Expert tips, guides, and insights to help you manage your business finances.

Set up trust accounting for property management in QuickBooks the right way — chart of accounts, sub-accounts, journal entries, and monthly reconciliation.

Read Article

Owner statement errors are the #1 reason property managers lose clients. Here are the 10 most common mistakes — and exactly how to eliminate each one.

Scaling past 50 properties? Learn how to structure multi-entity property management accounting in QuickBooks with intercompany controls and a 10-day close.

Property management fraud prevention checklist: spot vendor kickbacks, phantom invoices, and rent skimming with 7 bookkeeping controls that work.

Your IOLTA doesn’t balance? Stop. This step-by-step guide walks you through finding the discrepancy, fixing it, and knowing when to call your bar.

Most law firm partnership disputes start with the compensation check. Guaranteed payments, draws, K-1 distributions, and tax reserves — the mechanics most partnership agreements leave undefined until the cash gets tight.

Every messy set of books has the same root problem: bank accounts that were never properly connected to QuickBooks Online. This guide walks you through both ways to add a bank account in 2026, what to verify first, and the pitfalls that quietly break bank feeds.

Most law firm software comparisons pick a winner. This one picks winners by category — pricing, IOLTA, billing, integrations, document automation — so you can match the platform to your firm's actual shape.

Trust accounting is the single most frequent source of attorney discipline. Three-way reconciliation is the monthly process that prevents it — when done correctly. Here's the workflow, the common discrepancies, and the software that gets it right.

You’re a freelancer choosing between FreshBooks and QuickBooks, and every comparison you’ve read so far ends with “it depends.” Helpful. Let’s fix that. Here’s what the FreshBooks vs QuickBooks debate actually comes down to for freelancers: FreshBooks is built for invoicing clients. QuickBooks is built…

Bench Accounting shut down abruptly in December 2024, leaving thousands of small business owners scrambling to find a new bookkeeping solution — many of them mid-month-end close, some of them mid-tax-season. If you’re one of those businesses (or you’ve been putting off the switch because…

You’ve narrowed the accounting software field down to two finalists: QuickBooks Online and Xero. Good instincts. In 2026, these are the only two platforms that matter for the vast majority of small businesses — and despite what the affiliate bloggers want you to believe, the…

A Loop law firm running $3.2 million in annual revenue discovered during an audit that they’d been miscalculating Chicago’s Personal Property Lease Transaction Tax on their copier leases for four years. The back taxes, penalties, and interest totaled $18,400 — on a tax most business…

The letter arrives on a Tuesday. Professional letterhead, certified mail. Your franchisor is exercising its contractual right to audit your financial records for the prior 24 months. You have 21 days to assemble three years of POS reports, bank statements, tax returns, vendor invoices, and…

When David opened his second Great Clips location, he added a Class in QuickBooks Online and figured he’d sort it out later. By the time he opened his fifth location — three in Illinois, two in Indiana — “later” had arrived in the form of…

A Subway franchisee in suburban Dallas discovered during a franchisor audit that she had been excluding DoorDash and Uber Eats revenue from her gross sales calculation for 18 months. Her reasoning made intuitive sense — the delivery platforms retained 25-30% of each order, so she…

Marcus owns four quick-service restaurant locations across suburban Chicago. Combined revenue last year: $2.8 million. His accountant — a generalist CPA who also handles two dental practices and a landscaping company — had been calculating royalties on net sales for three years. The franchise agreement…

Insurance is the third-largest expense for most Amazon DSPs — after payroll and vehicle costs — typically consuming 8-12% of gross revenue. A 25-route DSP running 30 vans can expect $140,000-$250,000/year in total insurance premiums across commercial auto, general liability, cargo, workers’ compensation, and umbrella…

Last month, a 20-route DSP owner found $6,400 in settlement errors by actually reading the line items instead of just checking the deposit amount. Duplicate chargebacks on three routes, an incentive tier miscalculation for one week, and a missing peak-day surcharge that Amazon never applied….

