financing activities (including partner draws). It's the report that bridges your P&L profit to your bank balance.

Ask your bookkeeper or outsourced bookkeeping/CFO partner to produce one monthly. If they can't, that's a sign you need a more capable financial partner.

Stop managing your firm from the P&L alone. Here are the five numbers you should review weekly:

| Metric | Target | Why It Matters |

|---|---|---|

| Lockup days (WIP + AR) | < 75 days | Measures how fast work converts to cash |

| WIP over 30 days | < 15% of total WIP | Identifies billing bottlenecks |

| AR over 60 days | < 10% of total AR | Identifies collection problems |

| Trust-to-operating transfer lag | < 48 hours | Ensures earned fees reach operating promptly |

| Weeks of operating cash on hand | > 8 weeks | Your runway — how long you survive without new collections |

Use your bookkeeping health check to assess where your firm stands today.

Ready to fix the gap between profit and cash? Steph's Books provides law firm bookkeeping with monthly cash flow reporting, trust account management, and the financial visibility you need to make confident decisions. Get an instant quote to see what it costs for your firm.

Get a free quote and see how Steph's Books can save you 40-60% vs hiring in-house.