A 30-van Amazon DSP fleet costs $900,000-$1.6 million per year to operate — leases, fuel, insurance, maintenance, registration, and depreciation combined. That’s 25-40% of gross revenue flowing through your vehicle accounts, and most DSP owners don’t know their actual cost per mile within 20%. If…

Your delivery drivers are your largest expense — and your largest compliance risk. A 25-route Amazon DSP with 60 drivers spends $2.0-$2.4 million per year on Amazon DSP driver payroll between base wages, overtime, benefits, and payroll taxes. Get any of it wrong and you’re…

You run 25 routes out of a single delivery station. Revenue last year: $3.2 million. Drivers on payroll: 62. Vans in the fleet: 30. Take-home pay after everything? About $80,000 — a 2.5% net margin on a business that never stops moving. That number isn’t…

You sold 12,000 units last year at an average price of $28. Your supplier invoices total $96,000, so your COGS is $8.00 per unit and your gross margin is 71%. Except it is not, because you also spent $14,400 on ocean freight, $7,200 on customs…

You have been selling on Amazon for three years and never filed a sales tax return. Amazon collects and remits sales tax on your behalf through marketplace facilitator laws — so you thought you were covered. Then you launched a Shopify store, and suddenly you…

You sell on Amazon, Shopify, and Etsy. Amazon pays you every two weeks. Shopify pays daily. Etsy pays weekly. Each platform calculates fees differently, reports revenue differently, handles refunds differently, and deposits money into your bank account on a different schedule. Your bank statement shows…

Your Shopify store processed $94,000 in orders last month. Shopify Payments deposited $88,400 across 22 separate daily payouts. The $5,600 difference is scattered across transaction fees, refunds, chargebacks, and a Shopify Payments reserve hold you did not know existed. Now your bookkeeper is trying to…

Amazon deposited $47,312 into your bank account last month. Your Seller Central dashboard shows $68,440 in gross sales. The $21,128 difference — 30.9% of your revenue — vanished into a maze of referral fees, FBA fulfillment fees, storage charges, advertising costs, and return processing deductions….

Your Shopify store did $1.2 million in gross sales last year. Amazon added another $800K. Etsy kicked in $150K. When your CPA pulled the numbers together, you owed $38,000 in taxes on income you thought was $240,000 — but was actually $167,000 after marketplace fees,…

He built a digital agency from his apartment to $900,000 in revenue in three years. Twelve employees, four major clients, a project management system he was proud of. But every month, somewhere between midnight and 2 AM, he’d sit at his kitchen table trying to…

The owner of a $1.4 million marketing agency came to us in March for catch-up bookkeeping. Her previous bookkeeper had categorized 23% of expenses as “Miscellaneous” or “Other.” When we recategorized every transaction properly and cross-referenced against IRS-allowable deductions, we found $31,400 in legitimate deductions…

A consulting firm owner in Chicago ran payroll for 12 employees using a spreadsheet for three years. She calculated gross-to-net manually, wrote checks, and filed her own quarterly returns. It worked — until it didn’t. An IRS notice arrived for $18,400 in penalties: $6,200 for…

Your bookkeeper sends you three reports every month. You glance at the bottom line of the P&L, confirm you made money (or didn’t), and move on. The balance sheet gets filed without opening. The cash flow statement — if one even exists — might as…

Every business picks one of two accounting methods — cash or accrual — and uses it to record every transaction. The choice isn’t cosmetic. It determines when revenue and expenses show up on your books, what your tax bill looks like in any given year,…

Most new business owners treat bookkeeping as an afterthought — something to deal with “when things get busy.” Then tax season arrives, they have 11 months of unsorted bank transactions, and the CPA charges $3,000 to reconstruct what should have been maintained for $200/month. Setting…

She grew the business from $400,000 to $1.8 million in four years. Built a team of nine. Landed three anchor clients who alone accounted for $600K in annual revenue. By every visible metric, the company was thriving. But when the IRS notice arrived — $23,000…

You started freelancing and told yourself you’d handle the books. For the first year or two, you probably did. A spreadsheet, some bank statements, maybe a free Wave account — it worked fine when you had ten clients and $40,000 in revenue. Then things grew….

The freelancer home office deduction is one of the most valuable tax breaks available to self-employed workers — and one of the most frequently botched. About 60% of freelancers work from home at least part-time, but a surprising number either skip this deduction entirely (afraid…

You’ve been freelancing for two years, your income just crossed $60,000, and your current system is a spreadsheet with 14 tabs, a shoebox of receipts, and a growing sense of dread every time you open your bank statement. You know you need bookkeeping software. You…

A client hands you a 1099-NEC in January. Your day-job employer hands you a W-2. Both show income you earned last year — but the tax treatment couldn’t be more different. That 1099 income carries an extra 15.3% self-employment tax that your W-2 wages don’t,…

Most freelancers overpay on taxes. Not by a little — by $3,000 to $10,000 a year. The problem isn’t that the deductions don’t exist. It’s that nobody tells you about them until it’s too late, and your bookkeeper (if you even have one) categorizes everything…

You earned $120,000 freelancing last year. You were meticulous about tracking income and expenses. You even set aside money in a separate savings account for taxes. Then April rolled around, and the IRS hit you with a $1,200 underpayment penalty on top of your tax…

A graphic designer we work with made $185,000 last year. She landed two anchor clients in Q2, picked up a steady stream of Upwork projects through the summer, and closed a $28,000 brand identity package in November that she still talks about. It was her…

Construction payroll is harder than payroll in any other industry — and it’s not close. A typical professional services firm runs one pay rate per employee, in one state, with a standard overtime threshold. A mid-size contractor running three active jobsites might be juggling prevailing…

Getting contractor vs employee classification wrong in construction will cost you more than any blown bid. The IRS, the DOL, and your state labor board all have enforcement mechanisms aimed squarely at the trades — and construction is the single most audited industry for worker…

Your company pulled in $3.6 million last year. You’ve got a solid crew, clean safety record, and a pipeline of $800K+ public bids you’d love to chase. But your bonding agent just told you the surety company won’t go above $500,000 per job — and…

You submitted 47 bids last year. You won 11. Your accountant says the company made money. But which of those 11 projects actually made the margin you estimated? And of the 36 you lost — were you too high, too low, or bidding the wrong…

Your general contractor just closed out Q3 with $4.8 million in billings. The bank account looks healthy. The project managers are saying every job is on track. Then your bonding company reviews the financials, and the underwriter flags $620,000 in overbillings that your books never…

You did $5.2 million in revenue last year. Your crew finished 14 projects — three of them over $500K. You had a backlog that stretched into Q3. By every visible metric, your general contracting company was thriving. But when your accountant pulled the year-end balance…

Most electrical contractors overpay on taxes. Not by a little — by $8,000 to $20,000 per year in missed deductions, misclassified expenses, and depreciation strategies nobody elected. The problem isn’t that the deductions don’t exist. It’s that a general bookkeeper categorizing your expenses into QuickBooks…

If your electrical contracting company works on government projects — or plans to bid on them — electrical contractor prevailing wage requirements will define how you pay your crews, how you bid work, and how much documentation you carry on every job. The Davis-Bacon Act…

The overtime tax deduction for electricians is now law — and it changes how both employees and employers handle overtime pay for the next four tax years. Signed on July 4, 2025, as part of the One Big Beautiful Bill Act, this provision lets nonexempt…

You pulled permits on 340 jobs last year, ran four crews across residential service, commercial tenant improvements, and a handful of EV charger installations — and your QuickBooks still has a single income account called “Electrical Revenue.” Your CPA set it up that way five…

Most electrical contractors know their backlog. They can tell you how many jobs are on the board and roughly what they billed last month. Ask about their electrical contractor profit margins — real margins, by job type, net of burden and overhead — and the…

You billed $2.6 million last year. Your P&L says you made a profit. But your checking account balance tells a different story, and you cannot point to which projects put money in the bank and which ones quietly bled it out. That is the problem…

Your crew pulled $3.4 million in revenue last year. You landed two data center fit-outs, ran a steady stream of residential panel upgrades, and picked up an EV charger installation contract with a regional auto dealer. But when your accountant closed the books, net profit…

Certified payroll and Davis-Bacon compliance for contractors. Form WH-347, prevailing wage requirements, apprentice ratio tracking, penalties, and bookkeeping workflow.

1099 subcontractor compliance for contractors. W-9 collection, payment tracking, 1099-NEC filing requirements, IRS penalties, and worker misclassification risks.

Section 179 and equipment depreciation for contractors in 2026. Deduction limits, truck weight thresholds, bonus depreciation, and buy vs lease decisions for trade contractors.

Manage plumbing company cash flow through seasonal swings. Build reserves, speed up receivables, use progress billing for large projects, and stabilize revenue.

Manage 1099 subcontractors in your plumbing business. W-9 collection, payment tracking, IRS penalties, worker misclassification risks, and year-end filing workflow.

Set up QuickBooks Online for your plumbing company. Complete chart of accounts, job costing with classes and projects, and integration with ServiceTitan, Housecall Pro, and Jobber.

Plumbing profit margin benchmarks for 2026. Gross margin by service type, net margin targets, and the 5 most common margin killers for plumbing contractors.

Complete plumbing contractor tax deduction checklist for 2026. Section 179 for trucks and tools, vehicle expenses, licensing, insurance, and 1099 filing requirements.

Set up plumbing job costing to track profitability by service call, drain cleaning, remodel, and new construction. Includes QuickBooks setup and worked examples.

HVAC profit margin benchmarks for 2026. Net margin targets, gross margin by job type, revenue per technician, and 5 strategies to improve profitability.

HVAC technician payroll done right. Overtime rules, spiff allocation for overtime recalculation, commission tracking, and fully loaded burden rate calculation.

Compare ServiceTitan, Housecall Pro, and Jobber QuickBooks integrations from a bookkeeper perspective. What syncs, what breaks, and what your bookkeeper needs.

HVAC tax deductions most contractors miss. Section 179 for trucks over 6,000 lbs, tool expensing, mileage deductions, and home office write-offs for HVAC businesses.

Manage HVAC seasonal cash flow with a month-by-month framework. Build reserves during peak season, survive slow months, and stabilize revenue with maintenance contracts.

Learn how to set up HVAC job costing to track profitability by service call, installation, and maintenance agreement. Includes burden rate calculation and QuickBooks setup.

Complete guide to plumbing bookkeeping. Job costing, 1099 subcontractor tracking, truck stock management, tiered labor rates, and profit margin benchmarks.

Complete guide to HVAC bookkeeping. Job costing, seasonal cash flow, technician payroll, service agreements, and QuickBooks setup for HVAC contractors.

A phase-by-phase playbook for cleaning up neglected law firm books, from trust account triage to ongoing maintenance, with cost estimates and timelines.

The 4 most common embezzlement schemes at law firms, warning signs you're missing, a 5-point prevention checklist, and why outsourced bookkeeping is the best defense.

Week-by-week timeline from onboarding to steady state. What to provide, success metrics, and red flags to watch for.

What each role does, when you need one versus the other, cost comparison, and signs you have outgrown bookkeeping-only.

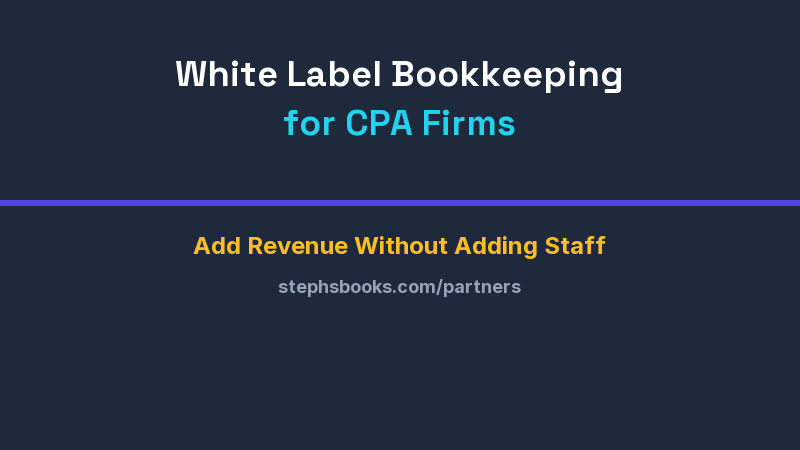

Learn how CPA firms can add recurring bookkeeping revenue through white label partnerships — without hiring, training, or managing bookkeepers.

Your P&L shows last month. Your business is happening now. Learn the leading indicators every professional services firm should track weekly and how to build a business driver dashboard.

Cash vs accrual accounting for law firms — tax implications, IRS requirements, and which method fits your firm size. Includes conversion guidance.

The 7 financial KPIs every law firm managing partner needs to review monthly. Benchmarks, formulas, and red flags for realization rate, collection rate, and more.

Compare matter-based billing and flat fee accounting for law firms. Revenue recognition, WIP tracking, realization rates, and which model fits your practice.

How to track partner distributions, equity, and K-1 preparation for law firms. Covers eat-what-you-kill, lockstep, and hybrid compensation models.

Step-by-step guide to IOLTA trust account reconciliation for law firms. Three-way reconciliation, common violations, and compliance best practices.

Complete guide to property management accounting — CAM reconciliation, owner distributions, security deposits, property-level tracking, and chart of accounts. For property managers managing 50+ units.

Complete guide to law firm bookkeeping — IOLTA trust accounting, partner distributions, billing models, KPIs, and when to outsource. Built for managing partners.

2026 bookkeeping benchmarks for professional services firms. Staffing costs, technology adoption, monthly close times, and industry-specific data from BLS, AICPA, and Intuit.

Free property management chart of accounts template for QuickBooks. Numbered account structure, property-level tracking, and setup guide for 50+ unit portfolios.

Security deposit accounting for property managers — trust account rules, state-by-state requirements, interest-bearing accounts, and move-out reconciliation.

What to include in owner distribution reports for property management. Templates, timing, reserve calculations, and how to prevent owner disputes.

How to set up QuickBooks Online to track income and expenses by property. Location tracking, class tracking, and reporting for property managers.

Complete guide to CAM reconciliation for property managers. Step-by-step process, common errors, tenant dispute prevention, and software recommendations.

The biggest accounting fraud cases in history include Enron ($74 billion), WorldCom ($11 billion), Bernie Madoff ($65 billion), Wirecard ($2.1 billion), and Tyco ($600 million). Here’s what happened in each case and the bookkeeping red flags that should have caught them. When we think of…

Ghost payroll fraud occurs when an employer’s payroll includes payments to employees who don’t exist, have left the company, or aren’t actually working. It’s one of the most common forms of occupational fraud, costing U.S. businesses an estimated $5 billion annually. Somewhere in your payroll…

Here’s a statistic that should keep every business owner up at night: the Association of Certified Fraud Examiners (ACFE) 2024 Report to the Nations found that the median loss from occupational fraud is $117,000 per scheme. The median duration before detection? 12 months. That means…

Every outsourced bookkeeping firm’s website says the same things: “accurate books,” “dedicated team,” “industry expertise.” The proposals look similar. The pricing seems comparable. And yet, the wrong choice will cost you three to six months of lost time, messy data, and a painful migration to…

DIY bookkeeping works at $200K in revenue. You’re doing the data entry, the reconciliation, maybe running payroll yourself. It takes a few hours a month. No big deal. Then your firm crosses $1M. And that “free” bookkeeping becomes the most expensive thing you do. Not…

You know you’re behind on your books. Maybe it’s been three months. Maybe it’s been three years. Either way, the pile of unreconciled transactions, missing records, and “I’ll deal with it later” decisions has turned into a real problem. You’re not alone. According to a…

Your firm bills $175/hour. Your managing partner spent six hours last month reconciling QuickBooks because your office manager was on PTO. That’s $1,050 in lost billable time — on a task that an outsourced bookkeeping team handles for $500/month. That math is why professional services…

Step-by-step QuickBooks Online setup guide for professional services firms. Chart of accounts, class tracking, bank feeds, invoicing, payroll, and reporting — configured for project profitability, not retail.

How much does outsourced bookkeeping cost in 2026? Real pricing by business size, from $200/mo to $10,000+/mo, plus what drives the price and red flags to avoid.

Compare the true cost of in-house vs. outsourced bookkeeping for $1MM-$10MM firms. Salary, benefits, software, turnover — the full picture most owners miss.

Your firm billed $2.4M but your bank account says $900K. Here are 5 structural bookkeeping gaps draining professional services firms — with the formulas to find and fix each one.

Compare 9 property management accounting software platforms in 2026 — AppFolio, Buildium, Yardi Breeze, and more. Includes trust accounting compliance, 1099 filing, CAM reconciliation, and recommendations by portfolio size.

Compare the 8 best law firm bookkeeping software platforms in 2026 — Clio, CosmoLex, QuickBooks + LeanLaw. Includes IOLTA trust accounting compliance, pricing breakdowns, and specific recommendations by firm size.

A QuickBooks ProAdvisor is a certified accounting professional who has passed Intuit’s official certification exams and demonstrated deep expertise in QuickBooks Online, QuickBooks Desktop, or both. Unlike a general bookkeeper who happens to use QuickBooks, a ProAdvisor has proven mastery of the platform’s advanced features…

Accounting and bookkeeping for Airbnb properties are essential for keeping track of all rental income and expenses. Doing so ensures the business stays organized and taxes are accurately reported. Most importantly, these practices help you make informed business decisions to keep cash flowing and your…

Bookkeeping involves more than numbers and spreadsheets — it’s the process of recording each of your business’ financial transactions. Whether you’ve been an entrepreneur for years or you’re only getting started, you can improve your finances. Bookkeeping gives you an accurate view of your organization’s…

In a perfect world, what’s left in your business bank account at the end of the month would align with what your company spent or earned that month. That doesn’t always happen, though, due to delays in payment processing or deposits. A discrepancy between your…

Payroll is often an overlooked priority, and busy business owners don’t always have the time to do it. This leads many to the question — should a business outsource payroll? While some business owners choose to handle payroll in-house through a payroll app or manual bookkeeping, others…

A bank reconciliation discrepancy is a difference between your bank statement balance and your accounting records. Common causes include outstanding checks, deposits in transit, bank fees, errors in data entry, and unauthorized transactions. Below is a step-by-step guide to finding and fixing discrepancies. A Bank…

Every small business owner hits the same fork in the road: keep tracking finances in Excel spreadsheets, or invest in dedicated accounting software like QuickBooks? It is the most common QuickBooks vs Excel debate in small business bookkeeping, and the right answer depends on where…

It’s the age-old question, isn’t it? “What does a bookkeeper do?” Maybe you’re a business owner who’s been handling your own finances with a spreadsheet and a prayer. Maybe your accountant just told you to “get a bookkeeper” and you nodded like you knew what…